Nov. Payrolls Beat, But Rising Unemployment Sets Off Market Alarms

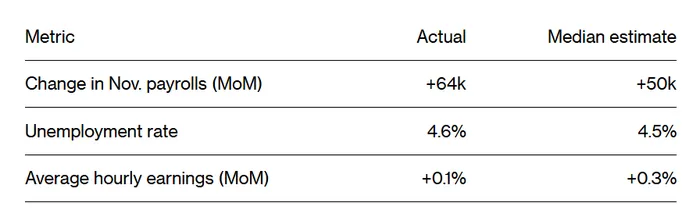

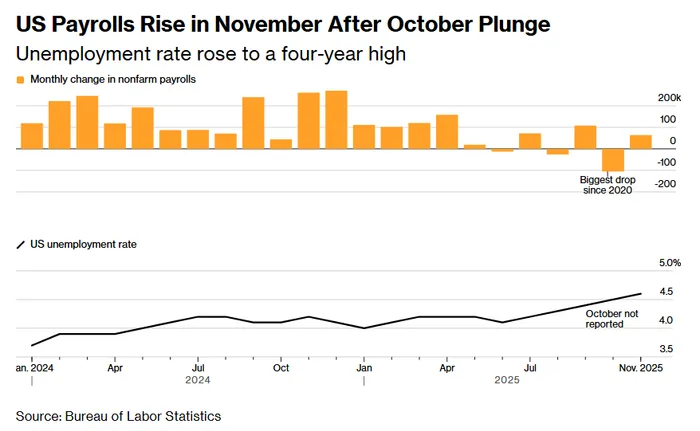

The U.S. Bureau of Labor Statistics (BLS) released the latest nonfarm payrolls report. In November, U.S. nonfarm employment increased by 64,000, beating market expectations of 50,000.

However, the unemployment rate unexpectedly rose to 4.6% in November, above the expected 4.5%, marking the highest level since September 2021. October’s unemployment rate was permanently unavailable due to the government shutdown.

In addition, the BLS released the delayed October nonfarm payroll data, which had been suspended because of the shutdown. Employment in October declined by 105,000, far worse than the market expectation of a 25,000 decline. The BLS stated it was unable to quantify the impact of the shutdown on the October–November surveys, indicating deficiencies in data completeness and comparability.

The BLS also revised down employment figures for August and September. August payrolls were revised from a decline of 4,000 to a decline of 26,000, while September was revised from an increase of 119,000 to 108,000. Combined, these revisions subtracted 33,000 jobs, further confirming labor-market weakness.

Following the data release, federal funds futures showed that the probability of a January rate cut rose modestly to 31%, up from 22% before the report.

Markets currently expect the Federal Reserve to cut rates twice in 2026. However, the December dot plot indicates that FOMC officials anticipate only one rate cut next year.

Healthcare Remains the Hiring Engine, Manufacturing Jobs Continue to Decline

By sector, healthcare remained the primary source of job growth in November, adding 46,000 jobs—above its past-year average of 39,000 per month. Construction added 28,000 jobs, while social assistance gained 18,000.

Other sectors were far weaker. Despite repeated calls for reshoring manufacturing, the data do not support that narrative. Manufacturing employment fell by 5,000 in November, following a 9,000 decline in October.

Although the “Department of Government Efficiency” (DOGE) has been dissolved, its effects persist. Federal government employment declined by 6,000 in November, after a sharp drop of 162,000 in October, becoming a major drag on overall employment.

Transportation and warehousing shed 18,000 jobs in November, concentrated in courier and logistics roles, signaling synchronized cooling in consumer demand and freight activity.

Wage data also pointed to deceleration. Average hourly earnings rose 3.5% year over year in November, the slowest pace since May 2021. Slowing real wage growth implies declining household purchasing power.

There was, however, one positive signal: average weekly hours increased to 34.3, the highest level since July. Working hours are a leading indicator for layoffs, as employers typically reduce hours before cutting headcount.

Many economists describe the current labor market as one of “low layoffs, low hiring.” Companies are not engaging in mass layoffs, but hiring appetite has turned cautious, partly because AI is replacing many entry-level roles.

Analysts Focus More on Rising Unemployment Risk; January Payrolls May Be More Informative

“This report sets a slightly dovish tone for monetary policy,” said Jeff Schulze, Head of Economic and Market Strategy at ClearBridge Investments. “The rise in unemployment warrants attention. We expect rate cuts in the first quarter, which should support risk assets.”

Seema Shah, Chief Global Strategist at Principal Asset Management, expressed skepticism about the data due to distortions and tighter immigration policy. “The labor market is cooling and warrants additional monetary easing, at least toward a neutral stance. The Fed may want more evidence of weakness, but based on today’s data, next year’s rate cuts could exceed the single cut implied by the dot plot.”

“We are more focused on wages,” said Bloomberg Intelligence analyst Ira Jersey. “Hourly earnings growth slowed to 3.5%, the lowest level of this cycle, suggesting the Fed may still lean toward easing.”

“Both October and November employment data look weak,” said Bloomberg economists Anna Wong, Stuart Paul, and Chris G. Collins. “Private-sector hiring is improving only marginally. While massive AI data-center demand supports construction jobs, hiring concentration in just a few sectors is concerning. In hindsight, December’s rate cut was the right decision.”

Some analysts argue the current data lack comparability, and that December’s payroll report—released next year—may be more informative.

“Given the prior data disruption, the Fed is unlikely to place much weight on today’s report,” said Kay Haigh, Global Co-Head of Fixed Income and Liquidity Solutions at Goldman Sachs Asset Management. “The December payrolls report, released ahead of the January FOMC meeting, will carry greater significance.”

Samuel Tombs, Chief U.S. Economist at Pantheon Macroeconomics, noted: “The labor market is weak but still resilient, and not weak enough to justify a January rate cut.”

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet