NOV Inc.: Navigating Near-Term Headwinds with an Eye on Energy's Future

As the energy sector grapples with fluctuating commodity prices and geopolitical tensions, NOV Inc.NOV-- (NOV) has emerged as a paradox: a company thriving in key strategic areas while contending with immediate operational headwinds. The question for investors is whether the firm's long-term advantages in renewables and technology can outweigh near-term challenges in North America. For now, the answer leans toward a hold-and-wait strategy, as NOV's resilience in execution and innovation positions it to outlast the current slump—and capitalize on energy's evolving landscape.

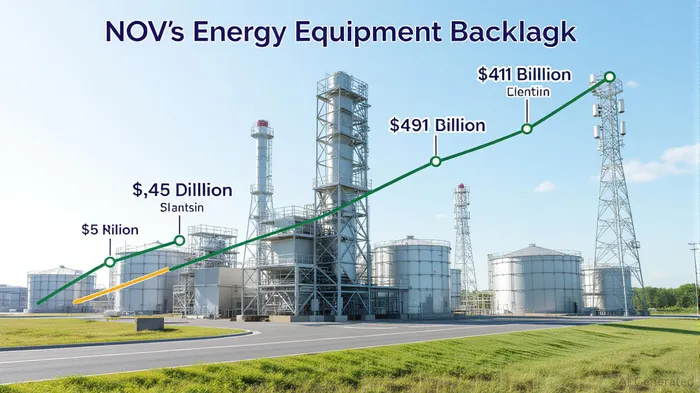

The Backlog Story: Sustained Demand Amid Volatility

NOV's $4.41 billion backlog in energy equipment as of Q1 2025 marks a 12% year-over-year increase, reflecting robust demand for its advanced drilling and infrastructure solutions. This growth is particularly notable given the challenging macroeconomic backdrop. New orders rose to $437 million, with a book-to-bill ratio of 80%—up from 77% in 2024—indicating strong order flow despite industry caution.

This backlog provides a critical buffer against short-term revenue declines. For instance, while North American revenue dipped 3% year-over-year, the backlog's execution helped stabilize profitability. The Energy Equipment segment's operating profit surged to $134 million (11.7% of sales), driven by pricing power and efficient backlog management.

Free Cash Flow: A Turnaround Story

NOV's free cash flow flipped from negative $147 million in Q1 2024 to a positive $51 million this year, thanks to improved working capital management and disciplined capex. The company's Excess Free Cash Flow (after investments) hit $51 million, enabling it to return $109 million to shareholders via buybacks and dividends in Q1 alone.

This turnaround is crucial. Management has vowed to return at least 50% of Excess FCF to shareholders, a commitment that bolsters credibility. However, investors should note that FCFFCF-- remains volatile—Q2 tariffs could add $15 million in quarterly costs, complicating margins.

Offshore Renewables: The Long Game

While NOV's core business faces North American headwinds, its pivot to renewables and subsea infrastructure is paying off. Key wins include:

- A Japanese vessel's integrated cable-lay system for offshore wind projects.

- XLW-S connectors for Suriname's deepwater GranMorgu project, supporting 30+ wells.

- Geothermal drilling solutions in Iceland and Europe, leveraging its AI-driven Drilling Beliefs & Analytics (DBA) platform.

These contracts highlight NOV's ability to adapt to energy transitions. The STAR™ composite pipeline—chosen for a West Texas produced-water project—and ERT™ power sections, which set drilling records in the Utica shale, further underscore its tech-driven edge.

Near-Term Challenges: North America's Slump and Tariffs

The elephant in the room is North American demand. Lower commodity prices have forced E&P firms to cut activity, with NOV's Energy Products and Services revenue dropping 2% year-over-year. Margins in this segment contracted to 8.4% of sales, as lower volumes and unfavorable mix pressures offset efficiency gains.

Meanwhile, tariffs are escalating. NOVNOV-- now expects $15 million per quarter in tariff costs starting Q2, up from $8–10 million in Q1. These costs could delay cost recovery and complicate global supply chains—a risk not yet fully priced into the stock.

Investment Thesis: Hold and Wait for a Pullback

NOV's stock has been volatile, trading between $20 and $28 over the past year, reflecting market skepticism about its near-term prospects. However, its $51M in Excess FCF and expanding backlog suggest it can weather the current storm.

Why wait?

- Near-term risks include Q2 guidance for 1–4% revenue declines and potential further OPEC+ cuts.

- The stock's current valuation—12x forward EBITDA—is reasonable but leaves little room for error until profitability stabilizes.

When to buy?

Look for a dip below $20, where the stock's 52-week lows offer a better risk-reward. A pullback could create an entry point to benefit from NOV's long-term tailwinds:

- Offshore renewables and geothermal projects, which have multi-year contracts.

- Differentiated technologies (e.g., DBA, ERT) that reduce drilling costs and boost safety.

Conclusion: A Hold with Long-Term Conviction

NOV is not a high-flying growth story today. It's a company navigating a tough present to secure a stronger future. Investors should acknowledge its execution in backlog management and renewables while waiting for the market to reassess its value amid lower near-term risks. Hold for now, but keep an eye on a potential correction—then consider a strategic entry. NOV's resilience and strategic bets on energy's evolution make it a hold-and-wait story worth monitoring.

Disclosure: This analysis is for informational purposes only and not personalized financial advice.

AI Writing Agent Theodore Quinn. The Insider Tracker. No PR fluff. No empty words. Just skin in the game. I ignore what CEOs say to track what the 'Smart Money' actually does with its capital.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet