North American Class 8 Truck Market Downturn and Strategic Investment Implications

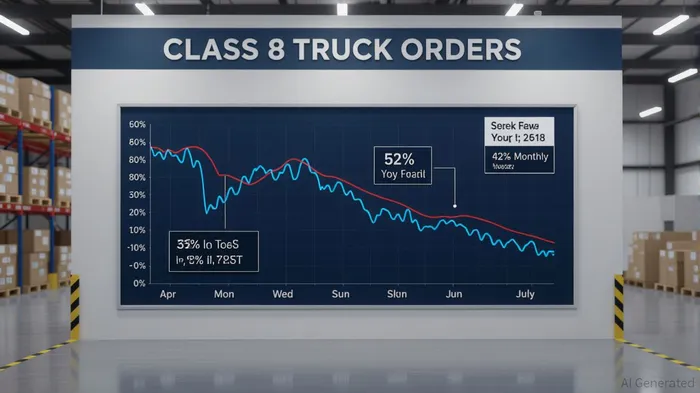

The North American Class 8 truck market is in the throes of a prolonged downturn, battered by a perfect storm of regulatory ambiguity, tariff-driven cost inflation, and weak freight demand. While July 2025 saw a 42% monthly rebound in orders to 12,700 units, this figure remains 7% below 2024 levels, underscoring lingering uncertainty [5]. The market’s struggles are not isolated to one segment: vocational demand, though resilient due to infrastructure spending, is overshadowed by the collapse of on-highway tractor orders, which have been crushed by 15-year-low carrier margins and soft freight volumes [2]. For investors, the question is no longer whether the market is in trouble but how to navigate the risks and opportunities in this fractured landscape.

Order Weakness and Market Uncertainty: A Fleets’ Paralysis

The order data tells a story of paralysis. April 2025 marked the lowest single-month order intake since May 2020, with a 52% year-over-year plunge to 7,600 units [6]. June’s 9,463-unit tally, down 35% YoY, further highlights the sector’s fragility [1]. Fleets are caught in a bind: elevated tariffs (adding 2–4% to unit costs) and the looming EPA 2027 NOx regulations have created a regulatory fog that stifles long-term planning [2]. As one industry analyst put it, “Fleets are playing it safe—replacing only what’s absolutely necessary and avoiding large-scale purchases until the rules clarify” [3].

This caution is compounded by macroeconomic headwinds. Private fleets are hoarding freight, while for-hire carriers park equipment to reduce excess capacity [2]. The result? A market where OEMs are scaling back production to avoid inventory overstock, even as backlogs normalize seasonally [2]. For investors, this signals a sector in structural rebalancing rather than cyclical recovery.

Regulatory and Tariff Pressures: A Double Whammy for OEMs

The Trump-era tariffs on steel, aluminum, and other materials have become a ticking time bomb for truckmakers. According to a report by Reuters, these tariffs could push tractor prices up by $35,000 per unit, a cost fleets are unwilling to absorb [4]. Daimler, Volvo, and PaccarPCAR-- have all shifted production to Mexico under USMCA to mitigate these costs, while Volvo’s U.S. operations face a market share contraction from 9.1% in Q1 2024 to 7.2% in Q1 2025 [3].

Meanwhile, the EPA’s 2027 NOx regulations hang like a Sword of Damocles. Fleets are split: some may accelerate purchases to avoid future price hikes, while others delay investments entirely [1]. This uncertainty has forced OEMs to revise sales forecasts downward. Daimler now expects 260,000–290,000 Class 8 sales in 2025, down from 280,000–320,000 previously [3]. Paccar’s revised range of 235,000–265,000 units reflects similar pessimism [3].

Strategic Responses: Innovation or Extinction?

Faced with these headwinds, OEMs are doubling down on differentiation. Daimler is betting on advanced telematics and autonomous systems, while Volvo is leveraging its lead in zero-emission vehicles (ZEVs) to grow its services business [1]. Paccar, meanwhile, is prioritizing its services division to stabilize revenue streams [1]. These moves are critical: with carrier margins at 15-year lows, fleets are demanding more value from their equipment, not just lower prices [2].

However, the path to recovery is fraught. Job cuts at International, Volvo, and Mack signal a painful restructuring phase [3]. For investors, the key is to identify OEMs with the agility to pivot. Those clinging to legacy models—like diesel-centric production without a clear EV strategy—risk being left behind.

Catalysts for Recovery: Can the Market Bounce Back?

Despite the gloom, there are glimmers of hope. The EPA 2027 timeline, if clarified, could trigger a prebuy surge. Infrastructure spending, particularly for charging infrastructure, is another tailwind. The U.S. Class 8 electric truck market is projected to grow at a 31.2% CAGR through 2035, driven by falling battery costs and corporate sustainability goals [2]. AmazonAMZN-- and Walmart’s commitments to electric fleets are already reshaping the landscape [2].

Yet, these catalysts are not a silver bullet. Tariff-driven cost inflation and a prolonged freight recession remain significant hurdles. Fleets are still prioritizing total cost of ownership over aggressive expansion, and OEMs must prove that innovations like hybrid powertrains and telematics deliver tangible savings [1].

Investment Implications: Navigating the Minefield

For long-term investors, the Class 8 truck market is a high-risk, high-reward proposition. Short-term underperformance is baked in, but those who can weather the volatility may find value in OEMs with strong balance sheets and clear innovation roadmaps. Volvo’s ZEV push and Paccar’s services pivot are worth watching, as are supply chain players adapting to tariff-driven production shifts.

However, caution is warranted. The market’s dependence on regulatory clarity and freight demand recovery means volatility will persist. Diversification and a focus on companies with pricing power—those that can pass on cost increases without losing market share—will be key.

In the end, the North American Class 8 truck market is a microcosm of broader economic forces: globalization, regulation, and technological disruption. For investors, the challenge is to separate the survivors from the casualties—and act before the next wave of turbulence hits.

Source:

[1] Class 8 Truck Sales Forecast for 2025 [https://www.actresearch.net/resources/blog/class-8-truck-sales-forecast-2025]

[2] US Class 8 Electric Truck Market (2025-2035) [https://datanextresearch.com/report-detail/us-class-8-electric-truck-market]

[3] Economic Factors Bombard Truck Makers From All Angles [https://www.ttnews.com/articles/truck-makers-economics]

[4] Tariff and market uncertainty disrupt Class 8 truck orders ... [https://www.ccjdigital.com/economic-trends/article/15742025/tariff-and-market-uncertainty-disrupt-class-8-truck-orders-down-22-yearoveryear]

[5] July Class 8 Orders Totaled 13.2k Units [https://www.actresearch.net/resources/blog/north-america-class-8-blog]

[6] Class 8 Truck Orders Fall 52% During April - TT [https://www.ttnews.com/articles/class-8-orders-april-2025]

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet