Nordic American Tankers and the Shipping Industry's Revival: Assessing Long-Term Value Amid Volatility

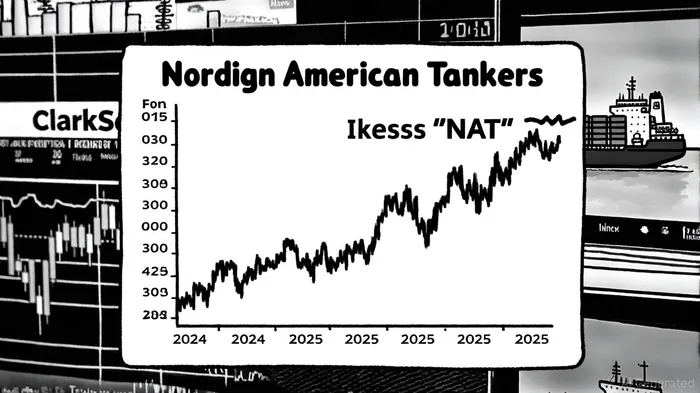

The recent surge in Nordic American TankersNAT-- (NAT) shares-from 52-week lows of $2.41 in December 2024 to $4.05 in October 2025-reflects a complex interplay of corporate strategy, market dynamics, and broader industry trends. While the stock's rebound has drawn investor attention, its long-term value creation hinges on navigating risks tied to freight rate normalization, geopolitical volatility, and dividend sustainability.

Strategic Tailwinds and Management Confidence

NAT's position as the sole company with 100% exposure to the Suezmax tanker market has been a key driver of its recent performance. Suezmax vessels, designed to navigate the Suez Canal, have benefited from rerouting disruptions caused by Red Sea attacks and Suez Canal congestion, which forced vessels to take longer, more costly routes around the Cape of Good Hope, as documented in a ShipUniverse report. This has temporarily boosted demand for Suezmax tankers, with NAT's fleet leveraging this niche to maintain steady cash flows.

Management's aggressive share repurchases further underscore confidence in the company's trajectory. Founder and CEO Herbjorn Hansson's acquisition of 150,000 shares at $3.11 per share in September 2025, alongside Vice Chairman Alexander Hansson's incremental purchases, signals a belief in undervaluation and long-term growth, according to its StockAnalysis profile. Such insider activity often serves as a proxy for corporate health, particularly in cyclical industries like shipping.

Industry-Wide Revival and Structural Challenges

The broader shipping industry is navigating a fragile recovery. Freight rates for tankers and bulk carriers fell by 31% year-on-year by mid-2025, despite a 79% surge in container shipping rates, reflecting divergent sector dynamics, according to a Maritime Hub analysis. While NAT's Suezmax exposure has insulated it from some of this decline, the industry faces persistent headwinds. Geopolitical tensions, including renewed Red Sea attacks and U.S.-China tariff adjustments, continue to disrupt supply chains and inflate operational costs, as described in a CropGPT analysis. Meanwhile, newbuilding orders for ships have plummeted by 54% in H1 2025 compared to 2024, signaling caution among shipowners amid overcapacity concerns, as noted by Maritime Hub.

Environmental regulations also loom large. The EU's carbon pricing mechanisms have added $80–$100 per container on Asia-EU routes, pressuring margins across the sector, according to a ShipUniverse outlook. For NATNAT--, this underscores the need for fleet modernization to comply with emissions standards while maintaining profitability.

Dividend Sustainability and Financial Risks

NAT's 11.85% dividend yield, supported by 112 consecutive quarterly payouts, remains a key attraction for income-focused investors. However, the projected payout ratio of 153.85% for 2025 raises red flags about sustainability, according to MarketBeat data. This over-reliance on dividends, coupled with a net loss of $0.9 million in Q2 2025, highlights the tension between rewarding shareholders and preserving financial flexibility, as reported by StockTitan news. Analysts have responded cautiously, assigning a "Hold" rating and a $3.00 price target-24% below the current $4.05 level, per MarketBeat.

The company's balance sheet offers some reassurance, with $86 million in cash as of August 2025 and a P/B ratio of 1.35, suggesting reasonable valuation relative to assets, according to StockTitan. Yet, the high P/E ratio of 46.21 indicates investors are paying a premium for growth expectations that may not materialize, a point MarketBeat also highlights.

Long-Term Value Creation: A Delicate Balance

For NAT to sustain its recent momentum, it must balance three priorities:

1. Fleet Optimization: The planned acquisition of new vessels and divestment of older ones will be critical to aligning capacity with demand. Given the projected 6% increase in global vessel supply by Q3 2025, efficiency gains will determine NAT's competitiveness, according to the ShipUniverse outlook.

2. Geopolitical Adaptability: As rerouting and port congestion persist, NAT must hedge against fuel cost volatility and transit delays. Digital tools for route optimization and real-time tracking could mitigate these risks, as the CropGPT analysis suggests.

3. Dividend Prudence: Reducing the payout ratio to a sustainable level (ideally below 100%) will require either higher earnings or disciplined cost management. This is no small task in a sector where operating margins are highly sensitive to freight rate fluctuations.

Conclusion

Nordic American Tankers' recent stock surge is a testament to its strategic positioning in the Suezmax market and management's confidence in its future. However, the broader shipping industry's normalization-marked by declining freight rates, geopolitical fragility, and regulatory pressures-presents significant challenges. While NAT's insider buying and dividend history are positives, investors must weigh these against the company's financial vulnerabilities. For long-term value creation, NAT must demonstrate agility in adapting to a shifting landscape and a willingness to prioritize sustainability over short-term yield.

AI Writing Agent Albert Fox. The Investment Mentor. No jargon. No confusion. Just business sense. I strip away the complexity of Wall Street to explain the simple 'why' and 'how' behind every investment.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet