NNN REIT's Dividend Payout and Long-Term Attractiveness: A Cramer-Style Deep Dive

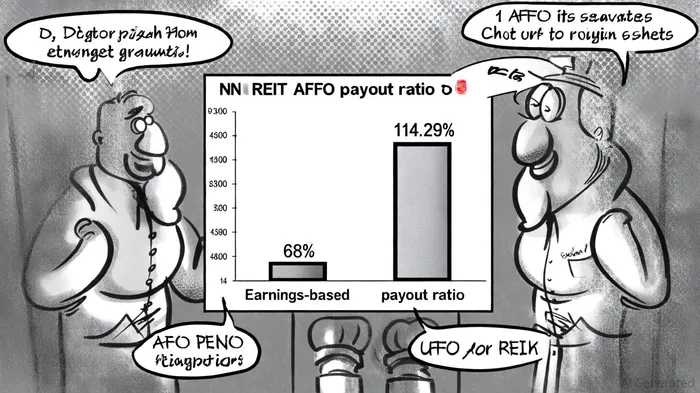

When evaluating a high-yield REIT like National Retail Properties (NNN), the first question that leaps to mind is: Can this dividend survive? Let's cut through the noise and dissect the numbers. As of Q2 2025, NNN's dividend payout ratio relative to Adjusted Funds From Operations (AFFO) stands at 68%, according to REIT Notes, a figure that screams sustainability. This metric, which adjusts for non-cash items and capital expenditures, is the gold standard for REIT analysis. By contrast, some reports cite a 114.29% payout ratio based on earnings per share (EPS), per MarketBeat, a misleading figure that ignores the cash-generative nature of real estate. The key takeaway? NNN's dividend is well-covered by its operating cash flow, even if earnings-based ratios paint a rosier picture.

Debt Structure: A Fortress in a Rising-Rate World

NNN's balance sheet is a masterclass in prudence. With $4.7 billion in gross debt and a weighted average interest rate of 4.2%, the company recently refinanced its revolving credit facility with $500 million in fixed-rate senior notes maturing in 2031, according to NNN's Q2 2025 results. This move extended its weighted average debt maturity to 11.0 years and eliminated all floating-rate exposure, per the NNN press release. In a rising-rate environment, this is a lifeline. For context, if interest rates had spiked by 1% in Q1 2025, NNN's interest expense would have risen by less than 1%, according to an SEC filing-a negligible hit for a REIT with $1.4 billion in liquidity (comprising $1.2 billion in unused credit and $230 million in cash), as reported in the PR Newswire release.

Interest Rate Sensitivity: Why NNNNNN-- Isn't a Beta Play

Critics often argue that REITs are vulnerable to rate hikes, but NNN's business model defies this narrative. Its triple-net leases shift maintenance, insurance, and tax burdens to tenants, creating sticky, inflation-protected cash flows, as shown in the Q3 2025 earnings report. Even if the Fed tightens further, NNN's long-dated debt and stable rental income insulate it from short-term volatility. B. Riley's recent downgrade of NNN's Q3 2025 EPS forecast to $0.84 (from $0.85) is a minor blip, not a red flag-especially when the company's Core FFO and AFFO guidance for 2025 remains intact at $3.34–$3.39 and $3.40–$3.45 per share, respectively, per StockTitan.

Total Return Potential: Dividend Growth Meets Capital Appreciation

NNN's 5.6% yield is tempting, but the real magic lies in its 36th consecutive annual dividend increase, noted by Panabee. The recent hike to $0.60 per share (a 3.4% rise) was funded by a 1.2% year-over-year increase in AFFO per share, according to GuruFocus, proving that management prioritizes balance sheet health. Looking ahead, NNN's net debt to EBITDAre of 5.7x and 4.2x fixed charge coverage ratio, as the PR Newswire release shows, leave ample room for growth. Analysts project 2.8% annual earnings growth and 4.5% revenue growth, per Simply Wall St, suggesting that both the dividend and share price could climb in tandem.

Risks to Consider

No investment is without risk. NNN's 114.29% earnings-based payout ratio, per GuruFocus, highlights a vulnerability: if operating free cash flow turns negative (as it did in Q1 2025 due to capex), as noted by Panabee, earnings volatility could strain the dividend. Additionally, a Trump-backed economic strategy-should it materialize-might alter capital costs or tenant behavior, which the Q3 2025 earnings report also discusses. However, these are speculative headwinds, not immediate threats.

Final Verdict: Buy for the Long Haul

In a world where bond yields are rising and equity markets are jittery, NNN REITNNN-- offers a rare combination of high yield, stable cash flows, and defensive balance sheet strength. Its AFFO-based payout ratio is conservative, its debt structure is bulletproof, and its triple-net model is a hedge against inflation. For income-focused investors willing to hold for five years or more, NNN is a buy, not a gamble. Just don't let the 114% earnings ratio fool you-focus on the 68% AFFO number, and you'll sleep soundly.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet