Can NFLX's Content Strength Sustain User Engagement & Revenue Growth?

Netflix’s NFLX content strength remains the primary engine driving user engagement and revenue growth. The company is seeing strong traction from originals, with branded content viewing rising 9% year over year in the second half of 2025, driven by blockbuster titles and a globally diverse slate. This depth of content fuels higher engagement, which management links to improved retention, lower churn and stronger customer satisfaction — key drivers of sustainable revenue growth. Notably, users watched more than 96 billion hours of content during the period.

Netflix’s strategy increasingly emphasizes the “quality of engagement,” with high-impact titles building fandom, boosting word-of-mouth acquisition and strengthening pricing power. This underscores content as a long-term value multiplier rather than a cost center. The company is also expanding into live events, documentaries and emerging formats like video podcasts, enhancing platform stickiness.

A strong global slate featuring series and films such as Love on the Spectrum Season 4, XO, Kitty Season 3 and Man on Fire, along with movies like The Giant Falls and Feel My Voice, is likely to sustain high engagement levels. Looking ahead, a solid 2026 pipeline — including marquee titles like Bridgerton S4, ONE PIECE S2, The Night Agent S3, 3 Body Problem S2 and Lupin Part 4 — reflects Netflix’s global, franchise-led strategy. This wide range of content and consistent output reinforces ongoing user engagement and supports long-term revenue growth.

Importantly, content underpins Netflix’s evolving monetization model. Higher engagement supports subscriber growth, enables pricing actions and strengthens its advertising business, which is scaling rapidly. Management’s 2026 revenue guidance of $50.7-$51.7 billion (up 12-14%) reinforces confidence in this content-driven growth model.

Netflix Faces Stiff Competition From Key Rivals

Amazon AMZN and Disney DIS are two strong rivals to NetflixNFLX-- that align closely with Netflix on “content, engagement and retention.”

Amazon competes with Netflix through a content-plus-ecosystem strategy that boosts engagement and retention. Amazon leverages Prime Video within its broader bundle of e-commerce, fast delivery and services, making content a retention tool. Strong momentum in ad-supported streaming (around 315 million viewers) and live sports like the NFL, along with hit originals such as The Boys and The Rings of Power, continues to boost engagement. This multi-touchpoint approach (commerce + content + ads + AI) gives Amazon a differentiated competitive edge.

Disney stands as a key rival to Netflix, leveraging its strong IP ecosystem to drive engagement and retention. It uses blockbuster films and franchises to boost Disney+ viewership. DIS benefits from hits like Zootopia 2 and Avatar: Fire and Ash, which increase streaming engagement. The company also improves retention through bundling (Disney+, Hulu, ESPN) and new initiatives like unified apps, local content and AI-generated content via Sora.

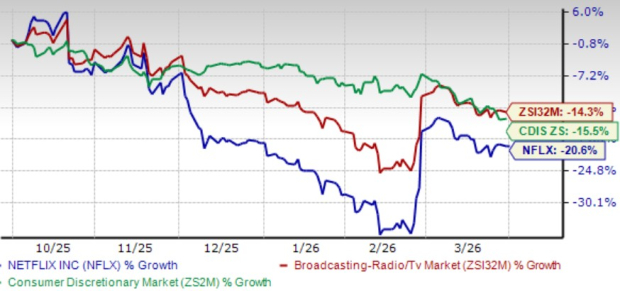

NFLX’s Price Performance, Valuation & Estimates

Shares of Netflix have declined 20.6% in the past six-month period, underperforming both the Zacks Broadcast Radio and Television industry and the Zacks Consumer Discretionary sector’s fall of 14.3% and 15.5%, respectively.

NFLX’s Price Performance

Image Source: Zacks Investment Research

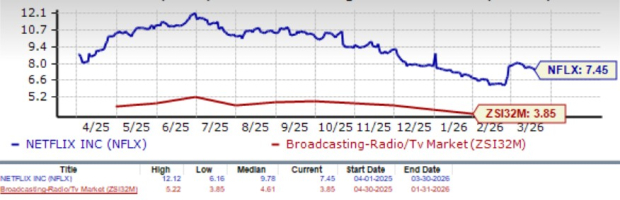

From a valuation standpoint, Netflix appears overvalued, trading at a forward 12-month price-to-sales ratio of 7.45X, higher than the industry's 3.85X. NFLXNFLX-- carries a Value Score of C.

NFLX’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for 2026 earnings is pegged at $3.17 per share, up by 3 cents over the past 30 days. This indicates a 25.3% increase from the previous year.

Image Source: Zacks Investment Research

NFLX currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Netflix, Inc. (NFLX): Free Stock Analysis Report

The Walt Disney Company (DIS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet