Netflix's Earnings Dip: A Buying Opportunity or a Warning Sign?

Netflix's Q2 2025 earnings report was a masterclass in financial execution: revenue surged 16% to $11.08 billion, EPS beat estimates by 1.7%, and free cash flow jumped 91%. Yet the stock fell 5% post-earnings, sparking a debate: Is this a contrarian buying opportunity, or a warning that the market is pricing in perfection?

The Case for Optimism: A House Built on Strong Foundations

Let's start with the fundamentals. Netflix's ability to raise full-year revenue guidance to $44.8–$45.2 billion, driven by pricing power, ad revenue growth (projected to double to $3 billion), and a 94 million ad-tier user base, is no small feat. Its operating margin of 34.1% in Q2, up 7 percentage points year-over-year, shows operational discipline. Even as it warns of margin compression in H2 due to content amortization and marketing costs, the company's cash flow generation remains robust.

For contrarian investors, the selloff might reflect overcorrection. Netflix's ad business is expanding rapidly, and its content slate—Stranger Things finale, Wednesday Season 2, and Guillermo del Toro's Frankenstein—is arguably the strongest in the industry. These hits could drive engagement and retention, countering concerns about stagnant streaming hours.

The Case for Caution: Valuation and Macro Risks

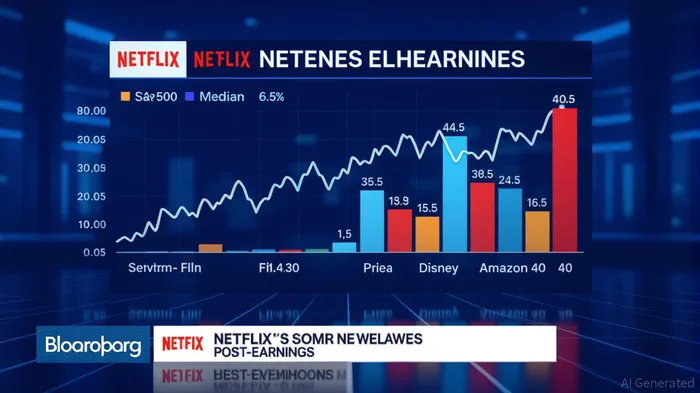

But let's not ignore the red flags. At a forward P/E of 44.5 and a PEG ratio of 1.8, NetflixNFLX-- trades at a premium to both historical norms and peers like DisneyDIS-- (P/E 35) and AmazonAMZN-- (P/E 40). The market is pricing in continued 30%+ EPS growth, a bar that's hard to clear when engagement growth is “anemic” at 1% year-over-year.

The macro environment adds another layer of risk. With interest rates remaining high and consumers tightening budgets, Netflix's margin warnings for H2—driven by a $2.5 billion content slate—could strain profitability. The lack of a sports strategy, a key growth lever for platforms like Disney and Peacock, also leaves Netflix exposed in a fragmented streaming landscape.

Contrarian Take: A Calculated Entry Point

Here's where a value investor's lens comes in. Netflix's selloff wasn't triggered by poor performance but by elevated expectations. The stock fell after a 42% YTD gain, and the market's reaction—punishing the company for not “blowing away” estimates—suggests overvaluation, not operational failure.

For long-term investors, this could be a buying opportunity if the fundamentals hold. Netflix's ad business is a $3 billion growth engine, and its global expansion (led by India and Brazil) offers untapped potential. The key is to monitor margin resilience and content ROI. If the second-half slate drives engagement and retention, the dip could be a correction, not a collapse.

However, the valuation remains a hurdle. At 44x forward earnings, Netflix is priced for perfection. A misstep in content execution or a macro downturn could lead to further pain. Diversification is key: Pairing a Netflix position with lower-PEG peers like Disney or Amazon might balance risk.

Final Verdict: Proceed with Prudence

Netflix's earnings dip is a textbook example of a market overreacting to a “good but not great” report. The company's financials are strong, but its valuation and macro risks demand caution. For contrarian investors, this could be an entry point—if you're willing to bet that the content machine can justify the premium. For others, it's a reminder that high-growth stocks often trade on hope, not just fundamentals.

In the end, the answer depends on your risk tolerance. If you believe Netflix can sustain its growth and navigate margin pressures, the dip offers a chance to buy a dominant player at a discount to its potential. But if you're wary of stretched valuations and macro volatility, it's better to sit this one out—and wait for a clearer signal."""

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet