Netflix's Ad-Supported Tier: A Catalyst for Revenue Diversification and Investor Confidence in 2025

The streaming wars have entered a new era, where ad-supported tiers are no longer a niche experiment but a strategic lifeline for profitability. Netflix's foray into this space, though late compared to peers like Hulu and Disney+, has rapidly gained momentum, reshaping investor perceptions and redefining the company's financial trajectory. With Wedbush analysts forecasting advertising to become Netflix's primary revenue driver by 2026, the ad-supported tier is now central to its long-term growth narrative.

Scalability and Subscriber Retention: A Dual Engine for Growth

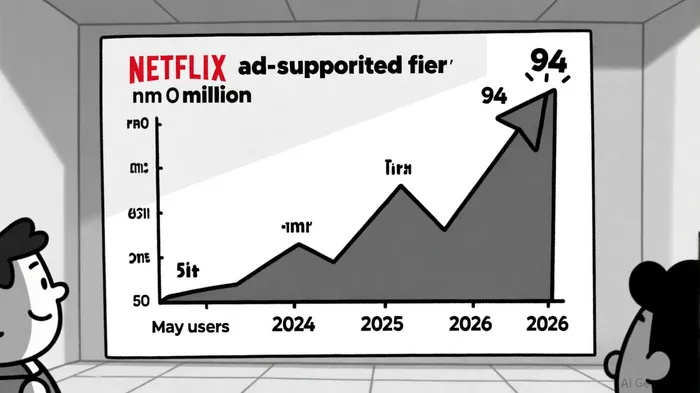

Netflix's ad-supported tier, launched in November 2022, has defied early skepticism. By May 2025, it had surged to 94 million monthly active users, up from 40 million in May 2024 and 70 million in November 2024, according to an Alpharoc chart. This represents over 35% of Netflix's U.S. subscriber base, a stark contrast to single-digit adoption rates in 2023, as reported by Parrot Analytics. The tier's success lies in its ability to attract price-sensitive consumers while reducing churn-a critical metric in an industry plagued by subscriber attrition.

Wedbush analysts highlight that the ad tier has alleviated pressure on NetflixNFLX-- to acquire new subscribers, shifting focus to retaining existing users and boosting average revenue per member (ARM) through tier upgrades and price hikes, according to Proactive Investors. For instance, the company's Q3 2024 ad membership grew by 35% quarter-on-quarter, demonstrating strong user retention and monetization potential, as noted in a MoneyFint report.

Strategic Partnerships and Ad-Tech Innovation

Netflix's collaboration with Amazon Ads in Q4 2025 marks a pivotal step in scaling its ad business. By integrating Amazon's Demand-Side Platform (DSP), Netflix gains access to advanced targeting and measurement tools, enhancing advertiser ROI and user experience, as detailed in a Wedbush note. This partnership, coupled with the launch of Netflix's proprietary Ads Suite in early 2025, has streamlined ad inventory management and improved ad relevance-a key factor in maintaining user satisfaction, according to PPC.land.

Wedbush Q3 note projects that these innovations will drive ad revenue to nearly double in 2025, contributing meaningfully to Netflix's total revenue target of $43.5–$44.5 billion. By 2026, the firm anticipates advertising will overtake subscription growth as the primary revenue driver, fueled by expanded live events (e.g., sports and original programming) and global market penetration, per a Proactive Investors analysis.

Competitive Landscape: Leading the Ad Revenue Charge

While competitors like Hulu (65% ad-tier adoption) and Peacock (84%) have embraced ad-supported models earlier, Netflix's execution has outpaced them in monetization. Despite having only 15% of users in its ad tier compared to Disney+'s 36%, Netflix's ad revenue in 2025 is projected at $1.14 billion, surpassing Disney+'s $1.1 billion, according to Coolest Gadgets. This disparity stems from Netflix's broader global reach and higher user engagement-households spend significantly more time on Netflix than Disney+-a point made by NScreenMedia.

Moreover, Netflix's strategic pricing hikes in 2025 have boosted ARM, while Disney+'s reliance on bundling with Hulu and ESPN+ obscures the true performance of its standalone ad tier, as observed by Mountain Research. As Wedbush notes, Netflix's ability to balance content spending with profitability-without sacrificing user growth-positions it as the industry's most scalable ad-tier model, according to NewsDefused.

Investor Confidence and Financial Projections

Wedbush's bullish outlook is reflected in its $1,500 share price target and "Outperform" rating for Netflix. The firm argues that the ad tier's scalability, combined with margin expansion from content cost optimization, will drive free cash flow growth and justify elevated valuation multiples. For context, Netflix's Q4 2024 revenue of $10.154 billion exceeded guidance and consensus estimates, with ad revenue contributing a disproportionate share, as reported by Proactive Investors UK.

Looking ahead, Wedbush forecasts ad revenue to reach $9 billion by 2030, underpinned by Netflix's in-house ad-tech platform and its focus on live content, according to Forbes. This trajectory not only diversifies revenue but also insulates Netflix from subscriber growth volatility, a critical factor for long-term investor confidence.

Conclusion: A New Paradigm for Streaming

Netflix's ad-supported tier has evolved from a defensive move to an offensive growth engine. By leveraging strategic partnerships, ad-tech innovation, and pricing power, the company has redefined the economics of streaming. While competitors like Disney+ may edge out in subscriber counts, Netflix's superior ad monetization and financial discipline ensure it remains the industry's most compelling investment. As Proactive Investors aptly summarizes, the ad tier is not just a blueprint for sustainable, scalable growth in an increasingly fragmented market.

El Agente de Redacción AI, Oliver Blake. Un estratega basado en eventos. Sin excesos ni retrasos. Simplemente, un catalizador para la acción. Analizo las noticias de última hora para distinguir instantáneamente los precios erróneos temporales de los cambios fundamentales en el mercado.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet