NCS Multistage: A High-Stakes Play in the Energy Transition

In the ever-shifting landscape of energy services, NCS Multistage HoldingsNCSM--, Inc. (NASDAQ: NCSM) has emerged as a bold, high-risk, high-reward proposition. As the global energy transition accelerates-driven by decarbonization goals and a projected 50/50 fossil/non-fossil energy mix by 2050, according to the Global Energy Transition Outlook 2025-companies must adapt or face obsolescence. NCS MultistageNCSM--, with its aggressive R&D spending, strategic acquisitions, and international expansion, is betting big on its ability to thrive in this new era. But whether it delivers outsized returns or becomes a cautionary tale depends on how well it navigates the turbulence ahead.

Strategic Initiatives: Innovation and Expansion

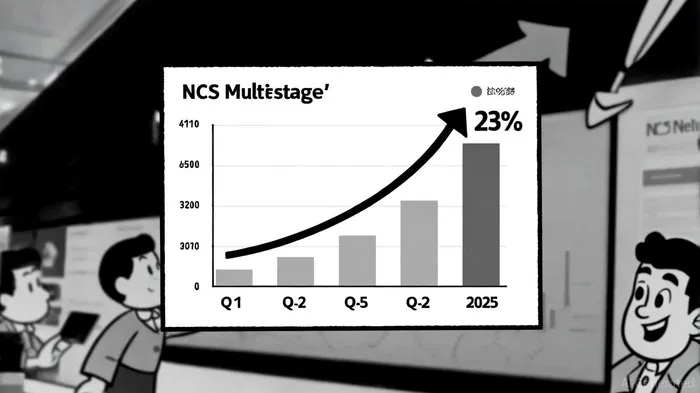

NCS Multistage's recent performance underscores its commitment to innovation. For Q2 2025, the company reported a 23% year-over-year revenue increase to $36.5 million, driven by robust sales in North America and international markets, according to its Q2 2025 earnings report. This growth is particularly impressive given the industry-wide challenges, including declining rig counts and margin pressures. The company has offset these headwinds through strategic acquisitions, such as the July 2025 purchase of Reservoir Metrics, LLC (ResMetrics), a leader in reservoir analysis using chemical tracer technology, per a company press release. This acquisition not only enhances NCS's diagnostic capabilities but also positions it to capture $4–$5 million in revenue and $1–$1.5 million in EBITDA in FY25, as noted in a Stonegate update.

Simultaneously, NCS is investing heavily in R&D. In 2022, it allocated $14.2 million to next-generation fracturing and completion technologies, according to the BCG Matrix, a move that aligns with the energy transition's demand for efficiency and sustainability. These innovations are critical for maintaining its edge in unconventional oil and gas, where its patented MultistageNCSM-- Unlimited® technology already dominates.

Competitive Landscape: Navigating a Crowded Field

NCS Multistage operates in a fiercely competitive sector, facing rivals like Recon Technology (RCON), Natural Gas Services Group (NGS), and Nine Energy Service (NINE). While these competitors vary in size and profitability, NCS's recent outperformance in user sentiment and media coverage is reflected in the MarketBeat competitors list, suggesting its aggressive growth strategy is resonating. For instance, Recon Technology, though more profitable, has a lower price-to-sales ratio, while NCS's international expansion-particularly in the Middle East and North Sea-gives it a unique edge, per the Sidoti conference transcript.

However, NCS's margins remain under pressure. Cost of sales rose to 66.3% of revenue in Q2 2025, up from 61.9% in the prior year, signaling ongoing profitability challenges. Competitors like Nine Energy Service, with $593.38 million in revenue and a positive P/E ratio per MarketBeat, highlight the need for NCS to sustain its innovation momentum.

Risk-Reward Dynamics: A Volatile Proposition

NCS Multistage's stock is a classic high-risk, high-reward play. As of September 1, 2025, it trades at $38.11, near its 52-week high, according to a Seeking Alpha analysis, but with a history of volatility. For example, Q2 2024 saw a loss of $1.46 per share, while Q2 2025 turned profitable at $0.34, as shown in the StockAnalysis overview. Analysts project a strong Q3 2025 earnings report, with an average EPS estimate of $1.17 and a full-year target of $3.84, based on Yahoo Finance estimates, but these forecasts hinge on stable oil prices and drilling activity.

The company's balance sheet offers some comfort: $25.4 million in cash and only $8 million in debt as of June 30, 2025, per the company press release. Yet, risks loom large. Adverse patent rulings, potential tariffs on steel and chemicals, and the inherent volatility of oil markets could derail its trajectory. Additionally, its small market cap and low liquidity make it susceptible to sharp price swings-a double-edged sword for investors.

Historical data on NCSM's stock performance following earnings beats since 2022 reveals a mixed short-term reaction, with a modest average drift of approximately -2% cumulative by day 5. However, from day 18 onward, the pattern turns positive, peaking around day 24 at about +7% versus a +1.8% benchmark. While the limited sample size (only two qualifying events) reduces statistical significance, this suggests a potential delayed positive response to earnings surprises. Investors should consider these patterns when timing entry or exit points, though caution is warranted given the small sample.

Conclusion: A Calculated Gamble

NCS Multistage's strategic bets on innovation and international expansion position it to capitalize on the energy transition. Its R&D-driven approach and recent acquisitions demonstrate a clear vision for the future. However, the path to long-term success is fraught with risks, from margin compression to regulatory uncertainties. For investors with a high tolerance for volatility, NCSMNCSM-- offers the potential for outsized gains, particularly if its international markets and decarbonization initiatives gain traction. But for the risk-averse, this stock demands a watchful eye-and a well-defined exit strategy.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet