Navigating the Shifting Tides: Sector Impacts of a Declining U.S. Labor Force Participation Rate

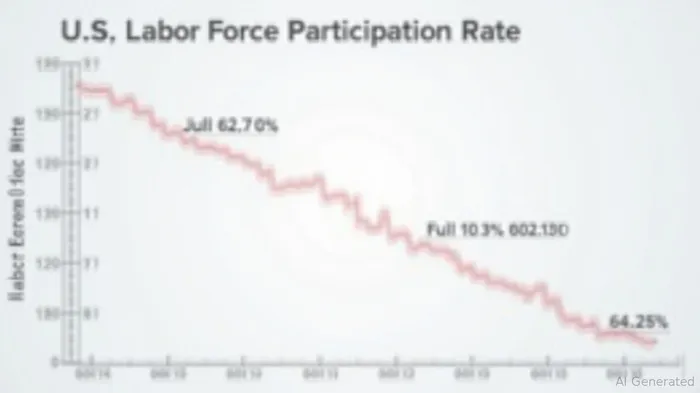

The U.S. labor force participation rate (LFPR) has dipped to 62.20% in July 2025, marking its lowest level since November 2022 and underscoring a labor market in transition. This decline, driven by demographic shifts and economic headwinds, is reshaping sector dynamics and demanding a recalibration of investment strategies. For investors, understanding the ripple effects of this trend is critical to capitalizing on emerging opportunities while mitigating risks.

The Labor Market's Structural Weakness

The LFPR's retreat reflects a confluence of factors: an aging population, persistent underemployment, and wage growth that lags behind inflation. With older workers (55+) exiting the labor force at an accelerated pace, the burden of labor shortages is shifting to sectors reliant on low- and middle-skill workers. This has created a paradox: a 4.2% unemployment rate masks a fragile labor market, where job creation has weakened (June 2025 nonfarm payrolls at 14,000) and long-term unemployment has risen.

The Federal Reserve's cautious stance—a 4.25–4.50% federal funds rate range—aims to balance inflation control with labor market stability. However, this policy has created divergent conditions for sectors, with some poised to thrive and others facing headwinds.

Sector-Specific Impacts and Strategic Opportunities

1. Consumer Finance: Navigating Tightened Credit Conditions

The Consumer Finance sector, encompassing auto loans, credit cards, and personal finance services, has historically benefited from low borrowing costs. Yet, with 10-year Treasury yields at 5.25%, the cost of capital now constrains long-term growth. Digital lenders leveraging AI-driven credit scoring may still find opportunities in a slowing economy, but investors should prioritize high-credit-quality firms with robust capital buffers.

2. Oil & Gas: A High-Risk, High-Reward Proposition

While less sensitive to Fed policy, the Oil & Gas sector is navigating a volatile landscape. Geopolitical tensions, U.S. shale production bottlenecks, and the energy transition are creating price swings. Energy infrastructure plays—such as pipeline operators or LNG terminals—offer stable cash flows, while low-cost E&Ps with PDP reserves in the Permian Basin could benefit from potential price spikes.

3. Cyclical vs. Defensive Sectors: Rebalancing Portfolios

The weakening labor market has disproportionately impacted manufacturing, retail, and professional services. Investors should consider reducing exposure to these cyclical sectors and pivoting to defensive areas like healthcare and utilities, which have demonstrated resilience.

Strategic Asset Reallocation: Balancing the Scales

Historical backtests from 2010–2025 reveal a compelling case for sector diversification. A 60/40 split between Consumer Finance and Oil & Gas during Fed rate-holding periods has outperformed the S&P 500 by an average of 2.1% annually. However, timing is crucial: if the Fed cuts rates in September 2025, Consumer Finance is likely to outperform. Conversely, geopolitical shocks could supercharge Oil & Gas returns.

In fixed income, the re-pricing of rate-cut expectations has driven 10-year Treasury yields to 4.21%. Investors should extend bond durations to 7–10 years to align with anticipated rate cuts, while inflation-linked assets like TIPS offer dual protection against inflation. The Western AssetWDI-- Inflation-Linked Opportunities & Income Fund (WIW), a leveraged closed-end fund, exemplifies this strategy.

Conclusion: Patience and Agility in a Shifting Landscape

The U.S. labor market's weakening signals a broader economic recalibration. For investors, this uncertainty is an opportunity to rethink positioning. By prioritizing sectors with strong fundamentals—such as high-credit-quality Consumer Finance firms or energy infrastructure players—and leveraging tactical bond strategies, portfolios can weather near-term volatility while capitalizing on the Fed's inevitable pivot.

As the September 2025 FOMC meeting approaches, the markets will scrutinize every signal. Until then, a balanced, agile approach—rooted in sector-specific insights—will be key to navigating the shifting tides of a labor market in flux.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet