Navigating the Shift in Student Loan Policy and Its Impact on Financial Markets

The U.S. student loan landscape has undergone seismic shifts in 2025, driven by the termination of the Biden-era , the implementation of the (OBBBA), and the introduction of the Repayment Assistance Plan (RAP). These policy changes have profound implications for asset allocation strategies and risk management practices in education-related sectors, reshaping the financial dynamics for borrowers, institutions, and investors.

Policy Shifts and Their Immediate Implications

The Trump administration's decision to end the SAVE plan through a settlement with GOP-led states has forced existing borrowers into costlier repayment structures, such as (IBR) or the new RAP, which

mandates a minimum $10 monthly payment and extends repayment terms to 30 years. Concurrently, the OBBBA, signed into law in July 2025, has

restructured , eliminated , and imposed stricter borrowing caps for graduate and professional students. These measures aim to curb tuition inflation but

risk exacerbating financial strain on low-income borrowers, particularly in critical fields like healthcare and education.

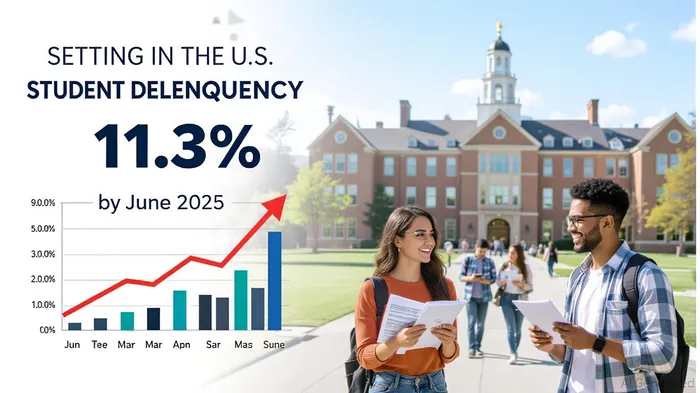

The transition to the RAP, set to begin in July 2026, introduces income-based payment tiers but removes the flexibility of previous income-driven repayment (IDR) plans.

Critics argue this could push borrowers toward default, . Such trends are already evident: by June 2025,

, with borrowers from for-profit institutions and those without completed degrees facing the highest risks.

Asset Allocation Strategies in a Restructured Landscape

Financial institutions are recalibrating their asset allocation strategies to account for heightened default risks and shifting borrower behavior. The phaseout of federal loan programs has spurred increased reliance on private student loans, which now fill the funding gap for students whose federal borrowing is restricted. This shift has

led to a projected rise in private student loan volume, despite higher interest rates and fewer borrower protections compared to federal loans.

For (ABS) tied to private student loans, the 2025-2026 performance metrics reveal mixed signals.

in late 2025, . These figures underscore the growing volatility in the sector, prompting investors to adopt more conservative and diversify their portfolios to mitigate exposure.

Higher education institutions, meanwhile, are reassessing their financial strategies. With federal funding subject to stricter compliance requirements and operational costs rising-driven by inflation and increased demand for mental health and healthcare services-universities are

prioritizing centralized resource management and program realignment. Institutions reliant on federal grants, such as those facing scrutiny under reinterpreted and policies, are particularly vulnerable, with

.

Risk Management and Sector-Specific Challenges

The OBBBA's elimination of Grad PLUS loans and caps on federal borrowing has created sector-specific risks. For example,

graduate nursing and education programs now face potential as access to funding dwindles. Financial institutions are responding by tightening terms for private loan coverage and

increasing premiums for institutions exposed to high-risk liabilities, such as cyber threats or litigation.

Risk-sharing mechanisms, inspired by Brazil's model, have emerged as a potential solution to align institutional incentives with borrower outcomes. While the OBBBA did not adopt such provisions, the concept remains influential in shaping risk management frameworks.

to repayment rates, these models encourage improved program quality and student retention.

For investors, the growing complexity of student loan portfolios necessitates enhanced due diligence.

The Federal Reserve's 2025 Economic Well-Being of U.S. Households report highlights that borrowers with lower incomes and less education are disproportionately affected by delinquency and default trends. This demographic skew requires tailored risk assessments, particularly for backed by private loans, which

lack the federal safeguards of their public counterparts.

Market Trends and Forward-Looking Considerations

The interplay of policy shifts and market dynamics is reshaping the education sector's financial landscape. By 2026, the RAP's implementation will likely amplify default risks, . Financial institutions are advised to strengthen compliance programs and

to monitor lending practices and mitigate non-compliance risks.

For asset allocators, the key challenge lies in balancing exposure to education-related sectors with the sector's heightened volatility. While private student loan ABS offer higher yields, their performance remains contingent on borrower repayment capacity and macroeconomic conditions. Conversely, institutions with robust risk management frameworks and diversified revenue streams may present more stable investment opportunities.

Conclusion

The 2025 student loan policy changes represent a tectonic shift in the U.S. education finance ecosystem. As federal support contracts and private lending expands, asset allocation strategies must evolve to address rising default risks, regulatory uncertainties, and sector-specific vulnerabilities. For investors, the path forward demands a nuanced understanding of borrower behavior, institutional resilience, and the broader economic forces shaping the sector.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet