Navigating Q4 2025 Market Volatility: Strategic Sector Rebalancing in a Shifting Macro Landscape

The Q4 2025 market environment is a high-stakes chessboard, where tariffs, inflation, and central bank policy shifts are reshaping the rules of the game. According to a CBO report, global GDP growth clocked in at 2.3% quarter-over-quarter annualized in Q4 2025, driven by a consumer-led surge in durable goods spending as households stockpiled ahead of anticipated tariff-driven price hikes CBO report. Yet, this resilience masks deeper fissures: the CBO warns that 2025 growth is 0.5 percentage points below earlier forecasts, with tariffs and reduced immigration dragging on long-term potential.

The Macro Tightrope: Tariffs, Inflation, and Policy Uncertainty

The U.S. tariff regime has become a double-edged sword. While it has boosted domestic manufacturing demand, it has also inflated goods prices by 1.9% above pre-2025 trends, particularly in electronics and appliances AB outlook. Meanwhile, the Federal Reserve's cautious stance-holding rates steady in H1 2025-reflects a delicate balancing act. As stated by S&P Global, policy uncertainty remains a drag on economic resilience, even as trade policy clarity in Q3 2025 offered a temporary reprieve.

The IMF forecasts global inflation to decline to 3.0% in 2025 and 3.1% in 2026, but U.S. inflation remains stubbornly above target at 4.2% IMF forecast. This divergence has pushed institutional investors to hedge with commodities like gold and copper, which have surged amid macroeconomic turbulence, the AB outlook notes.

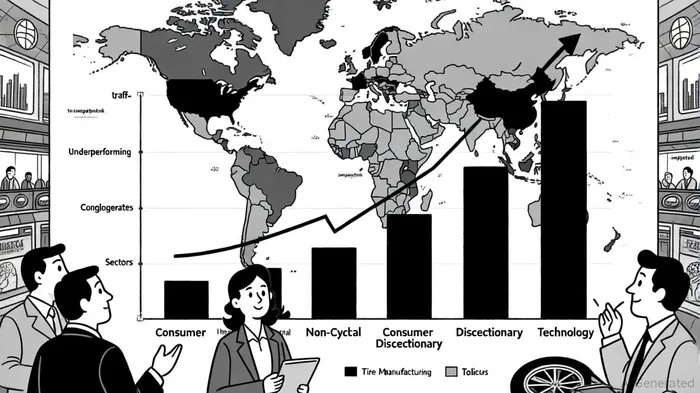

Sector Rotation: Winners, Losers, and the AI Tailwind

The equity sector landscape in Q4 2025 tells a tale of two Americas. Consumer Non-Cyclical (15.82%) and Consumer Discretionary (15.12%) sectors led the charge, fueled by tariff-driven demand and pent-up consumer spending CSIMarket data. The Technology sector, bolstered by the AI boom, delivered a robust 21.09% return, with companies investing heavily in AI infrastructure Morningstar.

However, not all sectors fared well. Conglomerates (-5.33%) and Tire Manufacturing (-16.90%) lagged, hit by supply chain disruptions and margin compression from tariffs, according to CSIMarket. Energy and industrials, while cyclical, remain under pressure from mixed demand signals and geopolitical risks Permutable.ai.

Rebalancing for Resilience: A Cramer-Style Playbook

Given this volatile backdrop, portfolio rebalancing must prioritize adaptability. Here's how to position for Q4 2025:

Embrace Cyclical Pockets: Overweight sectors poised to benefit from Fed rate cuts, such as Capital Goods (9.54% return) and REITs, which have outperformed in Q4. Invesco's Q4 2025 outlook recommends maintaining an overweight in China equities and short-duration corporate bonds Invesco outlook.

Hedge with Commodities: Allocate to gold and copper to offset inflationary pressures. These assets have historically served as safe havens during policy-driven volatility, as noted in the AB outlook.

Tax-Smart Rebalancing: Utilize tax-loss harvesting in taxable accounts, particularly in underperforming sectors like Conglomerates. Charitable donations of appreciated stocks can also mitigate capital gains taxes Welch Group guide.

Short-Duration Fixed Income: With the yield curve expected to steepen, prioritize short-duration bonds for yield advantage. Corporate investment-grade debt, especially in emerging markets, offers a compelling risk-return profile, the Invesco outlook suggests.

Stay Nimble on Tech: While U.S. equities trade at high valuations, AI-driven tech earnings remain resilient. However, avoid overexposure to overhyped subsectors without sustainable cash flows, as Morningstar outlines.

The Bottom Line: Balancing Risk and Reward

The Q4 2025 market demands a blend of tactical agility and long-term vision. As the Fed edges toward rate cuts and global growth stabilizes, investors should focus on sectors with pricing power and defensive characteristics. Yet, the specter of policy unpredictability-whether through new tariffs or fiscal interventions-means diversification and liquidity remain non-negotiable.

In this environment, the mantra is clear: "Buy the dip, but don't chase the rip." Position your portfolio to capitalize on the AI tailwind and cyclical rebound, but keep a weather eye on the macro horizon. After all, in markets as in life, the only certainty is uncertainty.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet