Navigating Mortgage Rate Volatility: Strategic Asset Allocation in a Shifting Interest Rate Environment

The U.S. housing market is at a crossroads. Mortgage rates, , are reshaping homeowner behavior and investor strategies. This shift, driven by weak labor market data and expectations of Federal Reserve rate cuts, has created a complex landscape where affordability challenges persist alongside pockets of opportunity. For investors, the key lies in strategic asset allocation—leveraging the interplay between mortgage rate volatility, refinancing demand, and sector-specific dynamics to build resilient portfolios.

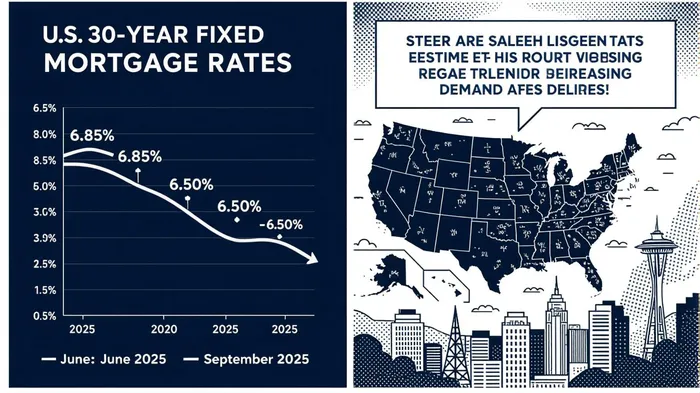

The Drivers of Mortgage Rate Volatility

The recent decline in mortgage rates is rooted in a confluence of economic signals. The July 2025 jobs report, , and downward revisions to prior months' data, signaled a weakening labor market. . By mid-August, , , .

The Fed's dual mandate—balancing inflation control with employment stability—has become a tightrope. , the labor market's deterioration has shifted the central bank's calculus. Analysts now project three rate cuts in 2025, . This creates a paradox: a weaker economy could lead to lower borrowing costs, but it also raises risks of prolonged affordability challenges for homebuyers.

Refinancing Demand and Housing Market Dynamics

The drop in rates has reignited refinancing activity, though its impact on the broader housing market remains muted. Homeowners with mortgages from the 2020–2021 period—many locked in at historic lows—remain hesitant to sell, . Meanwhile, urban centers with strong employment growth, such as Austin and Seattle, are seeing a modest uptick in demand.

For investors, this environment demands a nuanced approach. Single-family home purchases remain constrained by affordability, but multifamily properties and secondary markets offer more stable cash flow. , but this hinges on inventory adjustments and continued rate declines.

Strategic Allocation in Real Estate and Mortgage-Backed Securities

The shifting rate environment has created divergent opportunities across real estate and mortgage-backed securities (MBS):

Multifamily and Secondary Markets:

With single-family home inventory tight, investors are pivoting to multifamily assets and secondary markets. These properties offer predictable rental income streams, particularly in regions with demographic tailwinds. For example, Southern California's affordability crisis has driven demand for affordable housing, while overcorrecting markets like Miami and Atlanta face oversupply risks.(MBS):

Agency RMBS (government-backed securities) have become a defensive play, offering yields in a low-rate environment. Non-agency RMBS, though riskier, present opportunities due to wider spreads and improving credit fundamentals. Duration management is critical here: short-duration MBS benefit from refinancing activity, while long-duration tranches face prepayment risks.Geographic Arbitrage and Niche Sectors:

Investors are capitalizing on geographic arbitrage, , . , .

Hedging and Sector Tilts

Given the uncertainty around Fed policy and economic moderation, hedging strategies are essential. . Similarly, .

For real estate investors, a shift from capital gains to cash flow is prudent. (DSCR) loans, which prioritize rental income over personal borrowing capacity, enable scaling in a high-rate environment. Meanwhile, regional banks with heavy commercial real estate (CRE) exposure, particularly in office sectors, face heightened vulnerability. .

Conclusion: Balancing Growth and Defense

The 2025 mortgage rate decline, while modest, signals a pivotal shift in housing and financial market dynamics. . Strategic asset allocation—focusing on cash flow, geographic diversification, and hedging—will be key to capturing opportunities in real estate and MBS.

As mortgage rates approach the psychologically significant 6% threshold, . For now, the path forward requires agility, a focus on defensive yields, and a willingness to capitalize on sector-specific imbalances. In this environment, the most successful investors will be those who balance growth opportunities with prudent risk management.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet