Navigating Market Volatility Amid Trump's Tariff Deadline and Central Bank Policy Shifts

The global financial landscape in 2025 is defined by two seismic forces: the impending enforcement of Donald Trump's reciprocal tariffs and the Federal Reserve's cautious recalibration of monetary policy. As the August 1, 2025, deadline for tariff implementation looms, markets are bracing for a new era of policy-driven volatility. For investors, the challenge is clear: how to navigate this uncertainty while preserving capital and capitalizing on emerging opportunities. The answer lies in strategic asset allocation, a disciplined approach that leverages sector rotation, defensive equities, and macroeconomic hedging tools.

The Tariff Deadline: A Catalyst for Structural Shifts

The Trump administration's 2025 tariff regime—ranging from 10% on smaller economies to 15% on major trading partners like the EU—has already begun reshaping global supply chains. U.S. Customs will begin collecting these tariffs on August 1, 2025, with no extensions granted. While the EU and Japan have secured temporary deals (e.g., the EU's $750 billion energy purchase and $600 billion investment pledge), countries like Brazil and China remain uncooperative, threatening retaliatory measures.

The impact on corporate earnings is stark. Manufacturing and agriculture sectors, already strained by rising input costs, face margin compression. CaterpillarCAT-- and DeereDE-- have issued profit warnings, while TeslaTSLA-- and GMGM-- have withdrawn guidance. Meanwhile, logistics firms like UPSUPS-- and DHL are thriving, leveraging fragmented supply chains to expand their U.S.-centric infrastructure. This duality underscores the importance of sector rotation: exiting overexposed industries (e.g., industrials, agribusiness) and pivoting to resilient ones (e.g., logistics, AI-driven supply chain tech).

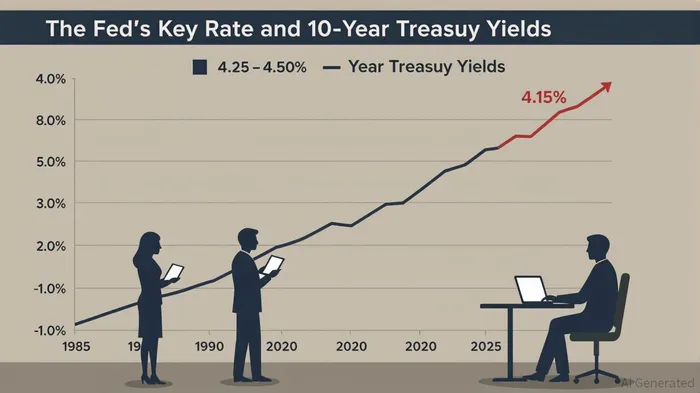

Fed Policy: A Delicate Balancing Act

The Federal Reserve's response to this environment has been measured but not passive. Despite Trump's public pressure to cut rates, the Fed has maintained its benchmark rate at 4.25–4.50%, prioritizing inflation control over political expediency. Q2 2025 data reveals a tightening labor market (unemployment at 4.2%) and moderating inflation (core PCE at 2.8%), but the Fed remains wary of stagflation risks from tariffs.

The Fed's Summary of Economic Projections (SEP) now forecasts GDP growth of 1.4% for 2025, down from 1.9% in Q1, with two rate cuts anticipated in 2025. However, the “dot plot” of FOMC members has shifted toward a hawkish bias, with eight policymakers expecting fewer than two cuts. This uncertainty complicates asset pricing, as investors grapple with the Fed's dual mandate of controlling inflation while avoiding a recession.

Strategic Allocation: Hedging Policy-Driven Risks

To thrive in this environment, investors must adopt a multi-pronged strategy:

- Sector Rotation:

- Exit Vulnerable Sectors: Manufacturing (e.g., Caterpillar), agriculture (e.g., Cargill), and energy (e.g., ExxonMobil) face near-term headwinds from tariffs and retaliatory measures.

Enter Resilient Sectors: Logistics (DHL, FedEx), AI-driven supply chain tech (JDA Software), and defensive utilities (NextEra Energy) offer downside protection.

Defensive Equities:

High-dividend sectors like healthcare (Johnson & Johnson, UnitedHealth) and utilities (Dominion Energy) provide stable cash flows and lower volatility. These assets act as a buffer against trade-war-related downturns.Macro Hedging Tools:

- Treasuries: U.S. bonds (e.g., 10-year yields at 4.1%) offer a safe haven as inflation stabilizes. A 5% yield on corporate bonds (as of June 2025) also provides income without excessive risk.

Commodities: Gold (currently $2,300/oz) and copper (a proxy for global demand) hedge against currency devaluation and inflation.

Geographic Diversification:

International equities (MSCI EAFE at 14.7X forward P/E) and emerging markets (MSCI EM at 12.5X) offer undervalued opportunities. A weaker U.S. dollar (DXY index at 103) enhances returns for U.S.-based investors in foreign assets.

Proactive Rebalancing: The Case for Discipline

The Q2 2025 data underscores the need for proactive rebalancing. For instance, the S&P 500's 18.6% rebound from April's -15.3% low highlights the market's capacity to recover but also its susceptibility to overcorrection. Investors who rotated into defensive sectors and fixed income during the selloff were rewarded with resilience.

A 60/40 equity/bond portfolio, augmented with 10% in commodities and 5% in international equities, could balance growth and safety. For example, a $1 million portfolio might allocate:

- 40% U.S. large-cap (S&P 500 ETFs)

- 15% International equities (EAFE ETFs)

- 10% Defensive equities (utilities, healthcare)

- 20% U.S. Treasuries and corporate bonds

- 10% Commodities (gold, copper)

- 5% Cash reserves

Conclusion: Navigating the Crossroads

The convergence of Trump's tariff deadline and Fed policy shifts creates a high-stakes environment for investors. While the U.S. economy remains resilient, the risks of stagflation and trade wars demand a proactive, diversified approach. By rotating into defensive sectors, leveraging macro hedging tools, and maintaining geographic diversification, investors can mitigate policy-driven volatility and position themselves to capitalize on the inevitable recalibrations in 2025 and beyond. The key takeaway? In a world of uncertainty, adaptability is the ultimate asset.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet