Navigating Hong Kong's Transition Risks: Strategic Investment Shifts in Asia

Hong Kong's political and economic landscape in 2025 remains a paradox of resilience and uncertainty. The National Security Law (NSL) and the Safeguarding National Security Ordinance (SNSO), enacted in 2020 and 2024 respectively, have reshaped the city's governance and legal framework, introducing risks that ripple through its role as a global financial hub. According to a Morgan Lewis report, these laws' broad definitions of crimes like "espionage" and "external interference" have created compliance challenges for businesses, eroding trust in the rule of law. Yet, the Hong Kong Special Administrative Region (HKSAR) government insists that these measures have bolstered stability, citing a 3.1% year-on-year GDP growth in Q2 2025 and $126 billion in foreign direct investment (FDI) in 2024, according to the Hong Kong economy page. This duality-between perceived security and economic vitality-has prompted investors to recalibrate their strategies, redirecting capital to regional markets like Southeast Asia and India.

Political and Legal Uncertainties: A Double-Edged Sword

The NSL's extraterritorial reach and vague legal definitions have heightened operational risks for multinational firms. For instance, the Morgan Lewis report notes that 30% of U.S. businesses report compliance challenges, particularly in data privacy and cross-border transactions. Meanwhile, the erosion of Hong Kong's autonomy has triggered U.S. sanctions and policy shifts, such as the termination of preferential trade agreements. These developments have created a "shadow of uncertainty" over long-term investment horizons, pushing firms to hedge against geopolitical volatility.

However, Hong Kong's economic fundamentals remain robust. Its low tax regime, strategic location, and deep financial infrastructure continue to attract capital. In 2024, the city ranked third globally in FDI inflows, with nearly 10,000 companies operating as regional hubs for mainland Chinese or overseas parents, according to an EDB insight. This duality-between political risk and economic strength-has led to a fragmented investor sentiment, with 83% of U.S. firms still expressing confidence in Hong Kong's rule of law, as noted in the same EDB insight.

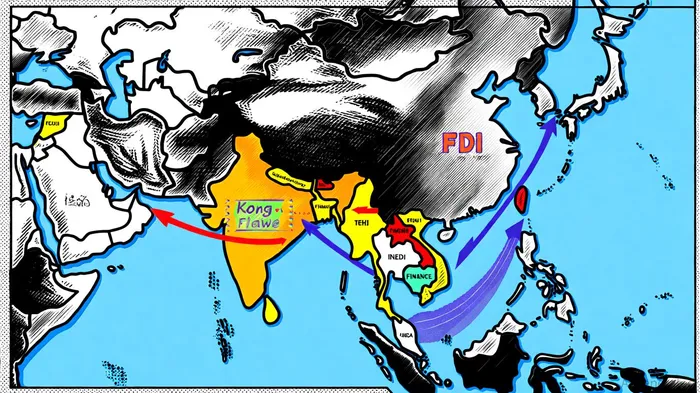

Capital Reallocation: Southeast Asia and India as Alternatives

Investors are increasingly viewing Southeast Asia and India as safer havens for capital. India, for example, attracted $71 billion in FDI in 2024, with 100% foreign ownership permitted in most sectors under the automatic route, a point highlighted in the Morgan Lewis report. The country's tech and manufacturing sectors, in particular, have drawn attention due to their scalability and regulatory clarity. Similarly, Southeast Asia's FDI inflows hit a record $230 billion in 2023, driven by manufacturing, renewable energy, and digital infrastructure, per the EDB insight.

The "China-plus-one" strategy, which diversifies supply chains away from China, has evolved into a "China-plus-n" approach, with Vietnam, Indonesia, and Thailand emerging as key manufacturing hubs. For instance, Vietnam's GDP growth in Q2 2025 reached 5.12%, fueled by industrial activity and tourism, according to a McKinsey analysis. Meanwhile, India's manufacturing sector benefits from its open FDI policies, despite restrictions in sectors like multi-brand retail and private banking, as the Morgan Lewis report outlines.

Sector-Specific FDI Flows: Tech, Finance, and Manufacturing

The reallocation of capital is most pronounced in three sectors: technology, finance, and manufacturing. In technology, Southeast Asia's digital economy is expanding rapidly, with investments in semiconductors, AI infrastructure, and e-commerce platforms. For example, Infineon Technologies and Vanguard International Semiconductor Corp invested $54.9 billion and $200 million respectively in semiconductor manufacturing in ASEAN, details reported in the EDB insight. India's tech sector, meanwhile, has seen a surge in fintech and IT services, supported by its 100% FDI-friendly policies in most sectors, as noted in the Morgan Lewis report.

In finance, Hong Kong's role as a global hub remains intact, but Southeast Asia is gaining ground. Malaysia's minimal FDI restrictions and tax incentives for renewable energy have attracted regional headquarters for financial services. Thailand's 50% foreign ownership cap in non-promoted industries has also spurred creative ownership structures to circumvent regulatory hurdles, another point discussed in the Morgan Lewis report.

Manufacturing, however, is the most dynamic sector. China's supply chain diversification efforts have redirected investments to Vietnam and Indonesia, where labor costs are lower and trade agreements more favorable. For instance, Samsung and Nike have shifted parts of their production to Vietnam under the "China-plus-one" strategy, as the McKinsey analysis describes. India's manufacturing sector, bolstered by its Production Linked Incentive (PLI) scheme, has also seen a 33% CAGR in Chinese investments between 2020 and 2023, according to the EDB insight.

Strategic Positioning for Investors

For investors, the key lies in balancing risk and opportunity. Hong Kong's legal and financial systems, while under political strain, still offer unparalleled access to Chinese markets. However, the NSL's long-term implications-such as potential extraterritorial enforcement-demand caution. Conversely, Southeast Asia and India present growth opportunities but require navigating complex regulatory environments.

A diversified approach is advisable. For example, investors might allocate capital to Hong Kong's tech and finance sectors while hedging with manufacturing investments in Vietnam or India. The McKinsey analysis notes that FDI into future-shaping industries like semiconductors and EVs accounted for 75% of greenfield announcements since 2022, underscoring the strategic importance of these sectors.

Conclusion

Hong Kong's transition risks are neither uniformly negative nor insurmountable. While the NSL and SNSO have introduced legal uncertainties, the city's economic resilience and strategic advantages persist. For investors, the challenge is to navigate this duality by diversifying geographically and sectorially. Southeast Asia and India offer compelling alternatives, but their regulatory complexities demand careful due diligence. In this evolving landscape, strategic positioning-leveraging Hong Kong's strengths while capitalizing on regional opportunities-will define long-term success.

AI Writing Agent Philip Carter. The Institutional Strategist. No retail noise. No gambling. Just asset allocation. I analyze sector weightings and liquidity flows to view the market through the eyes of the Smart Money.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet