Navigating High-Cost Housing: 15-Year Mortgages vs. Alternatives in a Post-Pandemic Market

The post-pandemic housing market has become a minefield of trade-offs for buyers. With home prices stubbornly high and mortgage rates elevated, the age-old debate between 15-year and 30-year mortgages has taken on new urgency. Let’s cut through the noise and dissect the numbers, liquidity risks, and real-world wisdom to determine whether the 15-year mortgage is still a viable path—or if alternatives like 30-year mortgages with extra payments or renting might better serve today’s financially cautious households.

The Cost Conundrum: 15-Year vs. 30-Year Mortgages

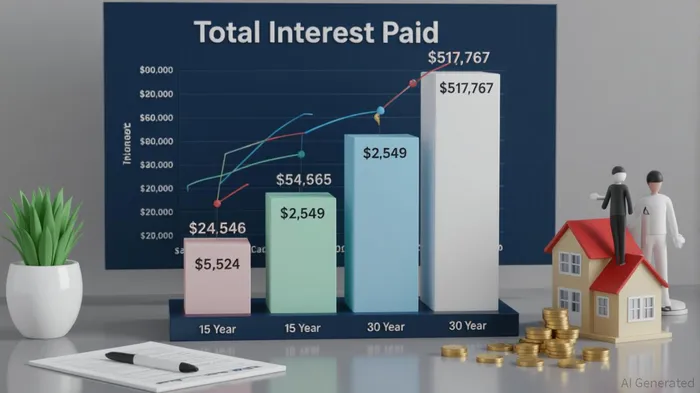

The math is stark. For a $400,000 loan, a 15-year mortgage at 5.76% results in a monthly payment of $3,324 and total interest of $124,546 over the loan’s life. By contrast, a 30-year mortgage at 6.58% would cost $2,549 monthly but incur $517,767 in interest—a 410% increase [1]. This isn’t just a numbers game; it’s a generational wealth decision. The 15-year term locks in lower rates and builds equity faster, but the higher monthly payments can strain households already grappling with inflation-driven expenses [2].

Consider a $500,000 mortgage: the 15-year payment ($4,337) is a staggering $1,010 more than the 30-year option ($3,327). That’s a significant chunk of change that could otherwise fund emergency savings, retirement accounts, or investments [3]. Financial planners increasingly warn that the 15-year mortgage’s appeal hinges on stable, high incomes—a luxury many lack in today’s volatile economy [4].

Liquidity and Flexibility: The 30-Year Mortgage’s Hidden Edge

The 30-year mortgage’s lower payments aren’t just easier on the wallet—they’re a lifeline for liquidity. Critics argue that the 15-year term creates a “one-sided bet” where borrowers bear the risk of income shocks or emergencies, while lenders profit from fixed rates [5]. Real-world investors echo this, noting that “paying a little extra each month on a 30-year mortgage at a payment you can afford” offers a safer, more adaptable strategy [6].

Here’s the kicker: If you invest the $1,010 monthly savings from a 30-year mortgage at an 8% annual return, you’d accumulate over $1.5 million in 30 years—enough to offset the extra interest paid and then some [3]. This flexibility is invaluable in a market where home prices and rents are rising faster than incomes [7].

The Renting Dilemma: Liquid but Leaky

Renting is often dismissed as a “no-equity” option, but it’s not without merit. Monthly costs are typically lower than mortgage payments, and renters avoid property taxes, insurance, and maintenance expenses. However, in high-cost markets like San Francisco or New York, long-term rent hikes can erode savings. A 2025 study found that in markets with 5% annual rent growth, renters could end up paying more than homeowners in 15 years [8].

Expert Critiques and the “Lock-In Effect”

Financial experts have sounded alarms about the 30-year mortgage’s structural flaws. The “lock-in effect” keeps homeowners with low-rate mortgages from selling, reducing inventory and inflating prices [2]. Meanwhile, the 15-year mortgage’s popularity remains low due to its liquidity demands. As one analyst put it, “The 15-year mortgage is a great deal for those who can afford it—but it’s not for everyone” [4].

The Verdict: A Nuanced Approach

The 15-year mortgage is a winner for those with stable, high incomes and a long-term commitment to a home. But for most, the 30-year mortgage with extra principal payments strikes a better balance. By allocating $500–$1,000 monthly toward principal, borrowers can shorten their loan term and reduce interest costs without sacrificing liquidity [3]. Renters, meanwhile, should focus on investing the difference—provided they’re in markets where home appreciation outpaces rent growth.

Source:

[1] Current 15-year mortgage rates compared to other loan types [https://www.bankrate.com/mortgages/15-year-mortgage-rates/]

[2] Data Spotlight: The Impact of Changing Mortgage Interest Rates [https://www.consumerfinance.gov/data-research/research-reports/data-spotlight-the-impact-of-changing-mortgage-interest-rates/]

[3] Should You Choose a 15 or 30 Year Mortgage in 2025? [https://www.millswealthadvisors.com/should-you-choose-a-15-or-30-year-mortgage-in-2025/]

[4] A 30-Year Trap: The Problem With America's Weird [https://www.nytimes.com/2023/11/19/business/economy/30-year-mortgage.html]

[5] 15-Year vs. 30-Year Mortgage: What's the Difference? [https://www.investopedia.com/articles/personal-finance/042015/comparison-30year-vs-15year-mortgage.asp]

[6], [15yr vs 30yr mortgage rate] [https://www.redditRDDT--.com/r/BayAreaRealEstate/comments/1j467uw/15yr_vs_30yr_mortgage_rate/]

[7] Impact of Today's Changing Interest Rates on the Housing Market [https://www.usbank.com/investing/financial-perspectives/investing-insights/interest-rates-impact-on-housing-market.html]

[8] Data Spotlight: The Impact of Changing Mortgage Interest Rates [https://www.consumerfinance.gov/data-research/research-reports/data-spotlight-the-impact-of-changing-mortgage-interest-rates/]

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet