Navigating the Fed's Extended Pause: Strategic Fixed-Income Plays in a Low-Growth World

The Federal Reserve's fourth consecutive decision to hold interest rates steady in June 2025 marks a pivotal shift in monetary policy, signaling a prolonged period of caution amid simmering economic uncertainties. With GDP growth projected at just 1.4% for 2025 and inflation remaining stubbornly above targets, the Fed has opted to prioritize stability over aggressive tightening or easing. This pause creates a unique opportunity for fixed-income investors to recalibrate portfolios toward high-quality bonds, duration strategies, and sector-specific plays that capitalize on the evolving yield environment. Below, we dissect the implications of this policy pivot and outline actionable strategies for navigating the next phase of the cycle.

The Fed's Message: Caution Amid Crosscurrents

The June policy statement emphasized a “solid pace of economic growth,” yet underscored lingering risks from stagflationary pressures and geopolitical instability. With the federal funds rate anchored at 4.25%-4.5%, the Fed's median projection now calls for two rate cuts by year-end 2025, followed by gradual declines to 3.0% by 2027. This dovish tilt reflects growing concerns about a slowdown in consumer spending and business investment, even as labor markets remain resilient.

The yield curve's flattening trajectory—driven by expectations of near-term cuts—has created a tactical opening for duration-sensitive strategies. Investors can exploit the steepness of the far end of the curve by overweighting intermediate- and long-term bonds, which typically outperform when rates stabilize or decline.

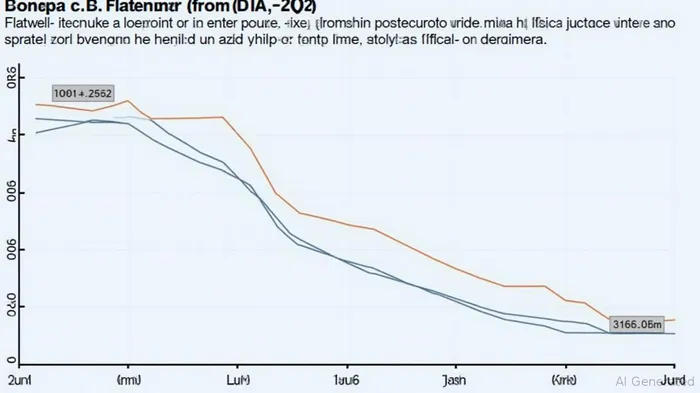

Yield Curve Dynamics: Duration as a Growth Hedge

The Fed's extended pause has stabilized the front end of the yield curve, while the long end reflects discounted expectations of easing. This environment rewards investors who can navigate the “sweet spot” of maturities where yield pickup outweighs duration risk. For instance, 7- to 10-year Treasuries currently offer a 3.6% yield—compared to 5.1% for 2-year notes—providing a compelling risk-reward trade-off if inflation continues to moderate.

The narrowing spread between these maturities highlights the market's pricing of an eventual rate cut. However, investors must remain vigilant to geopolitical shocks or inflation surprises that could steepen the curve again.

Credit Spreads: Opportunities in Investment-Grade and Munis

While high-yield bonds have underperformed in 2025 due to credit concerns, investment-grade corporates and municipal bonds present safer yield-enhancement avenues. The BAML US Corporate BBB Option-Adjusted Spread has tightened to 190bps—a premium to Treasuries that compensates for moderate default risk but remains attractive relative to historical averages.

Municipal bonds, meanwhile, benefit from tax-free yields and strong demand from individual investors. The 10-year muni/Treasury ratio currently stands at 82%, offering a 2.2% yield versus 3.6% for Treasuries—a compelling trade for those in high tax brackets.

Laddered Strategies: Mitigating Rate and Liquidity Risks

A laddered bond portfolio—diversified across maturities from 1 to 10 years—can smooth reinvestment risk and provide steady cash flow. By staggering maturities, investors avoid being locked into long-dated bonds if rates decline faster than expected, while still capturing higher yields on longer tenors. For example, a 5-year ladder weighted 40% in 3- to 5-year Treasuries and 30% in 7- to 10-year corporates could generate a 3.8% yield with manageable volatility.

Risks: The Fed's Tightrope Walk

While the pause presents opportunities, it also underscores the Fed's balancing act between fighting inflation and supporting growth. Key risks include:

1. Policy Missteps: Overly aggressive cuts could reignite inflation if labor markets remain tight.

2. Geopolitical Spillover: Middle East conflicts or trade disputes could disrupt commodity markets, raising input costs.

3. Credit Downgrades: A slowdown in revenue growth for corporates could pressure BBB-rated issuers.

Investment Recommendations

- Overweight Intermediate-Term Treasuries (e.g., 5- to 7-year maturity) for their yield and duration profile.

- Rotate into Munis: Focus on high-quality state bonds with low debt-to-GDP ratios (e.g., Texas, Colorado).

- Ladder Investment-Grade Corporates: Target sectors like utilities and healthcare, which benefit from stable cash flows.

- Avoid High-Yield and Emerging Markets: Until credit spreads stabilize and default rates decline.

Conclusion

The Fed's extended pause has transformed fixed-income markets into a battleground for strategic allocators. By prioritizing quality, duration flexibility, and sector-specific opportunities, investors can position portfolios to thrive in a low-growth environment. However, the path ahead hinges on navigating policy crosscurrents and external shocks—a reminder that even in a prolonged pause, vigilance remains the ultimate yield enhancer.

Stay cautious, stay tactical.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet