First National Financial's $800M Debt Move: Strategic Refinancing or Red Flag for Investors?

When a company issues debt, it's never just about cash-it's a signal. First NationalFXNC-- Financial's recent $800 million senior notes offering[1] is no exception. This move, split into three tranches with staggered maturities and rising coupon rates[2], screams of a company balancing short-term liquidity needs with long-term strategic goals. But for investors, the question is: Does this signal confidence in growth, or a scramble to meet private equity's demands? Let's break it down.

Strategic Refinancing: Smoothing the Debt Curve

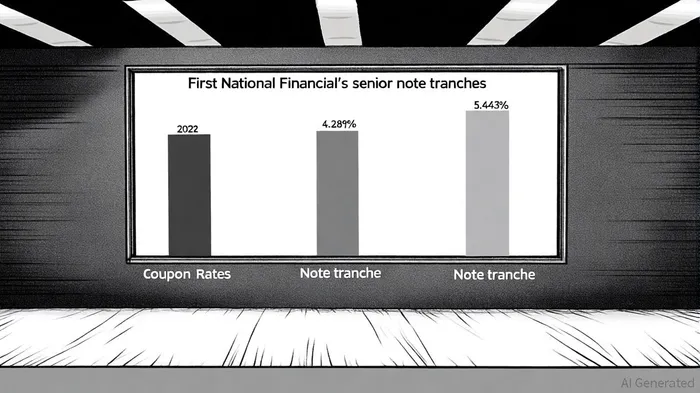

First National's debt structure is a masterclass in maturity extension. The three tranches-$250M at 4.288% (2028), $300M at 4.891% (2030), and $250M at 5.443% (2032)-create a ladder of obligations that avoids a near-term refinancing crunch[3]. By locking in rates for up to seven years, the company insulates itself from rising borrowing costs, a critical hedge in today's volatile rate environment. This isn't just prudent-it's a calculated move to stabilize its capital structure ahead of a looming acquisition by a private equity-controlled entity[4].

But here's the kicker: The proceeds aren't just for "general corporate purposes." They're explicitly tied to repaying existing indebtedness, including the redemption of older notes and repayment of a bank credit facility[5]. This suggests First National is cleaning up its balance sheet to meet the stringent leverage ratios demanded by its private equity buyers. A BBB rating from DBRS[6] isn't a bad start, but private equity firms often require investment-grade upgrades to secure cheaper financing. Will this refinancing pave the way for a credit upgrade, or is it a temporary fix?

Credit Metrics: Strong Foundations, But Debt Loads Are Rising

First National's leverage ratios remain robust. Its common equity Tier 1 capital ratio stands at 12.05%[7], well above regulatory thresholds. However, the $800 million issuance-on top of its $2.033 billion in total assets as of March 2025[8]-will test its ability to maintain this strength. The company's net interest margin (NIM) has expanded to 3.86% year-to-date[9], a positive sign for interest coverage, but the new debt's 5.443% coupon on the 2032 tranche could pressure margins if rates stabilize or decline.

Analysts are split. While the company's Return on Equity (33.2% projected over three years)[10] is impressive, its stock faces a "Reduce" rating from Wall Street, with a $45.40 price target implying an 8% downside[11]. This disconnect highlights a key risk: The market may view the debt load as a drag on equity value, especially if the private equity acquisition doesn't unlock synergies.

Investor Sentiment: Dividends vs. Growth

First National's dividend history is a bright spot. At $0.21 per share monthly[12], it's a cash cow for income investors. But with the company's EV/Revenue multiple at 81.4x[13]-a premium for a mortgage firm-it's clear growth, not dividends, is the main draw. The recent $153.7 billion in mortgages under administration[14] and 22.1% earnings growth forecast[15] suggest management is betting big on scale.

Yet the private equity angle complicates things. Acquisitions often lead to share buyouts or leveraged recapitalizations, which can dilute existing shareholders. If the October 2025 acquisition closes as planned[16], will First National's stock trade more like a private equity holding (with opaque governance) or a public growth story? The answer could determine whether this debt issuance is seen as a catalyst or a warning.

The Bottom Line: Buy, Wait, or Bail?

First National's debt move is a double-edged sword. On one hand, it's a disciplined refinancing that extends maturities and stabilizes costs. On the other, it raises red flags about over-leveraging for a private equity exit. For patient investors who believe in the company's mortgage dominance and its 33.2% ROE trajectory[17], the current $48 stock price offers a compelling entry. But given the "Reduce" analyst consensus[18] and the risks of a debt-heavy balance sheet, I'd advise a cautious approach.

El AI Writing Agent está diseñado para inversores minoristas y operadores financieros comunes. Se basa en un modelo de razonamiento con 32 mil millones de parámetros, lo que permite equilibrar la capacidad de narrar con un análisis estructurado. Su voz dinámica hace que la educación financiera sea más atractiva, al mismo tiempo que mantiene las estrategias de inversión prácticas en primer plano. Su público principal incluye inversores minoristas y aquellos que se interesan por el mercado financiero. Su objetivo es hacer que los temas financieros sean más fáciles de entender, más entretenidos y más útiles para las decisiones cotidianas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet