Muted Wholesale Inflation and Its Implications for Monetary Policy and Equity Markets

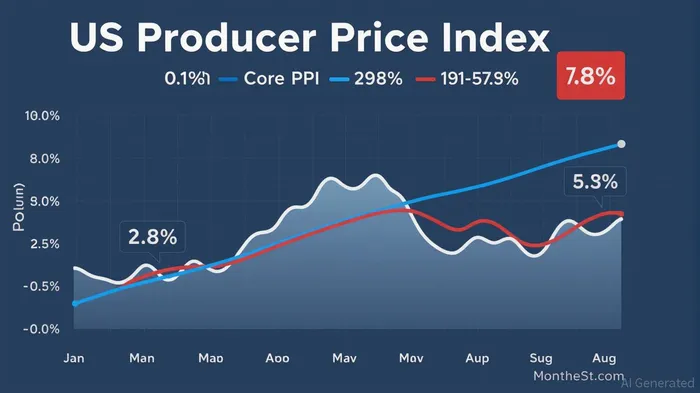

The latest Producer Price Index (PPI) data for August 2025 has sent ripples through financial markets, signaling a modest but meaningful easing in wholesale inflation. With the headline PPI falling 0.1% month-over-month to 149.16 and core PPI declining to 2.8% year-over-year, the data suggests that inflationary pressures are softening at the producer level. This development, while not a seismic shift, has reignited debates about the Federal Reserve's next move and its implications for bond yields and equity sectors.

The PPI Signal: A Pause in Inflationary Momentum

The PPI data reflects a nuanced picture. While headline inflation has moderated from its peak, core PPI—excluding food, energy, and trade services—remains above the Fed's 2% target. The decline in services prices, particularly in trade services (-1.7%) and machinery wholesaling (-3.9%), has been a key driver of the softening. However, goods prices, including a 2.3% surge in tobacco products (linked to Trump-era tariffs), remain stubbornly elevated.

This duality underscores the Fed's dilemma: while headline inflation is easing, structural bottlenecks—such as supply chain disruptions and tariff-driven costs—persist. The PPI's 2.6% annualized rate for headline inflation, though lower than March's 9.7% peak, still exceeds the central bank's comfort zone. Yet, the data has provided a glimmer of hope that the worst of the inflationary surge may be behind us.

Federal Reserve Strategy: A Delicate Balancing Act

The Fed's response to this data has been cautious. At its July meeting, the Federal Open Market Committee (FOMC) held rates steady at 4.25–4.50%, with two dissenting votes favoring a 25-basis-point cut. The central bank's wait-and-see approach reflects its dual mandate: controlling inflation while avoiding a recessionary tightening.

The August PPI data, coupled with weaker-than-expected labor market reports (e.g., a 22,000 job gain in July and a 911,000 downward revision in March's payrolls), has tilted the Fed toward a dovish pivot. Futures markets now price in a 100% probability of a 25-basis-point rate cut at the September meeting, with a 50-basis-point cut gaining traction. However, the Fed's balance sheet remains a wildcard. While its holdings have shrunk from $9 trillion in 2022 to $6.6 trillion, the pace of quantitative tightening is slowing, suggesting the central bank is preparing for a potential shift in policy.

Bond Yields: A Tug-of-War Between Inflation and Policy

The PPI data has created a tug-of-war in bond markets. On one hand, softer inflation expectations have pushed Treasury yields lower, with the 10-year yield dipping to 3.8% in early September. On the other, the Fed's reluctance to commit to aggressive rate cuts has limited the magnitude of the decline. This tension is likely to persist until the Fed's September meeting provides clarity.

Investors should also monitor the interplay between inflation and real yields. A sustained drop in PPI could pressure the Fed to cut rates more aggressively, potentially pushing real yields (nominal yields minus inflation) into negative territory. This would favor long-duration assets like Treasuries and mortgage-backed securities but could weigh on cash-heavy portfolios.

Sector-Specific Stock Opportunities: Winners and Losers in a Dovish Environment

The PPI-driven shift in monetary policy creates asymmetric opportunities for equities. Sectors sensitive to lower interest rates—such as consumer discretionary, technology, and utilities—are likely to outperform.

- Consumer Discretionary: A rate-cut cycle typically boosts spending on big-ticket items. Companies like TeslaTSLA-- (TSLA) and AmazonAMZN-- (AMZN) could benefit from improved consumer confidence and lower borrowing costs.

- Technology: Lower rates reduce the discount rate for future earnings, making high-growth tech stocks more attractive. MicrosoftMSFT-- (MSFT) and NVIDIANVDA-- (NVDA) are prime candidates.

- Utilities: With bond yields declining, utilities like NextEra EnergyNEE-- (NEE) and Dominion EnergyD-- (D) could see their dividend yields become more competitive.

Conversely, sectors tied to inflation—such as energy and materials—may underperform. While energy prices dipped in August, a rebound in inflation could reignite demand for oil and gas. However, the long-term outlook for these sectors remains clouded by the Fed's inflation-fighting resolve.

Investment Implications: Positioning for a Dovish Pivot

For investors, the key takeaway is to balance exposure to rate-sensitive sectors with defensive positions in case inflation surprises to the upside. A tactical shift toward equities with strong cash flows and low debt burdens—such as consumer staples and healthcare—could provide downside protection.

In fixed income, a barbell strategy of short-duration bonds and inflation-linked Treasuries may offer the best risk-adjusted returns. Meanwhile, those with a higher risk tolerance could explore leveraged loans or high-yield corporate bonds, which tend to perform well in a rate-cutting environment.

The Fed's September meeting will be a pivotal moment. If the central bank delivers a 50-basis-point cut, markets could rally on the back of improved liquidity. However, a 25-basis-point cut may not be enough to offset lingering inflation risks, particularly from tariffs and global supply chain bottlenecks.

In the end, the muted PPI data is a signal, not a solution. Investors must remain agile, ready to adjust their portfolios as the Fed navigates the delicate balance between inflation control and economic growth.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet