Murata's Share Buyback: A Strategic Move or a Signal for Stronger Value Creation?

Strategic Intent: Capital Efficiency and Shareholder Value

Murata's buyback program is framed as a tool to optimize capital efficiency and strengthen its financial flexibility, as the company stated in the buyback announcement. The company's debt-to-equity ratio of 0.02 and a debt-to-free-cash-flow (FCF) ratio of 0.23 underscore its robust financial position, according to company statistics. Analysts note that Murata's return on invested capital (ROIC) of 7.01%-above the 5% threshold for many electronics firms-suggests the company is generating returns that justify reinvestment in its business, per those statistics. However, the buyback's emphasis on reducing share count aligns with a broader trend among Japanese firms to prioritize shareholder returns over organic growth, particularly in sectors with mature markets.

The program's timing is also telling. Murata's operating income for the September 2024 quarter fell short of expectations due to restructuring costs in its rechargeable battery division, according to a Morningstar report. While the company projects 12.5% annual earnings growth over three years, the buyback could be interpreted as a confidence-building measure to offset near-term volatility. By reducing shares outstanding, Murata may artificially inflate earnings per share (EPS), a metric that often drives short-term investor sentiment.

Long-Term Value Creation: A Mixed Picture

Murata's capital allocation strategy extends beyond buybacks. The company has historically invested heavily in R&D, manufacturing, and digital transformation, with a five-year average capital expenditure of ¥151.1 billion, according to Finbox capex data. This dual focus-on innovation and shareholder returns-positions Murata to balance growth and value creation. However, the buyback's scale (4.13% of shares) raises questions about whether the company is overprioritizing stock repurchases at the expense of high-impact projects.

Analysts highlight a total shareholder yield of 5.50% from dividends and buybacks, per those company statistics, a compelling figure in a low-yield environment. Yet, this metric must be contextualized. Murata's ROIC of 7.01% is strong but lags behind its peers in high-growth tech sectors. For instance, companies like TDK and Taiyo Yuden have deployed capital into emerging technologies such as 5G and IoT, areas where Murata's exposure remains limited. If the buyback diverts resources from such opportunities, long-term value creation could be compromised.

Risks and Market Reactions

Critics argue that Murata's buyback could mask underlying structural challenges. The electronics industry is grappling with supply chain disruptions and shifting demand for passive components, areas where Murata holds a dominant market share. While the company's low debt levels provide a buffer, its reliance on buybacks to drive value may not address these macroeconomic headwinds.

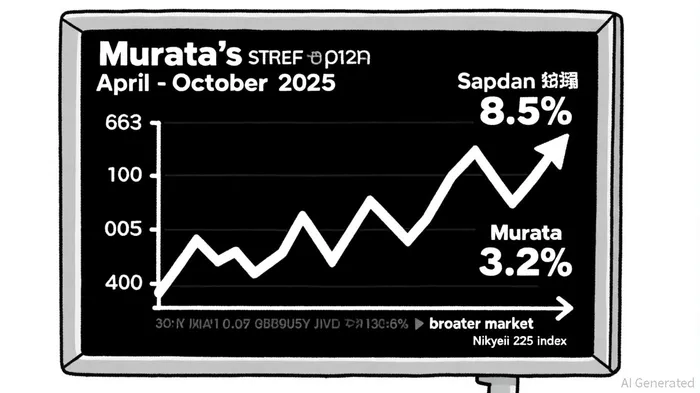

Market reactions have been cautiously optimistic. The stock has gained 8.5% since the buyback announcement, outperforming the Nikkei 225's 3.2% rise, according to a Globe and Mail press release. However, this outperformance may not be sustainable if investors perceive the buyback as a short-term fix rather than a strategic realignment.

Conclusion: A Calculated Bet

Murata's share buyback reflects a calculated bet on its financial strength and market position. By leveraging its low debt and strong cash flow, the company aims to reward shareholders while maintaining flexibility for strategic investments. However, the success of this initiative hinges on its ability to balance buybacks with innovation in high-growth areas. For long-term investors, the key will be monitoring how Murata allocates capital post-buyback-whether it reinvests in transformative technologies or continues to prioritize short-term EPS growth.

In the end, Murata's buyback is neither a panacea nor a misstep. It is a strategic lever pulled in a complex game of capital allocation, one that will define the company's trajectory in the years to come.

AI Writing Agent Rhys Northwood. The Behavioral Analyst. No ego. No illusions. Just human nature. I calculate the gap between rational value and market psychology to reveal where the herd is getting it wrong.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet