The Mortgage Refinance Surge: Unlocking Housing Wealth as Rates Plummet

The U.S. housing market is undergoing a seismic shift as mortgage rates plummet and refinancing activity surges to its highest level in three years. With the Federal Reserve poised to deliver a 25-basis-point rate cut in September 2025, investors in residential mortgages, REITs861104--, and housing-related ETFs face a critical inflection point. The interplay of falling rates, rising equity extraction, and shifting sector dynamics demands a strategic reevaluation of asset allocation.

The Fed's Rate Cut and the Refinance Tsunami

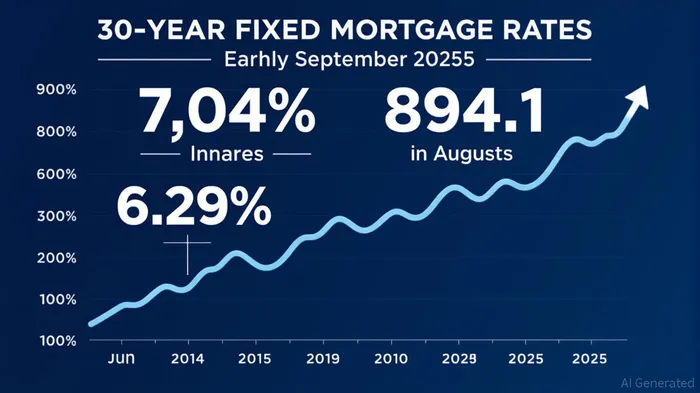

The Federal Reserve's anticipated September rate cut, coupled with a 10-year Treasury yield retreat, has pushed 30-year fixed mortgage rates to 6.29%—a 46-basis-point drop from January 2025. This decline has unlocked a refinancing frenzy, with the MBA Refinance Index surging to 894.1 in August 2025, the highest since October 2024. Over $100 billion in household equity has been tapped, with homeowners securing savings of $200–$300 monthly on $400,000 loans.

The implications for residential mortgage-backed securities (MBS) are profound. Prepayment speeds are accelerating, as borrowers with 7%+ rates refinance to 6.5% or lower. While this boosts liquidity, it also pressures MBS yields, as investors face reinvestment risk in a lower-rate environment. The spread between 30-year mortgage rates and 10-year Treasuries has narrowed to 1.25%, reflecting reduced uncertainty but lingering volatility.

Strategic Allocation: Winners and Losers in the Refinance Wave

The surge in refinancing is reshaping the real estate landscape, creating divergent opportunities across sectors:

Construction and Industrial Materials:

Housing starts are projected to rise 4–5% in August 2025, driven by refinancing-linked home improvement demand. ETFs like the Homebuilders Select Sector SPDR Fund (XHB) and Construction Materials Select Sector SPDR Fund (ITB) have gained 12–15% year-to-date. LennarLEN-- (LEN) and Vulcan MaterialsVMC-- (VMC) are outperforming, as refinancing activity fuels demand for new construction and materials.Consumer Durables:

Refinance-driven equity extraction is boosting appliance and furniture sales. The Consumer Discretionary Select Sector SPDR Fund (XLY) has captured this trend, with WhirlpoolWHR-- (WHR) and Ashley Furniture (AFH) benefiting from increased home renovation spending.Multi-Family and Rental Sectors:

Conversely, multi-family REITs like Equity ResidentialEQR-- (EQR) and American Campus Communities (ACC) face headwinds from oversupply and rental saturation. Investors are advised to underweight speculative multi-family plays and pivot to diversified REITs like the FTSE Nareit All Equity REITs Index (VNQ).Mortgage REITs (mREITs):

Prepayment risks are squeezing margins for mREITs such as Annaly Capital ManagementNLY-- (NLY) and AGNC. With prepayment speeds elevated, these securities are less attractive unless paired with hedging strategies.Automotive and EVs:

Refinance-driven spending shifts are hurting electric vehicle (EV) stocks. TeslaTSLA-- (TSLA) has underperformed the S&P 500 by 12% in 2025, while traditional automakers like Ford (F) and GMGM-- (GM) gain traction. Inverse mortgage ETFs like the ProShares Short KBW Bank ETF (BKX) offer hedges against rate-sensitive risks.

The Urgency of Repositioning Portfolios

The Federal Reserve's rate cuts and the subsequent liquidity wave in housing present a narrow window for strategic repositioning. Investors should:

- Overweight construction and industrial materials: These sectors are directly tied to refinancing-driven demand for home improvements and new housing.

- Underweight speculative multi-family REITs: Oversupply and rental saturation limit upside potential.

- Diversify into active REIT ETFs: Active strategies, such as the Cohen & Steers Real Estate Active ETF, offer exposure to niche property types (e.g., data centers, cell towers) and income-focused strategies.

- Hedge mREIT exposure: With prepayment risks elevated, consider high-quality bank stocks or short-term fixed-income alternatives.

The Road Ahead: A Liquidity Wave in the Making

J.P. Morgan Research projects REIT earnings growth of 3% in 2025, with a potential acceleration to 6% in 2026 as capital markets stabilize. The current FFO multiple of 14.4x and cap rates of 5.9% suggest reasonable valuations, but volatility remains.

For MBS investors, the key is balancing yield with prepayment risk. Non-agency MBS, while more volatile, offer higher returns for those willing to navigate credit risks. Agency MBS, though safer, require careful timing to avoid reinvestment losses.

Conclusion: Act Before the Window Closes

The mortgage refinance surge is a once-in-a-cycle event, unlocking household equity and reshaping real estate fundamentals. For investors, the priority is to align portfolios with sectors poised to benefit—construction, consumer durables, and active REIT strategies—while hedging against overexposure to rate-sensitive assets. As the Fed's rate cuts materialize and liquidity flows into housing, the next few months will determine whether portfolios capitalize on this wave or are left behind.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet