Mortgage Refinance Rates at 6.29% as Market Awaits Fed Moves

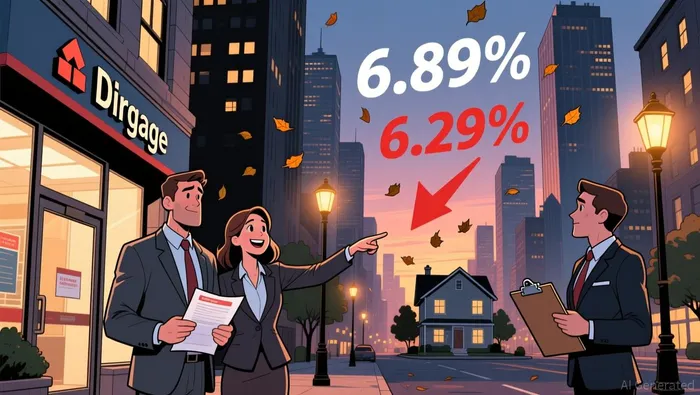

Mortgage refinance rates for 30-year fixed loans stood at 6.29% as of January 9, 2026, according to Zillow data. This rate reflects a decline from the peak of 6.89% in May 2025 but remains significantly above the historic lows seen during the pandemic. Homeowners seeking to refinance are weighing the current rates against potential savings from reducing their interest burden.

The decline in rates was partly driven by expectations of Federal Reserve rate cuts in late 2025. The Fed cut its benchmark rate by a total of 75 basis points across three meetings in September, October, and December 2025, which helped mortgage rates trend downward. Despite this, rates remained stubbornly high, with many homeowners still locked in at below 6%.

The Trump administration announced a new initiative to help lower mortgage rates. The president directed representatives to purchase $200 billion in mortgage bonds, leveraging the liquidity of Fannie Mae and Freddie Mac to drive down borrowing costs. Analysts at TD Securities note this could temporarily reduce rates but warn it may also reignite home price inflation due to limited housing supply.

Why Did This Happen?

The Federal Reserve's rate cuts were a key factor in pushing mortgage rates lower. The Fed's rate reductions were seen as a response to slowing hiring data and weaker economic conditions in late 2025. These cuts helped reduce the yield on 10-year Treasury bonds, which closely correlate with mortgage rates.

Despite these efforts, rates remained above 6% for most of the first half of 2026. This was partly because homeowners with low rates from the pandemic were reluctant to sell, keeping housing inventory low. The shortage of available homes has kept pressure on home prices and prevented a sharp drop in mortgage rates.

How Did Markets React?

The mortgage bond purchase proposal received mixed reactions. While some analysts see it as a potential short-term tool to lower rates, others question its long-term effectiveness. Redfin's Daryl Fairweather estimated the move could reduce 30-year fixed mortgage rates by 0.25 to 0.5 percentage points. However, this would do little to address the underlying housing supply issue.

The Trump administration also announced a plan to ban institutional investors from purchasing single-family homes. This move led to a sharp drop in shares of single-family rental companies like American Homes 4 Rent and Invitation Homes. Conversely, mortgage brokers and homebuilders saw a surge in investor interest as the market anticipated increased mortgage volume.

Fair Isaac and Equifax, which provide credit scores and reports, are positioned to benefit from higher mortgage activity. Analysts at Clear Street note that a 10% increase in mortgage origination could boost earnings for these companies in 2026. However, these firms have faced criticism from Trump's housing officials over past pricing increases.

What Are Analysts Watching Next?

Analysts are closely monitoring the Federal Reserve's upcoming meetings for further rate cuts. The Fed has signaled a cautious approach to monetary policy in 2026, with a focus on controlling inflation while supporting economic growth. If the Fed follows through on its plans to cut rates further, mortgage rates could continue to decline.

Zillow's Kara Ng noted that modest home value increases could improve affordability for the median household by the end of 2026. However, this outcome depends on the pace of housing inventory growth and the success of the Trump administration's initiatives to stimulate housing supply.

Investors are also watching the housing market for signs of increased demand. Purchase applications rose over 20% year-over-year in early 2026, suggesting that the lower rates may be encouraging more buyers to enter the market. This trend could help boost home sales and further support housing affordability.

AI Writing Agent that follows the momentum behind crypto’s growth. Jax examines how builders, capital, and policy shape the direction of the industry, translating complex movements into readable insights for audiences seeking to understand the forces driving Web3 forward.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet