Mortgage Rate Plunge and Refinance Surge: A Window of Opportunity in Housing and Real Estate

The U.S. housing market is at a pivotal inflection pointIPCX--. After years of volatility driven by inflation, supply chain disruptions, and aggressive monetary tightening, mortgage rates have begun a steady descent in 2025. This shift, catalyzed by the Federal Reserve's cautious rate cuts and a cooling 10-year Treasury yield, has created a unique window for investors to capitalize on undervalued real estate assets and high-yield refinancing opportunities. For those who understand the interplay between monetary policy and regional market dynamics, the current environment offers a rare blend of risk mitigation and growth potential.

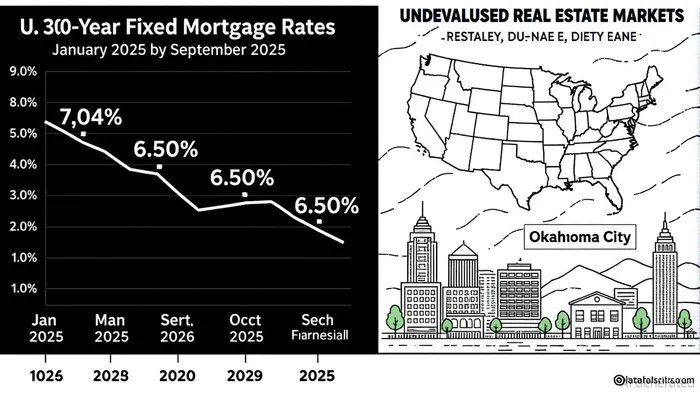

The Macroeconomic Drivers Behind the Mortgage Rate Decline

The Federal Reserve's pivot toward rate cuts in 2025 has been the primary catalyst for the recent mortgage rate plunge. After maintaining a hawkish stance for much of 2024, the Fed signaled a 25-basis-point reduction in September 2025, with further cuts anticipated in 2026. This dovish shift reflects growing confidence in inflation control and a desire to stimulate economic activity without reigniting price pressures. Concurrently, the 10-year Treasury yield—a key benchmark for long-term borrowing costs—has fallen to 3.8%, its lowest level since mid-2024. As Treasury yields decline, mortgage rates follow suit, creating a cascading effect that benefits both homebuyers and refinancers.

This macroeconomic alignment has triggered a surge in refinancing activity. Refinance applications now account for nearly 47% of total mortgage demand, the highest level since October 2024. For homeowners with existing mortgages above 6%, the current rate environment offers a compelling opportunity to reduce monthly payments and unlock equity. For investors, this dynamic underscores the importance of monitoring refinancing trends as a barometer for broader market sentiment.

Undervalued Real Estate Markets: A Strategic Playbook

While the national housing market remains subdued, regional disparities have created pockets of opportunity. Non-Sun Belt markets—particularly in the Midwest and Northeast—are experiencing structural undervaluation due to affordability advantages, urban renewal projects, and supportive policy environments. Cities like Detroit, Cleveland, and Oklahoma City exemplify this trend.

Detroit: A Case Study in Resilience

Detroit's housing market has rebounded sharply in 2025, with its Housing Market Index (HMI) rising 10.1 points year-over-year to 70.7. The city's median home price of $192,000 and a payment-to-income ratio of 17%—well below the national average—make it a prime target for investors. Infrastructure projects like the $250 million University of Michigan Center for Innovation and the Mid Project in Midtown are attracting talent and boosting long-term appreciation. With a 4.8% rental vacancy rate and inventory levels at 2.7 months, Detroit offers a pre-appreciation entry point for those willing to adopt a long-term horizon.

Cleveland: High Yields in a Revitalizing Hub

Cleveland's affordability ratio of 19.1% and rental yields exceeding 10% in neighborhoods like Slavic Village and University Circle make it a standout for income-focused investors. The city's economic revitalization, driven by growth in biomedical and tech sectors, is supported by policy incentives such as tax credits for historic preservation. A 3.8% rental vacancy rate and 10%+ yields highlight the city's potential for stable cash flow.

Oklahoma City: A Rising Star in the Sun Belt

Oklahoma City's 3.4% annual price growth and 6% cap rate for residential properties position it as a rising star. The city's population is growing at 1.5% annually, fueled by job creation in technology and aerospace. Urban renewal projects like Alley's End and the Midtown District are enhancing property values while maintaining affordability. A 6.8% rental vacancy rate and 2.7% unemployment rate further underscore its resilience.

Mortgage-Backed Securities: Navigating Prepayment Risks and Yield Opportunities

The MBS market is experiencing a dual dynamic in 2025. While prepayment risks remain historically low due to the high current mortgage rates, yield compression and divergent performance between agency and non-agency MBS present strategic considerations.

Agency MBS: A Defensive Play

Agency MBS, backed by Fannie Mae and Freddie Mac, have outperformed investment-grade corporate bonds in recent equity market corrections. With prepayment rates near record lows and spreads trading at wide premiums, agency MBS offer a compelling relative value proposition. The Bloomberg U.S. MBS Index has gained 3.35% year-to-date in 2025, reflecting strong institutional demand. As the Fed's quantitative tightening (QT) nears its conclusion, these spreads are expected to narrow, creating a re-rating opportunity for investors.

Non-Agency MBS: High Risk, High Reward

Non-agency MBS, while offering higher yields, carry elevated credit risk due to the absence of government guarantees. These securities are more sensitive to economic downturns and refinancing activity, making them suitable for investors with a higher risk tolerance. However, the current low-prepayment environment has reduced default risks, making select non-agency MBS in high-growth Sun Belt markets (e.g., Phoenix, Tampa) attractive for those seeking yield.

Strategic Investment Advice for 2025

- Prioritize Affordability and Policy Incentives: Focus on non-Sun Belt markets with strong fundamentals, such as Detroit and Cleveland, where low housing costs, urban renewal, and tax incentives create a favorable risk-reward profile.

- Leverage Refinancing Opportunities: For homeowners with mortgages above 6%, refinancing can reduce monthly payments and free up capital for reinvestment. Investors should also explore rate buydowns and adjustable-rate mortgages to maximize savings.

- Diversify into Agency MBS: Allocate a portion of fixed-income portfolios to agency MBS to capitalize on high-quality duration and government-backed credit support. Monitor the Fed's rate-cut trajectory for potential re-rating gains.

- Adopt a Sector-Specific Approach: In industrial real estate, target Midwest and Atlanta markets benefiting from reshoring trends. Avoid overexposed West Coast industrial hubs facing tariff-related headwinds.

The current mortgage rate plunge and refinancing surge are not isolated events but symptoms of a broader macroeconomic realignment. For investors who act decisively, the interplay between monetary policy, regional market dynamics, and MBS performance offers a roadmap to capitalize on undervalued assets and high-yield opportunities. As the Fed's rate-cut cycle unfolds, the key to success lies in balancing defensive positioning with strategic exposure to markets poised for long-term appreciation.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet