The Mortgage Rate Plunge Amid Economic Weakness: A Strategic Shift in Housing Market Dynamics

The U.S. economy in 2025 is caught in a paradox: a labor market that, while stable, shows signs of fatigue, and a housing sector where refinancing activity is surging despite lingering affordability challenges. This divergence—between a slowing labor force and a mortgage market poised for a modest rebound—has created asymmetric opportunities and risks for investors. For those attuned to the interplay between macroeconomic trends and asset-specific dynamics, residential real estate and (MBS) are emerging as strategic plays in a redefining economic landscape.

Labor Market: A Tale of Stagnation and Structural Shifts

The second quarter of 2025 revealed a labor market that, while not in crisis, is no longer expanding at pre-pandemic rates. , , . Wage growth, though nominal, has flattened, . Meanwhile, , a trend exacerbated by aging demographics and shifting immigration policies.

These metrics signal a maturing labor market, where employers face a tighter talent pool in sectors like healthcare and education, yet broader industries grapple with wage stagnation. The Department of Government Efficiency (DOGE) layoffs further complicated the picture, . For investors, this environment suggests a labor market that is neither collapsing nor accelerating—a critical backdrop for understanding capital flows into real estate.

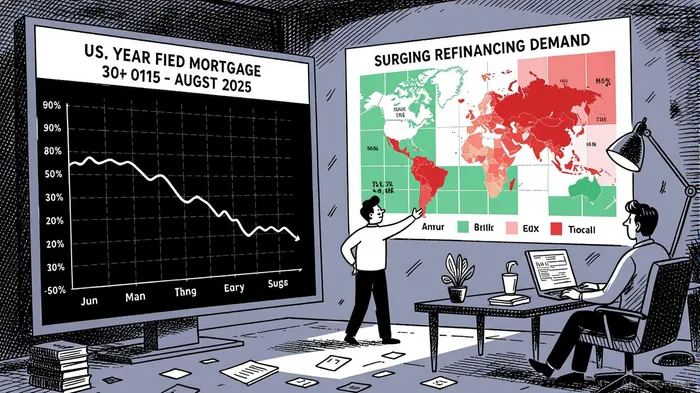

: A Silver Lining in a High-Rate Environment

Contrast this with the housing market, where refinancing demand has defied expectations. , , . , yet the annual trend remains upward.

This surge is not merely a function of lower rates but a strategic response to accumulated home equity. Homeowners are leveraging cash-out refinances to access liquidity, even as monthly savings from rate reductions remain modest. For example, .

: A Rebalancing of Risk and Reward

The interplay between labor market weakness and refinancing momentum has reshaped capital flows into residential real estate. While high mortgage rates have historically suppressed demand, the recent decline in rates has reignited investor interest in markets with strong equity fundamentals. , .

However, structural challenges persist. Construction labor shortages, exacerbated by reduced immigration and an aging workforce, have constrained new housing supply. J.P. Morgan notes that 30% of U.S. construction workers are immigrants, . , .

and Risks for Investors

The divergence between labor market underperformance and housing market resilience presents a unique investment landscape. For residential real estate, the key lies in asset selection. Markets with strong household formation trends—such as urban centers with growing populations—remain attractive, as do properties in areas with high equity-to-income ratios. Conversely, regions reliant on construction-driven growth face headwinds from labor shortages and cost inflation.

Mortgage-backed securities (MBS) also warrant a strategic reevaluation. While high rates have historically depressed prepayment speeds, the recent refinancing surge suggests a potential uptick in turnover. , which are less sensitive to rate volatility. Additionally, , though this remains contingent on inflation and labor market data.

Strategic Recommendations for a Shifting Landscape

- Rebalance Real Estate Portfolios: Prioritize markets with strong equity fundamentals and low inventory. Avoid overexposure to construction-dependent regions.

- Leverage MBS Opportunities: Target securities with shorter durations or those tied to cash-out refinances to capitalize on refinancing momentum.

- Monitor Labor Market Shifts: Track participation rates and wage growth in key sectors like healthcare and education, which drive long-term housing demand.

- Hedge Against Affordability Risks: Use derivatives or alternative real estate sectors (e.g., logistics, data centers) to offset potential downturns in residential demand.

Conclusion

The 2025 housing market is a study in contrasts: a labor force that is neither collapsing nor accelerating, and a refinancing boom that hints at a nascent recovery. For investors, the path forward lies in navigating these asymmetries with precision. Residential real estate and MBS are no longer passive plays—they are strategic instruments in a market defined by divergent forces. As the Federal Reserve weighs rate cuts and labor market dynamics evolve, those who adapt their strategies to this new paradigm will find themselves well-positioned for the opportunities ahead.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet