The Mortgage Rate Drop: A Catalyst for Housing Market Rebound and Real Estate Investment Opportunities

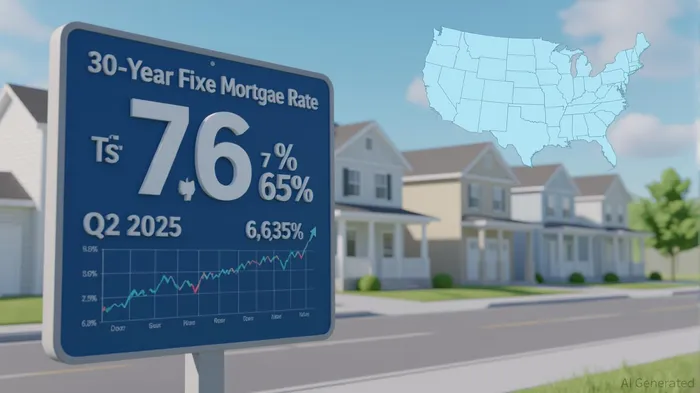

The U.S. housing market is at a pivotal inflection pointIPCX--. After years of volatility driven by inflation, Federal Reserve tightening, and geopolitical uncertainty, mortgage rates have begun a modest but meaningful decline in 2025. The 30-year fixed-rate mortgage averaged 6.63% in Q2 2025, down from a peak of 7.08% in 2022, signaling a shift in buyer behavior and unlocking new opportunities for investors. While these rates remain above the post-pandemic lows of 2.65%, they represent a critical threshold: a low-rate environment that could catalyze a housing market rebound and reshape regional investment dynamics.

The Mechanics of a Mortgage Rate Drop

Mortgage rates are not just numbers—they are levers that amplify or dampen market activity. A 1% drop in rates can increase purchasing power by 10%, as lower borrowing costs reduce monthly payments and expand affordability. In Q2 2025, the Federal Reserve's cautious approach to inflation—projecting only three rate cuts for the year—has kept the 30-year rate in a narrow range of 6.5–6.9%. However, analysts at the Mortgage Bankers Association and Wells FargoWFC-- anticipate further declines by 2026, with rates potentially dipping into the 5.5–6.0% range. This trajectory creates a window for investors to act before the market fully adjusts.

Undervalued Markets: The Midwest and South Lead the Way

The most compelling opportunities lie in regions where fundamentals align with the low-rate environment. Detroit, Cleveland, and Dayton, Ohio, exemplify this trend. These cities have historically low price-to-rent ratios—Detroit at 8, Cleveland at 11.0—indicating that buying is significantly more favorable than renting. For instance, Detroit's median home price of $97,200 compared to a median annual rent of $12,600 creates a cash flow-positive scenario for investors. Similarly, Cleveland's 11.0 ratio suggests strong rental demand and potential for appreciation, even as national home price growth slows to 3–5% annually.

Demographic shifts further bolster these markets. The Midwest and South have seen a net inflow of residents from high-cost coastal cities, driven by remote work and affordability. Detroit's revitalization efforts, Cleveland's growing healthcare sector, and Dayton's proximity to Cincinnati have attracted young professionals and families. Meanwhile, inventory levels in these regions remain below pre-pandemic norms, limiting supply and supporting price stability.

Strategic Investment Playbook

- Refinance Opportunities: Investors with existing properties in these markets should monitor rate trends. A drop to 6.0% by 2026 could unlock refinancing gains, reducing monthly payments and freeing capital for renovations. For example, a $200,000 loan at 6.0% would save $150/month compared to 6.8%.

- Cash Flow Analysis: Focus on single-family rentals (SFRs) in Detroit and Cleveland, where rental income often exceeds mortgage costs. A $150,000 SFR in Detroit with a 6.63% mortgage would generate a 12% cash-on-cash return, assuming $1,000/month in rent.

- Timing the Market: Enter undervalued markets before inventory increases. The “lock-in effect” (82% of homeowners still have rates below 6% in 2025) will gradually ease, increasing supply by 2026. Early entry allows investors to secure properties at current price levels.

- Value-Add Strategies: Target properties in need of minor upgrades (e.g., kitchens, HVAC systems) to boost rental income. In Dayton, a $5,000 renovation could increase rent by $200/month, improving ROI.

Risks and Mitigations

While the outlook is optimistic, risks persist. Sticky inflation and geopolitical tensions could delay rate cuts, prolonging high borrowing costs. Additionally, overleveraging in a low-rate environment may expose investors to future rate hikes. To mitigate these, prioritize properties with strong cash flow and maintain conservative leverage ratios (loan-to-value below 80%).

Conclusion

The mortgage rate drop of 2025 is not just a market correction—it is a catalyst for rebalancing. For investors, the key lies in identifying undervalued regions where fundamentals align with the low-rate environment. Detroit, Cleveland, and Dayton offer a blueprint: affordable prices, strong rental demand, and demographic tailwinds. By leveraging refinancing opportunities, focusing on cash flow, and timing market entry, investors can position themselves to capitalize on the next phase of the housing cycle.

In a world of uncertainty, the housing market's response to declining rates provides a rare combination of predictability and opportunity. For those who act with discipline and foresight, the rewards could be substantial.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet