Morgan Stanley Flags Over 20% Upside in ASML on AI Capex Boom

Key Takeaways

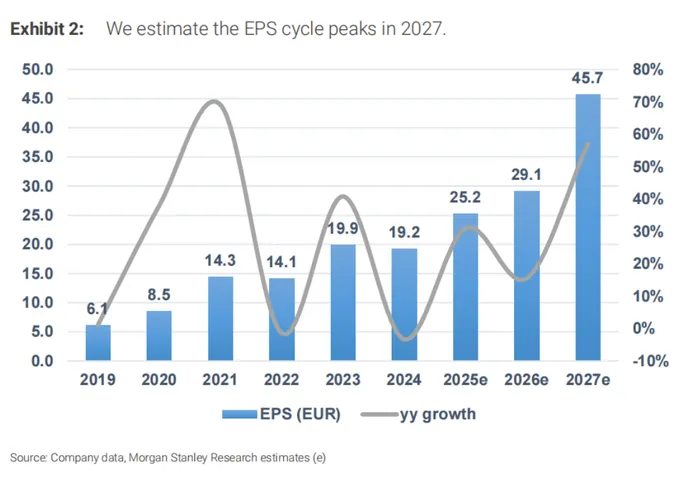

ASML is entering the strongest earnings cycle in its history, with 2027 projected as the peak year.

AI-driven expansion in advanced logic and memory is accelerating EUV and DUV demand.

TSMC’s sharply higher capex is a critical catalyst for ASML’s multi-year upside.

DRAM and HBM shortages are triggering a new wave of memory capacity investment.

Morgan Stanley delivers one of the most bullish outlooks on ASMLASML-- to date, implying substantial upside for the stock.

On January 16, Morgan StanleyMS-- released a major research report with a clear and forceful conclusion: as the AI wave drives capacity expansion in advanced logic and memory semiconductors, ASML is standing at the starting point of the strongest profit cycle in its history, with 2027 expected to mark the peak.

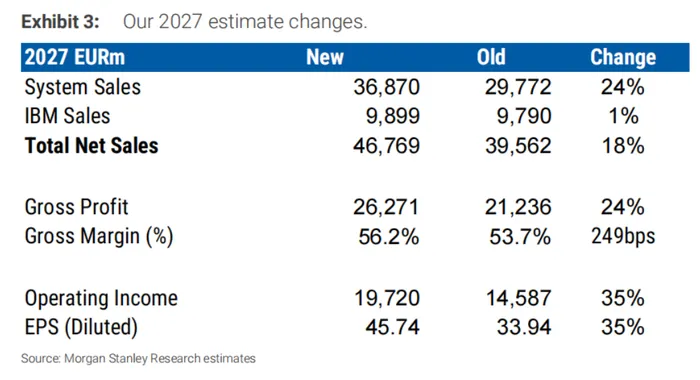

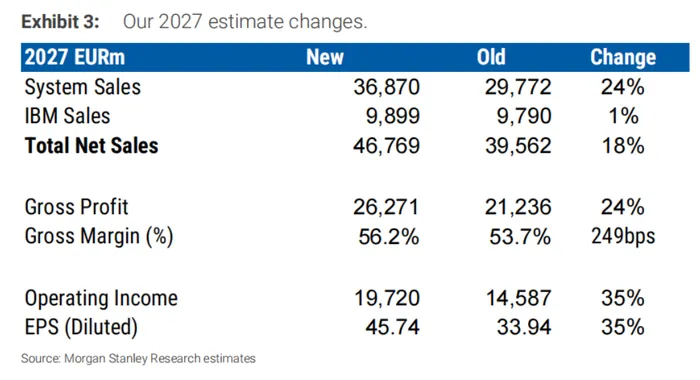

Morgan Stanley forecasts ASML’s fiscal 2027 revenue at approximately $51.5 billion, with EBIT reaching $21.7 billion and gross margin rising to 56.2%.

Earnings per share are projected at $50.31, representing a 35% upward revision from the prior estimate of $37.33 and a 57% year-over-year increase from the 2026 estimate of $32.03. This would mark the fastest annual earnings growth in ASML’s history.

Three Engines Driving the Earnings Explosion

According to the report, this earnings surge is powered by three major engines:

Strong demand from advanced logic foundries

Large-scale capacity expansion in DRAM memory

End-demand resilience that is exceeding prior expectations

Morgan Stanley issued an exceptionally strong bullish signal on ASML, sharply raising its price target from $1,100 to $1,540, while reiterating its Overweight rating and Top Pick status.

TSMC Capex Surge Is the Key Catalyst

TSMC’s sharply higher capital expenditure guidance has emerged as a critical catalyst.

During its fourth-quarter earnings call, TSMCTSM-- guided 2026 capex at $52–56 billion, with the midpoint implying 32% year-over-year growth, well above 2025’s $40.9 billion. Roughly 70–80% of this spending will be allocated to advanced process technologies. TSMC also hinted that capex could rise further in subsequent years.

As a result, Morgan Stanley raised its forecast for TSMC’s EUV tool purchases in 2026 from around 20 units to 29 units, and sharply increased the 2027 estimate from 28 units to 40 units. TSMC is expected to begin early construction of A14 capacity in preparation for 2028 production. In 2025, TSMC is projected to take delivery of approximately 18 low-NA EUV tools.

Beyond TSMC, improving process execution at Intel and Samsung is also expected to translate into tangible demand. Morgan Stanley estimates that each company will purchase 5–6 EUV tools in 2027 for foundry and logic operations.

In total, around 52 EUV tools are projected to be shipped to logic and foundry customers in 2027, far exceeding the previous expectation of 25–30 units.

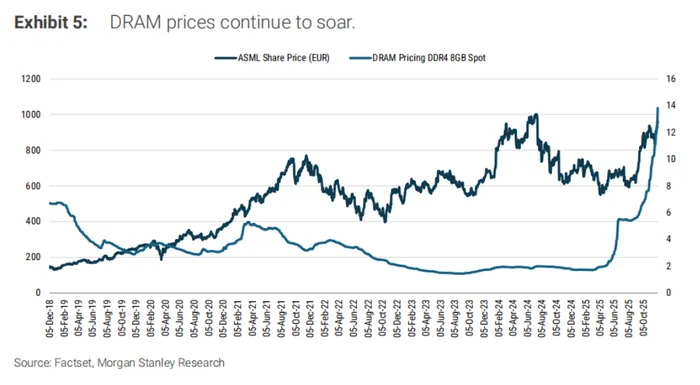

DRAM Enters an Unprecedented Boom

Morgan Stanley notes that DRAM prices have remained exceptionally strong through the fourth and first quarters, driven by conventional server CPU demand and hyperscalers’ aggressive investment in AI workloads for 2026–27, particularly agentic AI.

Capacity shortages have pushed both HBM and standard DRAM prices to near-unprecedented sequential and year-over-year growth rates. The firm expects this trend to persist for at least 1–2 more quarters, ultimately triggering a large-scale buildout in DRAM manufacturing capacity — directly boosting demand for ASML’s EUV and DUV tools.

Most of this capacity investment is expected to materialize in 2026–27, aimed at meeting demand in 2027–28.

Morgan Stanley projects ASML’s DUV revenue to reach approximately $16.5 billion in 2027, with potential upside if NAND investment accelerates beyond expectations.

EUV Shipments to Hit Record Highs

Based on combined logic and memory demand, Morgan Stanley expects ASML to ship approximately 80 EUV tools in 2027, a new all-time high. This includes roughly 52 units for logic and foundry customers, with the remainder going to memory manufacturers.

Demand Stronger Than Feared

Morgan Stanley’s channel checks indicate that demand remains robust across leading memory producers and major customers. Analysts expect ASML to highlight demand strength exceeding prior guidance in its upcoming earnings report.

The firm now expects 2026 revenue to be roughly flat year over year, rather than declining by 15–20% as previously guided by the company. This improved trend is assumed to carry into 2027.

Near-Term Catalyst: Q4 Earnings and Strong Orders

ASML is scheduled to report fourth-quarter results on January 28, 2026. Morgan Stanley expects:

Orders: Q4 bookings of approximately $8.0 billion, up from $5.9 billion in Q3. This includes 19 low-NA EUV tools, primarily from TSMC (9 units), along with memory demand from Samsung and SK Hynix. This will be the final quarter in which ASML discloses order data.

Revenue: Estimated at $10.6 billion, near the top end of guidance ($10.1–10.8 billion), up 4% year over year. Full-year revenue is projected at $35.9 billion, up 15%, in line with prior guidance.

Margins: Q4 gross margin is expected at 51.8%, near the midpoint of guidance (51–53%), up 20 basis points sequentially. Analysts maintain a constructive view on 2026 margin expansion.

2026 Guidance: ASML is expected to guide to double-digit revenue growth (+12%) for 2026, implying revenue of approximately $40.2 billion. While management may continue to reference downside risks, the tone is expected to become less conservative.

Valuation and Bull Case

Morgan Stanley maintains ASML as its top pick, applying a 31x P/E multiple to arrive at a $1,540 price target.

In a bull-case scenario, assuming $55 EPS in 2027 and a 40x multiple, the stock could reach $2,200, implying substantial upside from current levels.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO