Mohawk Industries: It's Premature To Upgrade This Play

The flooring manufacturing sector has long been a barometer of consumer confidence and housing market health. Yet, for Mohawk IndustriesMHK-- (MHK), a leader in hard surface flooring, the current valuation landscape suggests caution. Despite the sector's growth potential, Mohawk's stock appears misaligned with industry benchmarks, particularly when factoring in earnings growth expectations. Investors may find it premature to upgrade their exposure to this name without a clearer correction in its price-to-earnings-to-growth (PEG) dynamics.

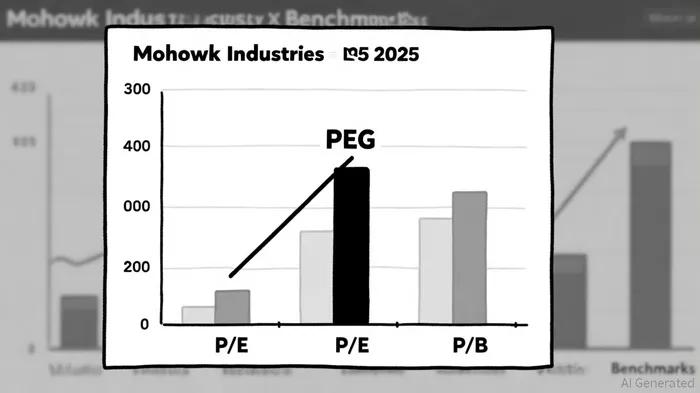

Valuation Metrics: A Tale of Two Stories

Mohawk's 2025 trailing price-to-earnings (P/E) ratio stands at 15.95, while its forward P/E of 12.28 implies a discount to current earnings, according to StockAnalysis statistics. On the surface, these figures suggest affordability. However, the price-to-book (P/B) ratio of 0.92 reveals a deeper issue: the market values MohawkMHK-- at a discount to its net asset value, a rare signal in an industry where intangible assets like brand strength and distribution networks often command premiums, per StockAnalysis.

The critical misalignment, though, lies in the PEG ratio. At 3.41, Mohawk's PEG ratio dwarfs the 1.45 average for the "Home furnishings" sector and the 14.44 PEG of the broader "Building products" industry, according to Eqvista data. A PEG above 1 typically signals overvaluation relative to growth expectations. For Mohawk, this implies that even with its forward P/E of 12.28, the market is pricing in growth that may not materialize-or is being rewarded for risks not fully reflected in traditional metrics. Eqvista's industry breakdown highlights the disparity between Mohawk and sector peers.

Sector Positioning: Growth vs. Valuation

The flooring industry itself is poised for expansion. Global market size is projected to grow at a 6.8% CAGR through 2030, driven by demand for premium products and sustainability-focused innovations, per Awedeco flooring statistics. North America, Mohawk's core market, is seeing strong adoption of luxury vinyl tile (LVT), a segment where the company holds a dominant position, a point Awedeco also emphasizes. Yet, this growth backdrop does not automatically justify its current valuation.

Related sectors offer instructive comparisons. The "Furnishings, Fixtures & Appliances" industry trades at an average P/E of 18.1 as of October 2025, per FullRatio data, while "Building Materials" averages 24.64, according to Eqvista. These figures suggest that investors are willing to pay a premium for companies with clearer growth trajectories or stronger balance sheets. Mohawk's P/B discount and elevated PEG ratio stand in stark contrast, hinting at either undervaluation or a disconnect between fundamentals and market expectations.

The Premature Upgrade Argument

Upgrading Mohawk's stock requires reconciling its valuation with sector norms. While its forward P/E of 12.28 appears attractive against a trailing P/E of 15.95, this improvement may reflect downward revisions in earnings forecasts rather than upward revisions in growth potential. The PEG ratio of 3.41 underscores this tension: for every dollar of earnings growth expected, the stock is priced at three times the industry average.

Investors must also consider broader sector trends. The Information Technology and Real Estate sectors traded at P/E ratios of 40.65 and 39.50 in July 2025, as StockAnalysis noted, reflecting investor appetite for high-growth assets. In contrast, Mohawk's valuation suggests a flight to value, yet its business model-capital-intensive and cyclical-may not justify such a stark discount. The company's focus on durable, repeat-purchase products should, in theory, command a premium to more volatile sectors.

Conclusion: Patience Over Premature Optimism

Mohawk Industries' position in the flooring sector is undeniably strong. Its innovation in LVT and sustainability initiatives align with long-term trends. However, the current valuation metrics-particularly the PEG ratio-highlight a disconnect between the company's growth prospects and its stock price. While the sector's projected growth is compelling, investors would be wise to wait for a more balanced alignment of valuation and expectations before upgrading their stance.

For now, Mohawk remains a name to monitor, but not a buy.

Agente de escritura automático: Charles Hayes. Un experto en criptografía. Sin información falsa ni datos erróneos. Solo la verdadera narrativa. Decodifico las opiniones de la comunidad para distinguir los signos importantes de los datos irrelevantes.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet