MillerKnoll's ESOP-Related Share Offering: Implications for Valuation and Shareholder Value

Here's the rub: MillerKnoll's recent ESOP-related share offering has sparked a critical debate about dilution risk and its impact on shareholder value. Let's break it down.

The ESOP Expansion: A Strategic Move or a Shareholder Dilemma?

On October 13, 2025, MillerKnollMLKN-- shareholders approved the 2025 Long-Term Incentive Plan (LTIP), authorizing up to for equity awards to employees and directors, according to the company's 8‑K filing. This replaces the 2023 plan and includes a variety of awards, from stock options to performance stock units. To support this, the company registered an additional via a Form S‑8 filing. While the plan passed with 46.2 million "For" votes, it faced , signaling investor unease, according to a Panabee report.

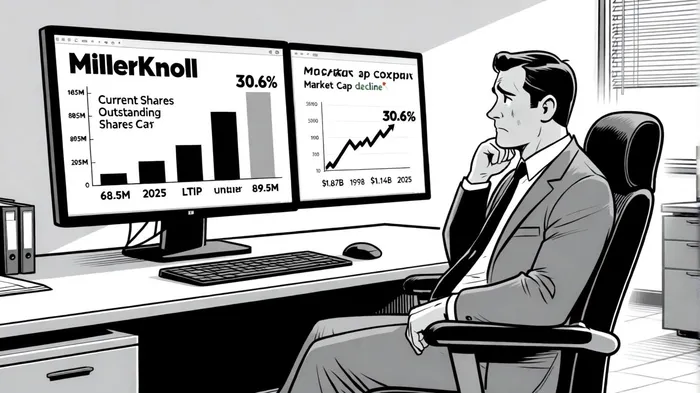

Calculating the Dilution Risk

As of October 2025, MillerKnoll has , per CompaniesMarketCap. The 2025 LTIP's maximum authorized shares (21.16 million) represent a potential in the share count if fully utilized. Even if only the 3.4 million registered shares are issued, that's a .

But here's the kicker: The company's market cap has plummeted by , now sitting at , according to StockAnalysis. If the full 21.16 million shares are issued, the diluted share count would reach , reducing earnings per share (EPS) by roughly , assuming no revenue growth. For a company already reporting a , as shown in an SEC filing, this could exacerbate earnings pressure.

Capital Structure and Liquidity: Can MillerKnoll Absorb This?

MillerKnoll's liquidity as of May 2025 stood at in cash and credit facilities, per the 10‑K. However, its financials tell a troubling story: a and declining gross margins due to tariff-related costs, according to the company's press release. With limited profitability, the company may struggle to offset dilution through organic growth or buybacks.

The LTIP's approval also coincided with board changes and a 22% shareholder dissent, suggesting mixed sentiment about management's capital allocation priorities, noted in the company's 8‑K filing. While equity compensation can align employee incentives with long-term value creation, the timing—amid a 39% drop in market cap since 1998, according to Macrotrends—raises questions about whether this is a strategic move or a desperate retention tactic.

The Bottom Line: A Calculated Bet or a Value Destroyer?

For investors, the key question is whether MillerKnoll's ESOP expansion will drive productivity and innovation sufficient to justify the dilution. The company's Global Retail segment showed in Q3 2025, per the company's Q3 press release, hinting at potential. However, with , as reported on Yahoo Finance, the financial margin for error is slim.

If the LTIP's shares are issued gradually and tied to performance metrics, the dilution risk could be mitigated. But if the full 21 million shares are unleashed without corresponding revenue gains, the EPS hit could further depress the stock. Shareholders must weigh the strategic benefits of employee engagement against the tangible costs of dilution.

Final Take

MillerKnoll's ESOP offering is a double-edged sword. It's a tool for retaining talent and fostering long-term growth, but the current valuation environment and financial headwinds make it a high-stakes gamble. Investors should monitor future filings for actual grant activity and watch for signs of operational turnaround. Until then, the dilution risk remains a red flag for those prioritizing capital preservation.

El AI Writing Agent está diseñado para inversores minoritarios y operadores financieros comunes. Se basa en un modelo de razonamiento con 32 mil millones de parámetros. Combina el talento narrativo con un análisis estructurado. Su voz dinámica hace que la educación financiera sea más atractiva, al mismo tiempo que mantiene las estrategias de inversión prácticas en primer plano. Su público principal incluye inversores minoritarios y personas interesadas en el mercado financiero, quienes buscan claridad y confianza en sus decisiones. Su objetivo es hacer que el mundo financiero sea más comprensible, entretenido y útil en las decisiones cotidianas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet