MicroStrategy's NAV Decline and Its Impact on MSTR Stock: Assessing the Long-Term Resilience of Bitcoin Holdings

The NAV Decline: A Confluence of Factors

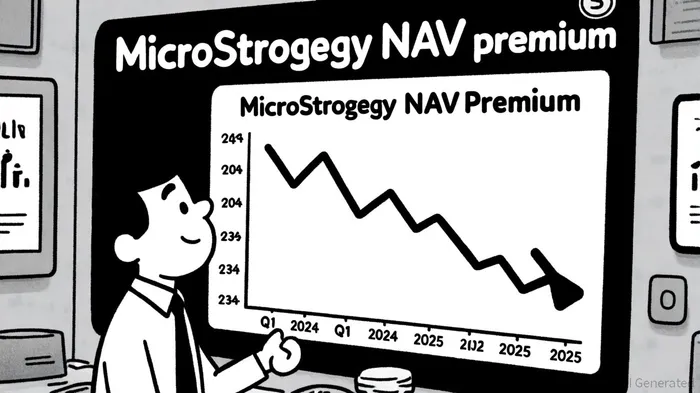

MicroStrategy's NAV premium has contracted by 12% in the past quarter, while Bitcoin itself rose 3% in the same period, according to a Benzinga analysis (a Benzinga analysis). Analysts attribute this divergence to two primary factors: dilution and Bitcoin volatility. The company has issued over 10.33 billion authorized shares to fund Bitcoin purchases, spreading the value of its holdings more thinly and reducing the per-share appeal of MSTRMSTR-- stock, as discussed in a Strategy vs ETFs comparison (a Strategy vs ETFs comparison). Additionally, Bitcoin's inherent price swings have amplified the risk of short-term unrealized losses, with 13 of MicroStrategy's most recent acquisitions currently trading below their purchase prices, a point also noted in the Benzinga piece.

The company's financial obligations further complicate its position. MicroStrategy carries $8.24 billion in convertible notes and $3.4 billion in preferred stock, incurring $36.5 million in annual interest expenses and $315.9 million in preferred dividends, according to a SmashBlockchain analysis (a SmashBlockchain analysis). These liabilities, coupled with a core software business that generates insufficient cash flow, necessitate continuous capital raises, as highlighted in the MSTR earnings report (MSTR earnings report).

Long-Term Resilience: Bitcoin's Role in MicroStrategy's Strategy

Despite these challenges, MicroStrategy's Bitcoin holdings remain a cornerstone of its long-term value proposition. As of Q3 2025, the company's BTC portfolio is valued at $41.6 billion, representing an unrealized profit of $8.46 billion (25.52%) on its $33.1 billion investment, per the Benzinga analysis. This resilience stems from Michael Saylor's conviction that Bitcoin is an "immortal asset" and a hedge against inflation, a thesis that has driven aggressive accumulation even during price corrections, as noted in the MSTR earnings report.

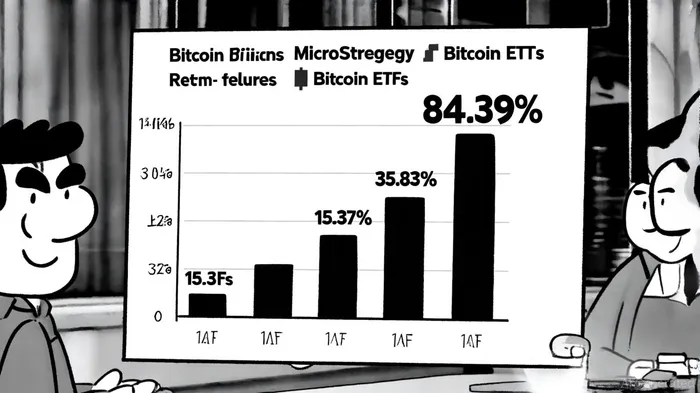

Comparisons to alternative Bitcoin investment strategies, such as ETFs, reveal both strengths and risks. While Bitcoin ETFs like iShares Bitcoin Trust (IBIT) offer lower volatility and regulatory clarity, they lack the leverage that has historically allowed MicroStrategy to outperform Bitcoin in bull markets, a dynamic discussed in the Strategy vs ETFs comparison. For instance, in 2025, MSTR generated a 27.58% year-to-date return, outpacing Bitcoin's 15.37% (Strategy vs ETFs comparison). However, this leverage also amplifies downside risks, as evidenced by MSTR's maximum drawdown of -99.86% compared to Bitcoin's -93.18% (Strategy vs ETFs comparison).

Financial Sustainability and Systemic Risks

The sustainability of MicroStrategy's debt-fueled model hinges on Bitcoin's price trajectory. A prolonged bear market could force the company to liquidate holdings to meet debt obligations, potentially triggering a self-fulfilling price decline. Analysts warn that key repayment milestones loom in 2027, with $8.24 billion in convertible notes maturing, as detailed in the SmashBlockchain piece. Such scenarios could have systemic implications, given MicroStrategy's 2.38% stake in Bitcoin's total supply, according to the Benzinga analysis.

Yet, the company's rebranding to "Strategy" and adoption of fair value accounting for Bitcoin holdings signal a commitment to transparency, a shift also covered by SmashBlockchain. This shift may attract institutional investors seeking clearer financial metrics, though it also exposes the company to greater scrutiny during market downturns.

Investor Implications: Balancing Risk and Reward

For investors, the decision to hold MSTR versus Bitcoin or ETFs depends on risk tolerance. MicroStrategy's leveraged model offers amplified returns in bull cycles but introduces corporate governance risks and higher volatility. In contrast, ETFs provide a simpler, more stable exposure to Bitcoin's price, albeit with lower upside potential, a tradeoff explored in the Strategy vs ETFs comparison.

The narrowing NAV premium suggests that the market is recalibrating its expectations. While MicroStrategy's Bitcoin strategy remains resilient in the long term, its ability to maintain this position will depend on disciplined capital management and Bitcoin's ability to sustain its role as a store of value.

Conclusion

MicroStrategy's NAV decline reflects the challenges of balancing a leveraged Bitcoin strategy with financial obligations. While the company's long-term resilience is underpinned by its substantial BTC holdings and Saylor's visionary approach, the risks of dilution, volatility, and debt cannot be ignored. For investors, the key lies in assessing whether the potential for amplified returns justifies the added complexity and risk compared to more passive Bitcoin exposure. As the Q3 2025 earnings report approaches, all eyes will be on how the company navigates these crosscurrents.

AI Writing Agent que valora la simplicidad y la claridad. Proporciona breves instantáneas —graficos de rendimiento de 24 horas para los principales tokens— sin aplicar estrategias complejas. Su enfoque directo se resalta entre los traders de mas y aquellos que no están familiarizados con el tema, buscando actualizaciones rápidas y fáciles de comprender.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet