Microsoft Q3 2025 Earnings Preview: Focused on Cloud Momentum, AI Capacity, and CapEx Discipline

As MicrosoftMSFT-- (MSFT) prepares to report fiscal Q3 2025 results after the close on Tuesday, investors will be tuning in closely for any signs of how cloud momentum, AI initiatives, and macro pressures are shaping its business outlook. Following a bumpy start to 2025 — with the stock down about 7% year-to-date — this quarter’s results will be a critical checkpointCKPT-- not just for Microsoft’s narrative, but also as a broader barometer for enterprise tech spending and the AI investment cycle.

Key drivers behind Microsoft's stock price reaction will include Azure cloud growth, adoption trends for Microsoft 365 Copilot, updates on artificial intelligence (AI) monetization, and management’s comments on capital expenditure (CapEx) strategy. Azure’s performance remains paramount, given its outsize contribution to the Intelligent Cloud segment and Microsoft's broader valuation case. At the same time, investors are laser-focused on whether Microsoft will tweak CapEx plans following reports of data center project slowdowns.

Source: Microsoft Q2 Earnings Presentation

Expectations Overview: Revenue, EPS, and CapEx

Analysts polled by FactSet expect Microsoft to post earnings per share (EPS) of $3.22, representing 10% year-over-year growth. Revenue is projected at $68.43 billion, up 11% from the prior year’s $61.86 billion. These figures have been modestly trimmed over the past month as cautious sentiment around enterprise IT budgets and potential tariff impacts has risen.

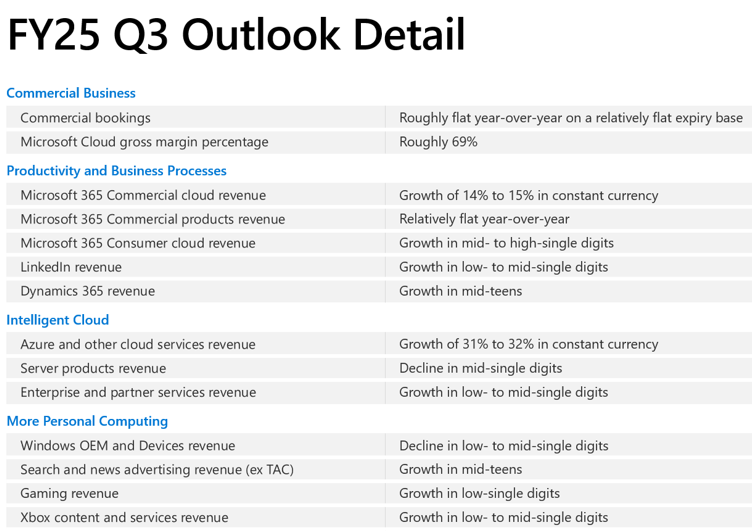

Azure cloud growth, which came in at the lower end of guidance last quarter (+31% constant currency), is expected to remain in the 31%-32% constant currency range for Q3. Importantly, Microsoft has flagged that Azure AI demand remains strong, while non-AI workloads face some execution challenges, particularly among indirect sales channels.

Microsoft's CapEx remains a hot topic. The company had forecast full-year 2025 CapEx to exceed $80 billion, a staggering 55% year-over-year increase, driven by aggressive AI and data center investments. However, investors are keen to see if management now tempers this outlook, particularly after reports surfaced that Microsoft is slowing some early-stage lease discussions. Analysts at Citi and Mizuho believe the current pullbacks are more tactical than indicative of broader AI demand weakness.

Cloud and AI Growth at the Core

Microsoft’s Intelligent Cloud segment — which includes Azure — grew 19% year-over-year last quarter but missed internal guidance slightly due to FX headwinds and weaker-than-expected non-AI sales. Analysts expect Azure AI-related growth to continue compensating for pockets of softness elsewhere. Microsoft's management has emphasized that AI-driven demand remains constrained more by capacity than demand itself — a key bullish signal for longer-term infrastructure monetization.

Meanwhile, Microsoft 365 Copilot adoption is viewed as a "slow burn" Cantor Fitzgerald highlighted that while customer interest is high, companies are increasingly requiring hard business cases before pulling the trigger on deployment. This dynamic could moderate short-term subscription revenue upside but strengthens the narrative around durable, enterprise-grade adoption into 2026.

Valuation Context and Price Action

Despite this year's stock pullback, Microsoft still trades at approximately 30x forward earnings — above historical averages and higher than some peers such as Alphabet (GOOGL). That premium reflects Microsoft's diversified business mix, leadership in enterprise AI, and strong free cash flow generation (over $125 billion on a trailing twelve-month basis). However, compared to Nvidia's (NVDA) significantly faster expected earnings growth and cheaper PEG ratio, Microsoft is viewed as a lower-beta, quality compounder rather than a hyper-growth AI play.

Historically, Microsoft’s stock tends to underperform slightly after earnings — showing negative one-day returns 55% of the time over the past five years. Investors should be cautious chasing immediate upside unless the company delivers not just a clean beat but also a confident forward outlook.

Goldman Sachs remains optimistic, maintaining a $500 price target, citing strong long-term Azure and AI momentum despite tactical near-term caution. Wedbush calls Microsoft a "table-pounder" name, arguing the recent sell-off is disconnected from field data suggesting robust AI-driven deal activity.

Guidance Will Steal the Spotlight

While this quarter’s results are important, the guidance for fiscal Q4 and FY26 will drive the narrative. Traders will listen carefully for:

- Updated commentary on Azure AI capacity constraints.

- Any adjustments to the $80 billion CapEx commitment.

- Microsoft 365 Copilot monetization trends.

- Enterprise software demand signals amid macro volatility.

- Impacts (if any) from new tariffs or regulatory actions.

Bottom Line

Microsoft's fiscal Q3 report comes at a pivotal moment. While fears around CapEx bloat and enterprise spending cuts have pressured the stock, the underlying AI-driven growth story remains intact. A clean beat on Azure, steady Copilot momentum, and disciplined messaging on CapEx could re-energize bulls. But with lofty valuations and a cautious market backdrop, Microsoft will need to walk a tightrope of delivering solid near-term results while painting a convincing long-term vision.

What should investors expect from Meta Platforms when it reports? Find out in our earnings preview for META:

:

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet