Microsoft Crushes Earnings—but AI Capacity Crunch Triggers $100B Sell-Off

Microsoft’s fiscal Q1 results were strong across nearly every line item—but the market’s focus is elsewhere. Shares are down roughly 3% in premarket trading as conservative guidance and renewed capacity constraints overshadow a beat on both earnings and revenue. The company posted $77.7B in revenue (+18% YoY, vs. $75.3B est.) and adjusted EPS of $4.13 (vs. $3.67 est.), marking solid double-digit growth across all major business units. However, management’s admission that Azure will remain capacity-constrained through fiscal 2026—despite nearly $35B in quarterly capital expenditures—has tempered enthusiasm. The setup echoes prior quarters where strong fundamentals met investor impatience for faster AI monetization.

Cloud remains the crown jewel. Microsoft Cloud revenue climbed 26% to $49.1B, and Intelligent Cloud—the segment housing Azure—jumped 28% to $30.9B, topping expectations of $30.25B. Azure and other cloud services grew 40% (39% in constant currency), beating consensus (~38%) but falling short of whisper numbers closer to 41–42%. The real story is demand: management cited “extraordinary” AI consumption that’s outpacing buildout. Commercial bookings surged 112%, while commercial remaining performance obligations (RPO) rose 51% to $392B—signaling multi-year visibility and durable growth. The problem is supply. CFO Amy Hood acknowledged the company remains “short in Azure” and expects constraints “through at least the end of the fiscal year.”

Satya Nadella called the quarter “a very strong start” as Microsoft’s “planet-scale cloud and AI factory” continues to expand. The company now serves over 900M monthly active users across its AI-enhanced products, with more than 150M users on its family of Copilots. MicrosoftMSFT-- 365 Copilot adoption rose 50% sequentially, underscoring the stickiness of AI integration within productivity software. Nadella confirmed plans to increase AI capacity by more than 80% this year and to double the total data center footprint within two years. The expansion reflects both internal demand (Copilot, Azure OpenAI Service) and external contracts—most notably OpenAI’s incremental $250B Azure commitment under an exclusive cloud arrangement extending to 2030.

Despite capacity limits, Azure continues to gain share in the hyperscale race. Its 39% constant-currency growth outpaced Google Cloud’s low-30s expansion and Amazon Web Services’ high-teens growth *AMZN reports tonight with analyst consensus at 18% YoY growth). The AI wave is a structural tailwind, driving compute intensity and stickier enterprise relationships. Commercial customers are accelerating commitments to AI workloads, fueling backlog expansion and record cRPO growth. Analysts noted that bookings are “astounding,” with short-term commitments up over 50% year-on-year, suggesting a second-half reacceleration once new capacity comes online.

Outside the cloud, the company’s diversification remains robust. The Productivity & Business Processes segment delivered $33B in revenue (+17% YoY), beating expectations on strength in Office 365, LinkedIn (+10%), and Dynamics 365 (+18%). More Personal Computing revenue came in at $13.8B (+4% YoY), also above consensus, helped by a modest recovery in Windows OEM (+6%) and a 16% jump in search and news advertising excluding TAC. Xbox content and services were flat, consistent with a normalization post-console cycle. Together, these segments illustrate a broad-based recovery from last year’s PC and ad softness, with AI now woven into nearly every surface of the business.

Expenses remain a defining feature of this new phase. CapEx soared to $34.9B in the quarter—roughly half on GPUs and CPUs—and management expects sequential increases ahead. Hood flagged that “FY26 growth in capital expenditures will exceed FY25,” reversing prior commentary suggesting moderation. Gross margin declined slightly to 69%, with Microsoft Cloud gross margin expected to dip to ~66% next quarter as AI infrastructure and the Azure mix weigh on profitability. Nonetheless, operating income still grew 24% YoY to $38B, and free cash flow rose 33% to $25.7B. The company returned $10.7B to shareholders via dividends and buybacks, maintaining capital discipline even amid historic reinvestment.

The quarter also featured a $3.1B hit tied to Microsoft’s equity method stake in OpenAI, trimming GAAP EPS by roughly $0.41. Analysts probed management on concentration risk from OpenAI and other large AI contracts, but Hood downplayed concerns, noting that the RPO is “distributed across multiple products” with a two-year weighted duration—indicating short-cycle consumption and diversified demand. Nadella reiterated that while early AI adoption has skewed toward digital-native customers, enterprise adoption is “just starting,” implying a longer runway for expansion.

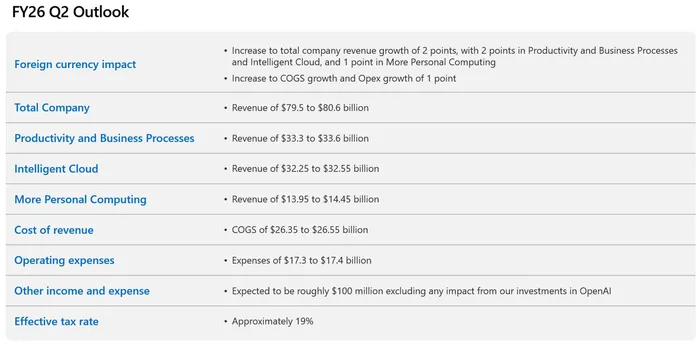

Looking forward, Microsoft guided fiscal Q2 revenue to $79.5B–$80.6B, roughly in line with consensus at the midpoint ($80.05B). The company expects Azure constant-currency growth of ~37%, essentially maintaining current momentum but below bulls’ hopes for a faster reacceleration. Cloud gross margin is guided to ~66%, down YoY due to continued AI investment. COGS is projected at $26.35B–$26.55B, opex at $17.3B–$17.4B, and operating margin flat YoY, down sequentially due to seasonal factors.

While guidance may look cautious, it’s not new behavior. Microsoft has a history of sandbagging AI-related outlays and cloud growth targets, only to exceed them as infrastructure comes online. Citi called the setup “constructive,” noting that commercial RPO and bookings “give us confidence that Azure will reaccelerate in 2H,” and reiterated a $690 price target. KeyBank remains overweight, saying the quarter was “not thesis-changing.” The consensus takeaway: demand is intact, but supply will dictate near-term growth cadence.

Technically, MSFT’s stock broke out above $530 ahead of earnings and now trades near that level again—a critical short-term test. With the stock down 3% pre-market, investors are recalibrating for a heavier CapEx glidepath rather than a slowdown. Yet, the strategic message is consistent: Microsoft is building the world’s largest AI infrastructure platform and monetizing it across every product line.

In short, fiscal Q1 reaffirmed the strength of Microsoft’s AI-fueled ecosystem even as the pace of capacity expansion tempers the near-term narrative. Azure growth of 40%, record bookings, and surging AI adoption validate the long-term story. The short-term reaction reflects déjà vu—investors fixating on cost optics while the demand curve steepens. If history is any guide, those willing to look past another quarter of CapEx indigestion may find that the true constraint isn’t capacity—it’s investor patience.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet