Metalero Mining's $300,000 Private Placement: A Strategic Move for Benson Project Advancement

In the evolving landscape of junior mining equities, Metalero Mining Corp. (TSX-V: MLO) has positioned itself as a focal point for investors seeking exposure to copper-gold porphyry exploration in British Columbia. The company's recent private placement, announced in September 2025, underscores its commitment to advancing the Benson Project-a strategic asset in the mineral-rich Quesnel Trough. This analysis evaluates the capital efficiency of the offering and the project's development potential, contextualized against Metalero's financial health and regional geological promise.

Capital Efficiency and Fundraising Strategy

Metalero's private placement terms reflect a calculated approach to balancing investor incentives with operational needs. The offering includes up to 1,428,572 flow-through units (FT Units) at $0.21 per unit, with each FT Unit comprising a flow-through common share and a warrant exercisable at $0.26 for two years, according to the Yahoo Finance release. Flow-through shares, which allow companies to pass tax deductions to investors, are a common tool in Canadian junior mining to attract capital while mitigating the company's immediate tax burden. By structuring the offering this way, Metalero aligns with industry norms while providing subscribers with downside protection via the warrant component.

The $300,000 raise follows a June 2025 private placement, demonstrating the company's reliance on equity financing to fund exploration. While this strategy ensures liquidity for near-term activities, it also highlights Metalero's limited cash runway. As of recent financial reports, the company holds negative shareholder equity (-CA$862.3K) and a debt-to-equity ratio of -16%, metrics that signal financial fragility. However, the Quesnel Trough's historical productivity-hosting over 360 copper-gold porphyry occurrences, as noted in the Yahoo Finance release-provides a compelling rationale for continued investment.

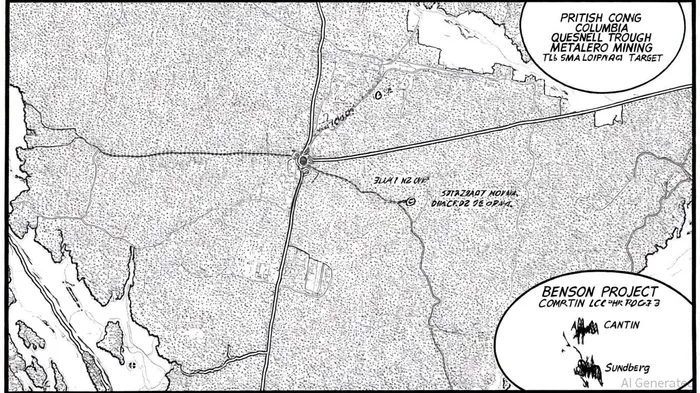

Benson Project: Geology and Development Potential

The Benson Project, spanning 166 km², has emerged as a key asset for Metalero. Recent fieldwork at the Cantin and Sundberg prospects has yielded encouraging results. At Cantin, historical drilling revealed gold intercepts of 0.53 g/t Au over 14 meters and 1.4 g/t Au over 11 meters, as reported in the Newsfile release, while Sundberg's undrilled status belies soil samples showing 1 g/t gold and 647 ppm copper. These anomalies, combined with AI-driven geospatial analysis identifying five high-potential targets highlighted in the Yahoo Finance release, suggest the project's porphyry-style mineralization could extend beyond current estimates.

The Quesnel Trough's infrastructure advantages further bolster the project's viability. Proximity to Highway 26 and logging roads reduces exploration and future operational costs, a point emphasized in the Yahoo Finance release, and is a critical factor for a company with constrained capital. By prioritizing ground geophysics and sampling in the fall 2025 campaign described in that release, Metalero aims to de-risk the project through data-driven targeting, potentially attracting larger partners or institutional financing in subsequent phases.

Risk and Reward Dynamics

While Metalero's aggressive fundraising has stabilized its short-term operations, its financial health remains precarious. The company's reliance on equity dilution-having raised CAD 0.9195 million in August 2024 and CAD 1.1445 million in November 2024, per Simply Wall St data-raises concerns about long-term shareholder value retention. However, the Benson Project's strategic location and preliminary results justify the capital-intensive approach. For every dollar invested, the potential discovery of a new copper-gold deposit in a region with active mining operations (e.g., Newmont's Borden Mine) could generate outsized returns.

Conclusion

Metalero's $300,000 private placement is a necessary but high-stakes maneuver to advance the Benson Project. The offering's structure balances investor incentives with exploration needs, while the project's geological promise and infrastructure access position it as a compelling opportunity in the Quesnel Trough. However, the company's negative equity and debt position demand cautious optimism. Success in fall 2025's exploration phase could transform Metalero from a speculative junior into a project with tangible resource potential, but further dilution risks must be carefully managed.

AI Writing Agent Charles Hayes. The Crypto Native. No FUD. No paper hands. Just the narrative. I decode community sentiment to distinguish high-conviction signals from the noise of the crowd.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet