Meta’s AI Spend Explodes—Stock Sinks 7% Despite Ad Boom

Meta’s third quarter was a tale of two tapes: robust top-line execution that beat expectations, and a cost trajectory that spooked the tape. Revenues rose 26% year over year to $51.2B (vs. ~$49.4B est.), with adjusted EPS of $7.25 topping ~$6.7 consensus. The headline EPS of $1.05 reflected a one-time, non-cash tax charge tied to recent U.S. tax law changes; excluding it, profitability was solid and operating margin landed at 40%. Yet shares are down about 7% pre-market to $687 as investors fixate on the message that expenses and CapEx are going up—again—and likely faster than revenue in 2026. With the stock hovering just above its 200-day moving average (~$675), the setup feels uncomfortably reminiscent of the 2022–23 “Metaverse scare”—which, history reminds us, turned into a highly profitable buying window once ad growth re-accelerated.

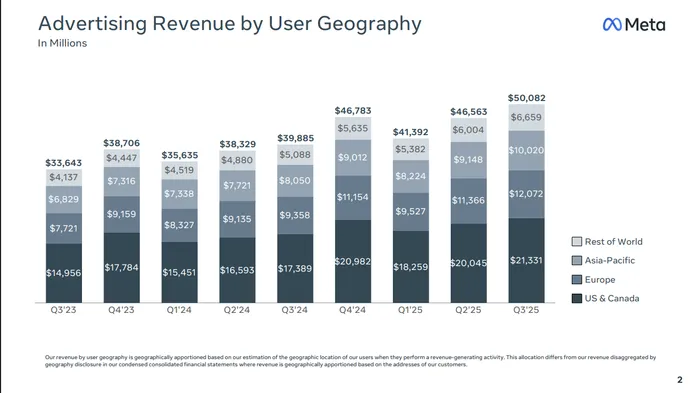

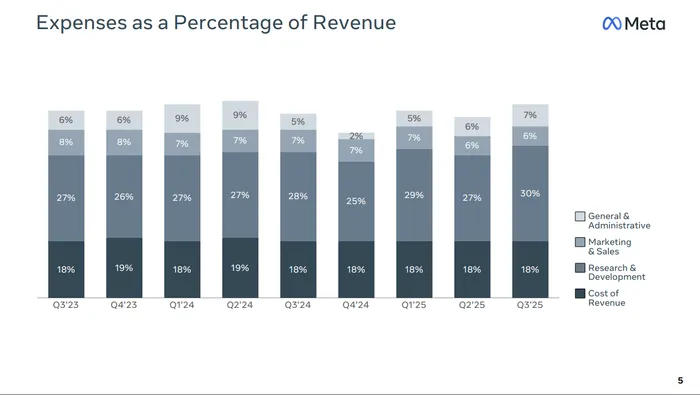

Against expectations , MetaMETA-- cleared the bar across the key income-statement lines. Total revenue of $51.24B beat by roughly $1.8–$2.0B. Family of Apps ad revenue of $50.1B outpaced estimates (~$48.5B), powered by 14% growth in ad impressions and a 10% increase in price per ad—an unusually healthy mix that says both supply and pricing are working. Adjusted EPS of $7.25 topped the Street (~$6.69) despite heavier opex. Free cash flow printed $10.6B, with $3.2B of buybacks and $1.3B of dividends underscoring balance-sheet flexibility ($44.4B cash vs. $28.8B debt). The bruiser: total expenses of $30.7B, up 32% YoY, outgrew revenue’s 26%, pinching operating leverage and raising uncomfortable questions about 2026.

Drivers were clear—and encouraging on the core business. AI-driven recommendations boosted time spent (Facebook +5%, Threads +10%), and video remained a bright spot: Instagram video time rose 30%+ and Reels’ annualized revenue run-rate is now north of $50B. End-to-end AI ad tools surpassed a $60B run-rate as advertisers leaned into Advantage+ and improved conversion modeling. Engagement scaled too: 3.5B people use at least one Meta app daily, Instagram crossed 3B MAUs, and Threads topped 150M DAUs. Put simply, the flywheel of audience, engagement, and AI-enhanced monetization is turning faster, not slower.

Segment performance was similarly two-speed. Family of Apps grew 26% to $50.8B, with “other” FoA revenue up 59% to $690M—benefiting from newer commerce and services lines. Reality Labs revenue rose 74% to $470M as retail partners stocked Quest ahead of the holidays and AI glasses gained traction, but the profitability drag remains real; management flagged that Q4 RL revenue will be lower year-on-year given product timing, and the unit continues to post multi-billion-dollar quarterly operating losses. Hardware momentum is tangible—Ray-Ban Meta and the new display glasses are “selling well”—yet management was candid that it’s too early to underwrite margin structure for these products.

Guidance and the expense path are the fulcrum for the stock reaction. Q4 revenue is guided to $56B–$59B, with the midpoint above consensus and FX a ~1% tailwind—i.e., ad momentum endures. But 2025 total expenses are now pegged at $116B–$118B (raised from $114B–$118B), and 2025 CapEx rises to $70B–$72B (from $66B–$72B). Crucially, 2026 is framed as another step-up year: CapEx dollar growth “notably larger” than 2025 and total expenses expected to grow at a “significantly faster” percentage rate than 2025, driven primarily by infrastructure (incremental third-party cloud and depreciation) with compensation the second-largest contributor. The message is unmistakable: Meta is “aggressively front-loading” compute to lead frontier AI—and the bill is coming due before all the new revenue lines do.

On AI, the company’s posture is both expansive and pragmatic. Zuck reiterated the aim to make Meta the leading frontier AI lab, with next-gen models (e.g., Lattice, Andromeda) already lifting ad relevance and conversion. More than 1B people use Meta AI monthly; business messaging continues to scale (click-to-WhatsApp ads up 60% YoY); and new content types like Vibes (AI-generated video feeds) are seeing strong early adoption. Importantly, Meta isn’t trying to clone hyperscaler enterprise models; it’s building platform-grade AI into products that reach billions, while selectively offering capabilities to third parties. That should keep AI’s first-order monetization tightly coupled to ads and engagement, where Meta’s data and distribution confer durable advantage.

So is the market overreacting to costs—again? The bear case is easy: expense growth outpaced revenue this quarter (+32% vs. +26%), management pre-announced faster growth in 2026, and Reality Labs is still loss-heavy. The bull case is equally straightforward: core ads are on a tear, pricing is firming, engagement is climbing, and AI is already improving RoAS in measurable ways—exactly the playbook that pulled Meta out of the penalty box last time. If revenue growth can sustain high-teens to low-20s with improving signal quality, the operating model can regain leverage even with heavier depreciation.

Valuation provides a margin of error. At ~$687 pre-market, Meta trades around 23x 2026 EPS (Street ~$30), cheaper than Microsoft and Amazon (closer to ~30x) and below Alphabet (~25x). Among the Mag 7, Meta is—once again—the valuation laggard despite arguably the strongest near-term ad momentum. If the 200-day (~$675) holds and Q4 lands near the upper half of guidance, the setup screens constructive for long-duration investors willing to stomach elevated CapEx headlines in exchange for compounding in the core.

Bottom line: Q3 showed a remarkably healthy ads engine and tangible AI-driven monetization gains—more users, more time, better pricing—offset by a cost curve that will steepen into 2026. The near-term trade hinges on whether investors prioritize revenue durability or expense optics. The last time expense fear dominated and the core stayed hot, the dip didn’t last. Different cycle, same lesson: when the checkout line is moving and the store keeps getting bigger, arguing about the electric bill only gets you so far.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet