Merck KGaA (ETR:MRK): A Hidden Gem or Overvalued Mirage?

The stock market is a game of contradictions, and right now, MerckMRK-- KGaA (ETR:MRK) is playing both ends against the middle. On one hand, analysts are screaming buy with consensus price targets nearly 44% above current levels, backed by discounted cash flow (DCF) models that say the stock is 50% undervalued. On the other, the stock has been stuck in a €100–€120 trading range for months, with some analysts even calling it a sell. What's the disconnect here? Let's dig in.

The Numbers Are Shouting “BUY,” But the Market Isn't Listening

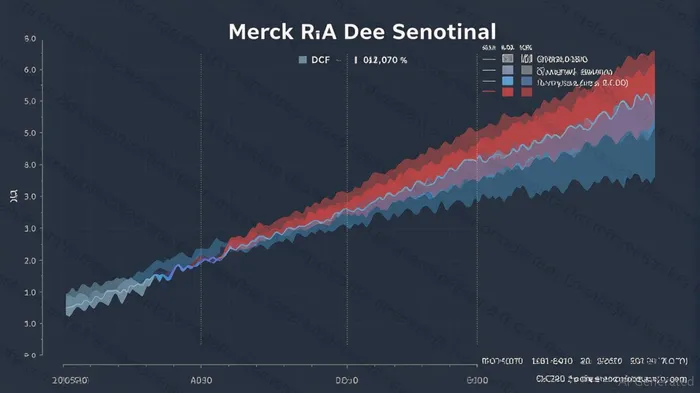

The math is undeniable: as of July 2025, Merck's DCF fair value is estimated at €222.92 per share by Simply Wall St, yet the stock trades at just €111.25—a 50.1% discount. Analysts' average price target of €159.88 (with a high of €182.00) suggests the market isn't pricing in the full potential of this German conglomerate.

But why the lag? Let's look behind the curtain.

The M&A Play: Betting on Rare Diseases and Semiconductors

Merck's strategy isn't just about buying high-flying companies—it's about owning the future of healthcare and tech. Take its €3.9 billion acquisition of SpringWorks Therapeutics in 2025, which gave it two FDA-approved drugs for rare tumors: Ogsiveo (desmoid tumors) and Gomekli (neurofibromatosis). These aren't just niche products—they're blockbuster opportunities in a world where orphan drugs command sky-high prices.

But here's the catch: these drugs are still in early commercialization stages. The market is skeptical about how quickly Merck can monetize this bet. Meanwhile, in the semiconductor materials space, Merck is doubling down on AI-driven demand for advanced chips, a sector that's red-hot but volatile.

Divisional Disparity: Healthcare Shines, Life Science Stumbles

Merck's divisions are like a seesaw. Healthcare is soaring:

- Oncology sales grew 12.7% in 2024, led by Erbitux, while SpringWorks' assets are expected to add €1.5 billion in annual sales by 2030.

- Neurology & Immunology saw 12.3% growth from Mavenclad, despite looming patent cliffs.

But Life Science is the laggard:

- Sales fell 3.3% in 2024 due to post-pandemic destocking and weak U.S. academic spending.

- The division's recovery is slow, with 2025 sales growth guidance cut to 2–7% from earlier expectations.

This split creates a valuation paradox: Healthcare's long-term potential is undeniable, but near-term Life Science headwinds are keeping shares grounded.

The Bulls' Case: This Is a Buy-and-Forget Stock

The bulls see Merck as a compounder of opportunities:

1. DCF math wins over time: At €222.92 fair value, even a half-way reversion to €160 would mean 44% upside from current levels.

2. M&A discipline: Unlike Big Pharma's overpriced deals, Merck's SpringWorks purchase at a 26% premium looks aggressive but strategically sound in a rare disease gold rush.

3. Dividend stability: The proposed €2.20 dividend (a 2% yield) offers a safety net in volatile markets.

The Bears' Warning: Growth Hurdles and PEG Ratio Red Flags

The skeptics aren't wrong either:

- PEG ratio of 2.2x: This suggests investors are already pricing in aggressive growth, leaving little margin for error if earnings miss.

- Life Science's slow recovery: A prolonged slump here could drag down overall margins.

- Regulatory risks: SpringWorks' drugs face European approvals that could delay revenue ramp-up.

The Bottom Line: Buy the Dip, But Set Traps

Merck KGaA is a textbook “value trap”… or a screaming bargain. The DCF undervaluation is too stark to ignore, and the analyst consensus isn't this bullish unless there's real catalysts (like FDA approvals or semiconductor demand spikes).

Action Plan:

- Buy if it dips below €100: That's a 20% discount to current levels and offers a margin of safety.

- Sell if it breaches €150: That's the consensus target ceiling, and greed could push it higher—but don't get greedy.

- Avoid at all costs if Life Science's EBITDA misses guidance by >5% in Q3.

This isn't a “buy and hold forever” stock—it's a strategic call option on healthcare innovation and tech demand. The math says BUY, but the execution has to deliver.

Stay hungry, stay foolish, but stay diversified.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet