MELI vs. SE: Which E-Commerce Stock Offers Better Growth Opportunity?

MercadoLibre MELI is the dominant e-commerce and fintech platform across Latin America, while Sea Limited SE operates Shopee, a leading e-commerce marketplace in Southeast Asia.

Both companies focus specifically on emerging markets and combine online retail with fintech ecosystems to drive user engagement. This dual-engine model — commerce and payments — has become central to the expansion of the digital economy in regions with low penetration of traditional banking systems.

Per the Grand View Research report, the global e-commerce market is set to grow strongly through 2033, driven by rising internet access and smartphone usage in emerging markets. This creates solid opportunities for both companies. So, which stock has more upside today — MELIMELI-- or SE?

The Case for MercadoLibreMELI-- Stock

MercadoLibre leads the Latin American e-commerce space, commanding over 30% market share in countries such as Brazil, Argentina and Mexico. The region’s low digital adoption supports a strong long-term growth outlook.

The company benefits from a deeply integrated ecosystem that combines marketplace, logistics and fintech. Its logistics network enables fast delivery (75% within 48 hours), lowering costs and improving user experience. Its fintech arm, Mercado Pago, is a major growth engine, with 78 million monthly active users and a $12.5 billion credit portfolio as of the fourth quarter of 2025. AI-driven tools across search, advertising and fintech further enhance monetization and efficiency.

The growth of e-commerce in Latin America is significantly lower than in developed markets, which creates potential for long-term expansion. Fintech growth is driven by financial inclusion, with low credit card penetration in key markets. Cross-border trade, first-party retail (1P), advertising and AI-led personalization provide additional growth levers.

However, aggressive investments in free shipping, credit expansion and cross-border logistics are putting pressure on margins, with additional risks stemming from credit exposure, higher funding costs and macro instability in markets like Argentina.

Overall, MercadoLibre is prioritizing long-term scale and ecosystem dominance over short-term profitability, positioning itself as a leading digital commerce and financial platform in emerging markets.

The Zacks Consensus Estimate for MELI's 2026 earnings is pegged at $52.27 per share, down 13% over the past 30 days. Despite this near-term estimate cut, the projection still implies a strong 32.66% year-over-year increase, indicating sustained long-term growth momentum.

Image Source: Zacks Investment Research

The Case for Sea LimitedSE-- Stock

Sea Limited is facing growing challenges in its e-commerce and fintech segments despite strong growth. Its profitability remains under pressure due to high operating costs and rising risk exposure. In Shopee (e-commerce), heavy spending on logistics, free shipping and customer incentives is pushing costs higher. In fact, costs grew faster than revenues, rising 40.4% year over year in the fourth quarter of 2025, reflecting heavy operational intensity and margin pressure. Marketing expenses also jumped 33.6%, showing that the company still depends heavily on promotions to attract users. At the same time, revenues from value-added services declined due to shipping subsidies, highlighting weak monetization quality in parts of the business.

In fintech (Monee), rapid credit expansion is increasing risk levels, as provision for credit losses jumped 66.7% year over year in the fourth quarter, showing higher exposure to potential defaults. While non-performing loans remain stable at 1.1%, the sharp 80% yearly rise in lending raises concerns about future loan repayment. The shift to an “all-can-apply” credit model further increases underwriting risk. Additionally, rising funding, compliance and macro risks in emerging markets remain key overhangs.

Despite these challenges, Sea Limited shows strong positives. In 2025, Shopee’s GMV reached $127 billion, supported by better advertising revenues and strong user engagement from around 400 million buyers. Its growing logistics network, along with initiatives like the VIP membership program and faster delivery, is helping retain customers. In fintech, revenues grew 60% year over year, and the expansion beyond e-commerce into broader use cases offers solid long-term growth potential.

The Zacks Consensus Estimate for SE's 2026 earnings is pegged at $4.85 per share, down 6% over the past 30 days, indicating slightly tempered earnings expectations.

Image Source: Zacks Investment Research

MELI vs. SE: Price Performance & Valuation

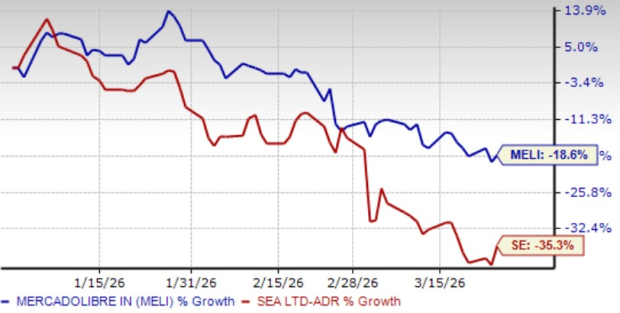

Year to date, MercadoLibre has performed much better than Sea Limited, with its shares declining 18.6% compared with a steeper 35.3% drop for Sea Limited.

SE’s lackluster price performance is mainly due to high operating and logistics expenses, increasing credit risk in fintech, and shrinking value-added services revenues amid shipping subsidies, highlighting challenges in delivering high-quality, profitable growth.

MELI’s relatively stronger performance has been supported by balanced growth in e-commerce and fintech business, backed by improved logistics and AI tools that help increase sales and user activity.

YTD Price Return Performance

Image Source: Zacks Investment Research

MELI Appears to be Pricier Than SE

MELI is trading at a forward 12-month price-to-sales (P/S) multiple of 2.06X. It has a Value Score of B. Meanwhile, SE has a Value Score of C, with its forward sales multiple at 1.54X. Despite trading at a higher P/S multiple, MELI’s valuation premium is supported by strong top-line growth, rapid fintech expansion and strong network effects across its e-commerce and payments platform.

MELI vs. SE: P/S F12M Ratio

Image Source: Zacks Investment Research

MELI or SE: Which Is a Better Pick?

MercadoLibre appears better positioned than Sea Limited, backed by its stronger ecosystem integration, improved logistics efficiency, and more balanced growth between commerce and fintech. While SE offers growth potential, its margin pressures and rising credit risks remain concerns. Despite a higher valuation, MELI offers a more balanced and reliable long-term investment case.

Compared with MercadoLibre’s Zacks Rank #3 (Hold), Sea Limited’s Zacks Rank #4 (Sell) suggests lower analyst confidence in near-term performance.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Sea Limited Sponsored ADR (SE): Free Stock Analysis Report

MercadoLibre, Inc. (MELI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet