Medicare Premium Hikes and Their Financial Impact on Retirees in 2026: How Rising Healthcare Costs Are Reshaping Retirement Portfolios

The Erosion of COLA and the Hold-Harmless Provision

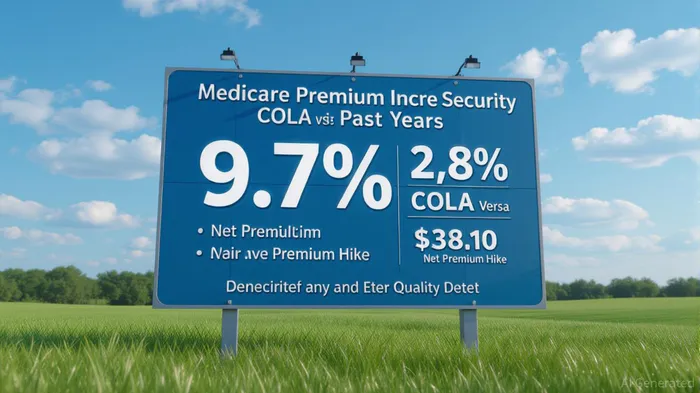

The disparity between Medicare premium hikes and COLA adjustments has long been a point of contention. In 2026, the situation is particularly acute. The hold-harmless provision, which prevents the full premium increase from being deducted from for beneficiaries with benefits of $640 or less, will protect approximately four million low-income retirees. However, for those earning above this threshold, the financial strain is palpable. According to a report by MarketWatch, the Part B premium increase effectively erodes one-third of the average COLA, leaving retirees to grapple with higher out-of-pocket costs for healthcare while their Social Security benefits grow at a fraction of the rate.

High-Income Retirees and the IRMAA Surcharge

The financial burden is even starker for high-income retirees, who face additional surcharges under the (IRMAA). In 2025, , depending on their income tier. For example, . , .

To mitigate this, retirees are increasingly adopting strategic tax planning. Timing Roth conversions carefully to avoid triggering higher IRMAA brackets, utilizing (QCDs) to reduce taxable income, and coordinating distributions from taxable, tax-deferred, and Roth accounts are becoming standard practices. For instance, QCDs allow individuals aged 70½ or older to donate directly from IRAs to charities, lowering AGI without increasing Medicare premiums.

To mitigate this, retirees are increasingly adopting strategic tax planning. Timing Roth conversions carefully to avoid triggering higher IRMAA brackets, utilizing (QCDs) to reduce taxable income, and coordinating distributions from taxable, tax-deferred, and Roth accounts are becoming standard practices. For instance, QCDs allow individuals aged 70½ or older to donate directly from IRAs to charities, lowering AGI without increasing Medicare premiums.

Elder Care Economics and the Broader Cost-of-Care Crisis

Beyond Medicare premiums, the broader landscape of elder care economics is equally daunting. U.S. . Elder care costs, including nursing home and in-home services, have surged dramatically. , . These trends are compounded by the growing number of unpaid caregivers, often at significant financial and emotional cost.

For retirees, these costs necessitate a reevaluation of retirement portfolios. Experts recommend diversifying into long-term care insurance, (HSAs), and or plans to cover gaps in Original Medicare. HSAs, in particular, offer triple tax advantages and can be used to pay for qualified elder care expenses, making them a cornerstone of modern retirement planning.

Policy Shifts and Market Dynamics

The Medicare Advantage (MA) market is also evolving in response to these pressures. Companies like GoHealth are prioritizing member retention and unit economics over expansion, signaling a shift toward disciplined growth. The industry is increasingly focusing on , which offer targeted care for beneficiaries with chronic conditions, reflecting a broader emphasis on value and continuity of care. Meanwhile, by 90%, have helped temper premium increases but highlight the fragility of the system.

Conclusion: Proactive Planning in a High-Cost Environment

The 2026 Medicare premium hikes underscore the urgent need for retirees to adopt proactive financial strategies. For high-income individuals, managing MAGI through tax-efficient distributions and Roth conversions is critical to avoiding IRMAA surcharges. For all retirees, annual reviews of Medicare plans and elder care budgets are essential, particularly as out-of-pocket costs and long-term care expenses continue to rise.

As healthcare costs outpace inflation and elder care demands grow, retirement portfolios must evolve to prioritize flexibility and resilience. The coming years will test the adaptability of retirees and their advisors, but with careful planning, it is possible to navigate these challenges without sacrificing financial security.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet