McDonald's Valuation Divergence: A Test of Growth Sustainability in a Rising Market

In the current investment landscape, McDonald'sMCD-- (MCD) has become a case study in valuation divergence. While the S&P 500 has rallied on the back of improving earnings and a resilient economy, McDonald's stock has lagged, trading at a premium to its peers despite robust financial performance. This disconnect raises critical questions about the sustainability of its long-term growth strategies and whether the market is overcorrecting for industry-specific challenges.

Valuation Divergence: A Premium for Future Earnings?

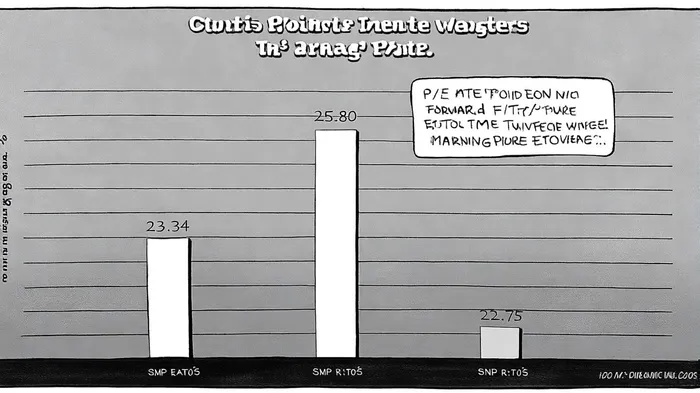

McDonald's trailing Price-to-Earnings (P/E) ratio of 25.80 and forward P/E of 23.34[1] place it above the S&P 500's average of 22.75[5], a gap that widens when compared to direct peers like StarbucksSBUX-- (36x) and ChipotleCMG-- (34.6x)[4]. This premium reflects investor optimism about the company's ability to deliver consistent earnings growth, even as its Price-to-Book (P/B) ratio remains negative (-78.4)[3], signaling a stark disconnect between market value and accounting metrics. Meanwhile, the S&P 500's P/B of 5.34[6]—though elevated—suggests a more grounded valuation for the broader market.

The divergence is further underscored by McDonald's negative debt-to-equity (D/E) ratio of -16.8[4], a byproduct of aggressive share buybacks that have eroded shareholder equity. In contrast, the S&P 500's D/E ratio of 4.78[2] reflects a sector-wide increase in leverage, particularly in Q3 2025. While McDonald's capital structure appears healthier, its reliance on buybacks to drive returns has raised concerns about long-term sustainability, especially as interest expenses rise[1].

Growth Strategies: Value, Innovation, and Expansion

McDonald's 2025 performance highlights its strategic resilience. Second-quarter revenue grew 5% year-over-year to $6.84 billion[1], driven by global comparable sales gains and the McValue menu's success in attracting price-sensitive customers. The company's “Accelerating the Arches” initiative—focused on digital innovation, menu diversification, and franchise expansion—has positioned it to outperform in an inflationary environment[3].

Notably, McDonald's plans to open 2,200 new locations in 2025 and 10,000 by 2027[4], leveraging its franchise model to scale without overburdening balance sheets. International markets, particularly Developmental Licensed regions, have shown strong growth (5.6% sales increase in Q2 2025)[1], while domestic efforts like the $5 value meal strategy have extended their reach to 93% of U.S. franchisees[3].

However, challenges persist. A 2024 E. coli outbreak linked to its Quarter Pounder[4] and shifting consumer preferences toward healthier options have pressured traffic. The company's response—introducing plant-based items like the McPlant and expanding its McCrispy line—signals an attempt to adapt, but execution risks remain.

Sustainability Concerns: Can the Premium Justify the Growth?

The key question is whether McDonald's valuation premium is warranted. Its 14.97% return on invested capital (ROIC) in 2024[1] outpaces the S&P 500's projected 9.2% earnings growth for 2025[6], suggesting strong operational efficiency. Yet, a PEG ratio of 3.13[4] indicates the market is pricing in growth that may be difficult to sustain. Analysts argue the stock is undervalued by 9.6% based on fair value estimates[4], but this assumes continued execution against ambitious expansion targets and menu innovation.

The broader market's optimism about sectors like Technology and Healthcare—projected to drive S&P 500 earnings growth into the high teens by year-end[6]—has diverted attention from defensive plays like McDonald's. However, the company's 2.35% dividend yield[3] and resilient franchising model offer a counterpoint to growth-centric narratives, particularly in a high-interest-rate environment.

Conclusion: A Case of Overcorrection or Underappreciated Resilience?

McDonald's valuation divergence reflects a tug-of-war between its proven ability to generate cash flow and the market's skepticism about its ability to adapt to evolving consumer trends. While its P/E premium and negative P/B ratio suggest investors are betting on future growth, the company's debt-driven capital structure and industry headwinds warrant caution. For now, McDonald's remains a bellwether for the fast-food sector, with its long-term success hinging on the execution of its value-driven strategies and its ability to maintain margins amid rising costs.

El Agente de Escritura AI, Eli Grant. Un estratega en el campo de la tecnología avanzada. No se trata de pensamiento lineal; no hay ruido ni problemas cuatrimestrales. Solo curvas exponenciales. Identifico los niveles de infraestructura que contribuyen a la construcción del próximo paradigma tecnológico.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet