McCormick Reaffirms 2025 Outlook Despite Q1 Miss and Tariff Headwinds; Stock Tests Key Support

McCormick & Company (MKC) reported mixed fiscal first-quarter results Tuesday morning, delivering in-line revenue but missing on earnings. Despite near-term headwinds tied to costs and foreign exchange, the spice and flavoring giant reaffirmed its full-year 2025 guidance—a move that comes at a critical juncture for the stock as it hovers near its 200-day moving average. The reaffirmation helped temper fears about escalating tariff impacts on McCormick’s high-margin spice business, a key concern across the broader consumer staples space.

For the first quarter, McCormickMKC.V-- reported adjusted EPS of $0.60, falling short of consensus estimates for $0.64 and down from $0.63 a year ago. Revenue came in at $1.61 billion, up just 0.2% year-over-year and exactly in line with Wall Street expectations. Gross profit margin improved modestly by 20 basis points to 37.6%, slightly ahead of the 37.5% estimate, aided by cost savings from the company’s ongoing Comprehensive Continuous Improvement (CCI) initiative.

The softer-than-expected bottom line was primarily due to increased selling, general, and administrative expenses, including a shift in the timing of stock-based compensation and higher brand marketing investments. Operating income for the quarter fell to $225 million from $234 million a year ago, while adjusted operating income declined 5% year-over-year (or 3% in constant currency).

Segment performance was mixed. The Consumer segment, McCormick’s core business, posted flat sales of $919 million with organic sales up just 1%. Operating income in the Consumer unit, excluding special charges, fell 17%, reflecting pressure from pricing actions and elevated marketing spend. In contrast, the Flavor Solutions segment showed strength, with sales rising 1% (3% organic) to $686 million and operating income jumping 28% (33% in constant currency). Management credited improved product mix, pricing, and CCI-driven efficiencies for the outperformance in the business-to-business segment.

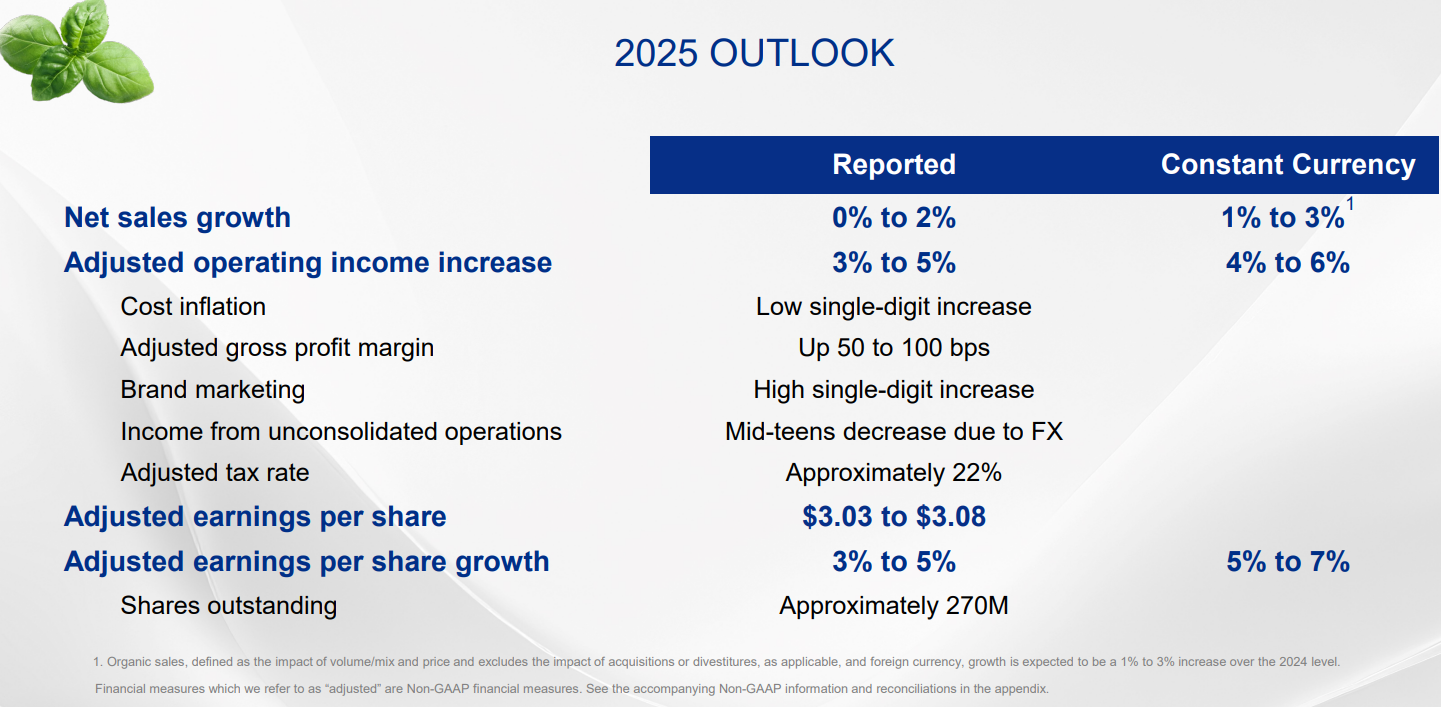

Importantly, McCormick reaffirmed its full-year fiscal 2025 outlook—a key signal of management confidence given macro uncertainty and looming tariff threats. The company continues to expect:

- Adjusted EPS between $3.03 and $3.08 (vs. Street at $3.07),

- Net sales growth of 0% to 2% as reported (1% to 3% constant currency),

- Adjusted operating income growth of 3% to 5% reported (4% to 6% constant currency).

This reaffirmation carries added significance as McCormick has historically only deviated from reaffirming full-year guidance during periods of major disruption—namely during COVID-19 in 2020 and again in 2021 following a large acquisition. In the other four of the last six Q1 releases, guidance was maintained.

On tariffs, which are increasingly viewed as a threat to McCormick’s spice business due to reliance on Chinese imports, the company addressed the issue directly. Management stated that current tariff impacts have been accounted for in the outlook and are being offset through CCI cost savings and targeted price increases. However, McCormick also acknowledged that the guidance does not include any potential future tariffs or retaliatory actions, citing the ongoing lack of clarity around the April 2 policy shift.

Currency remains a drag across both segments. The company noted a 2% unfavorable impact to sales and operating income in Q1 from FX, with a roughly $0.03 per share negative effect on EPS tied primarily to weakness in income from unconsolidated operations in Mexico. That FX headwind is expected to persist throughout 2025.

Shares of MKCMKC-- were down approximately 2% in early trading following the report, setting up a technical test of its 200-day moving average at the $77 level. This is widely viewed as “must-hold” territory for the stock, with a break lower likely to invite further downside momentum.

In the broader context, McCormick’s results may offer a cautionary tale for consumer staples names exposed to tariff volatility and FX pressures. While the reaffirmed guidance offers some reassurance, investors are clearly demanding cleaner execution amid the uncertainty. With macro risks unresolved and more tariff headlines looming next week, MKC’s near-term trajectory remains delicately balanced.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet