Maximizing Tax Efficiency: Strategic Moves Before the June 16 Deadline

As the June 16 estimated tax deadline approaches, investors face a critical juncture to optimize their cash flow and minimize tax liabilities. With the IRS adjusting key thresholds for 2025—including higher estate tax exclusions, expanded health savings account limits, and refined rules for investment income—the timing is ideal to recalibrate strategies that align with these changes. For long-term wealth accumulation, tax efficiency is not just an annual chore but a cornerstone of sustainable growth.

The June 16 Deadline: A Quarter in Review

The second-quarter deadline applies to income earned between April 1 and May 31, 2025, requiring taxpayers to submit payments by June 16 to avoid penalties. This includes self-employed individuals, investors with significant capital gains, and those relying on rental or dividend income. The IRS's "pay-as-you-go" system demands proactive management, especially as 90% of 2025 taxes or 100% of 2024 taxes must be paid to avoid underpayment penalties. For high-income earners (AGI over $150,000), the threshold rises to 110% of prior-year taxes, emphasizing the need for precise calculations.

Key Adjustments to Leverage

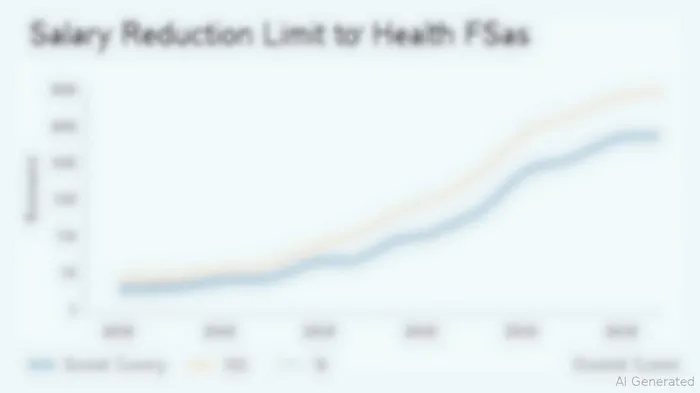

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs):

The 2025 FSA limit rises to $3,300, with a carryover of up to $660—a 3% increase from 2024. HSAs remain tax-advantaged, with contributions deductible, growth tax-free, and withdrawals penalty-free for qualified medical expenses. For example, a family could redirect $6,600 annually into an FSA while maximizing HSA contributions (up to $8,550 for families in 2025). This shields income from federal, state, and payroll taxes.Estate and Gift Tax Exclusions:

The $13.99 million per individual estate tax exclusion and $19,000 annual gift exclusion create opportunities to transfer wealth without triggering taxes. A married couple could gift $76,000 to each child this year, leveraging the increased thresholds to reduce taxable estates. The highlight how these limits have grown, offering a window to restructure trusts or execute irrevocable gifts.Tax-Loss Harvesting and Capital Gains Management:

Investors with taxable accounts should rebalance portfolios by selling underperforming assets to offset capital gains. For instance, a $10,000 loss on a tech stock could neutralize gains from a real estate ETF, reducing exposure to the 3.8% Net Investment Income Tax (NIIT). With the NIIT thresholds unchanged at $200,000 for singles, high earners must scrutinize holdings to avoid unintended tax hits.

Strategies for Long-Term Wealth Preservation

- Municipal Bonds: Interest from municipal bonds remains exempt from federal income tax and, in some cases, state taxes. For a taxpayer in the 22% federal bracket, a 3% municipal bond yields effectively 3.83%—superior to a 3.5% taxable bond.

- Roth Conversions: Convert traditional IRA assets to a Roth IRA using post-tax dollars, particularly if current income is low relative to future expectations. The $39,500 MAGI limit for the Retirement Savings Contribution Credit (up from $38,000) further incentivizes contributions for lower-income workers.

- Charitable Giving: Use appreciated assets (stocks, real estate) to donate to a charity or donor-advised fund. This avoids capital gains taxes while securing a charitable deduction. For example, donating a stock with a 20% gain generates a tax write-off equal to the asset's fair market value, not the cost basis.

Avoiding Pitfalls

- Farmers and Fishermen: Those deriving over two-thirds of income from these sectors can defer payments until January 15, 2026, but must file their 2025 return by March 2, 2026.

- Disaster Relief: Taxpayers in Arkansas and Tennessee affected by recent disasters have until November 3, 2025, to file or pay taxes.

- Penalties for Underpayment: Missing the June 16 deadline triggers daily compounded interest. Use the IRS Tax Withholding Estimator to adjust Form W-4 withholdings or increase estimated payments via IRS Direct Pay.

Conclusion: Tax Efficiency as a Growth Engine

The June 16 deadline is more than a compliance checkpoint—it's a catalyst for refining tax strategies that compound wealth over decades. By exploiting higher FSA limits, estate planning tools, and tax-advantaged accounts, investors can redirect hundreds or thousands of dollars back into their portfolios. For instance, a couple maximizing their FSA and HSA contributions could reduce taxable income by $11,850 annually, potentially saving over $4,000 in combined federal and state taxes.

The key takeaway? Tax efficiency is a multiplier. Every dollar saved on taxes is a dollar available to compound in investments. With the IRS's rules evolving, now is the time to act—before the clock runs out on June 16.

Data sources: IRS Publications 505, 525; Tax Withholding Estimator tool.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet