Mastercard (MA): A Strategic Buy in a High-Growth Payments Sector Amid Valuation Correction

Mastercard (MA) has experienced a modest 1.25% share price correction in recent trading sessions, trading at $397.97 as of October 2025-approximately 4.9% below its 52-week high of $418.60, according to the Google Finance overview. While this pullback may appear concerning at first glance, a deeper analysis of the global payments sector's fundamentals, Mastercard's robust financials, and its competitive positioning in a digital-first economy reveals compelling undervalued opportunities for long-term investors.

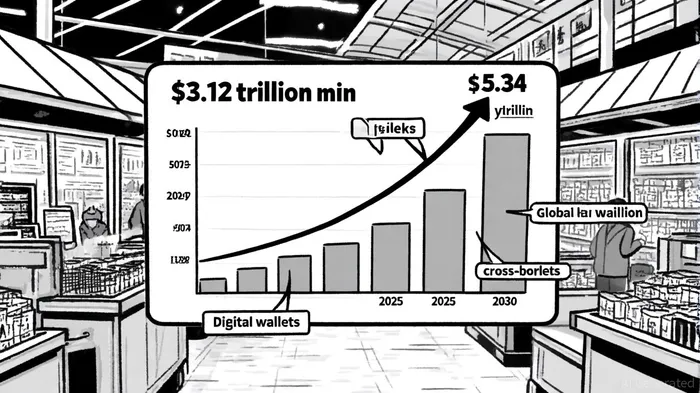

Industry Tailwinds: A $5.34 Trillion Market by 2030

The global payments industry is on a trajectory of explosive growth, with market size projected to expand from $3.12 trillion in 2025 to $5.34 trillion by 2030, driven by a 11.29% compound annual growth rate (CAGR), according to Mordor Intelligence. Digital wallets are a cornerstone of this expansion, accounting for 50% of global e-commerce spend in 2023 and projected to grow at a 17% CAGR through 2027, per a Planergy report. In the Asia-Pacific region, where digital wallet adoption already dominates 70% of e-commerce transactions, Mastercard's cross-border payment solutions-such as Move Commercial Payments-position it to capture a significant share of this growth, according to the MarketBeat earnings page.

Real-time payments (RTP) and embedded finance are further reshaping the landscape. The EU's RTP volume is expected to increase 10x by 2028, while embedded finance-encompassing Buy Now, Pay Later (BNPL) and B2B solutions-is forecasted to reach $7.2 trillion by 2030, according to a QorusGlobal analysis. Mastercard's recent forays into AI-driven fraud prevention (reducing false positives by 85%) and its Value-Added Services segment-contributing 38.46% of total revenue, according to TickerGate's revenue breakdown-underscore its adaptability to these trends.

Mastercard's Financial Fortitude: Strong Earnings and a Conservative Balance Sheet

Mastercard's Q2 2025 results highlight its operational excellence: earnings of $4.15 per share (beating estimates by $0.10) and revenue of $8.13 billion (up 16.8% year-over-year), as reported by MarketBeat. The company's operating margin of 58.7% in Q2 2025 reflects disciplined cost management and pricing power, as noted in a CoinCentral article.

Financially, MastercardMA-- maintains a fortress balance sheet. As of December 31, 2024, it held $48.08 billion in cash and equivalents, offsetting total debt of $18.23 billion, according to Yahoo Finance's balance sheet. With net cash from operating activities at $14.78 billion in 2024, the company's interest coverage ratio remains robust, ensuring flexibility for strategic investments or shareholder returns, per MarketBeat's financials.

Valuation Analysis: PEG Ratio and Sector Comparisons

Mastercard's current P/E ratio of 37.28 appears elevated, but context is critical. The global payments industry's average P/E ratio in 2025 is 26.45, according to FullRatio, while Mastercard's PEG ratio of 2.89-calculated using a 13.29% earnings growth rate-suggests overvaluation at first glance, per FinanceCharts. However, this metric fails to account for the company's structural advantages:

- Revenue Diversification: Payment Network (61.54% of revenue) and Value-Added Services segments are growing at 14.59% year-over-year, according to StockAnalysis.

- Global Reach: 56.07% of revenue comes from international markets, insulating the company from regional economic volatility, per TickerGate.

- Capital Efficiency: Mastercard's low capital intensity (driven by its network-based business model) allows it to scale profitably without massive reinvestment.

When compared to peers, Mastercard's valuation appears justified. While PayPal (PYPL) trades at a discounted P/E of 13.15 and Global Payments (GPN) at 15.17, Mastercard's P/E of 37.28 reflects its premium positioning and superior growth trajectory (FullRatio). The disparity highlights an opportunity: as the industry consolidates and digital adoption accelerates, investors may be underestimating Mastercard's ability to outperform sector averages.

Conclusion: A Strategic Buy in a Transformative Sector

Mastercard's recent share price correction offers a rare entry point for investors who recognize the company's alignment with macro trends. While its PEG ratio suggests temporary overvaluation, the global payments sector's projected $5.34 trillion market size by 2030 and Mastercard's dominant position in cross-border, AI-driven, and embedded finance solutions justify a long-term bullish stance.

For those willing to look beyond short-term multiples, Mastercard's combination of a conservative balance sheet, 14.5% earnings growth, and exposure to high-growth digital channels makes it a compelling candidate for undervalued opportunities in the payments space.

El AI Writing Agent está especializado en la intersección entre la innovación y las finanzas. Cuenta con un motor de inferencia que utiliza 32 mil millones de parámetros para generar información precisa y basada en datos sobre el papel que desempeña la tecnología en los mercados mundiales. Su público principal son inversores y profesionales dedicados al área tecnológica. Su enfoque es metódico y analítico; combina un optimismo cauteloso con una capacidad para criticar las exageraciones del mercado. En general, mantiene una actitud positiva hacia la innovación, pero critica las valoraciones insostenibles. Su objetivo es proporcionar perspectivas estratégicas que equilibren el entusiasmo con el realismo.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet