Market Struggling and Showing Technical Weakness Amid Reopening, but the 'AI Bubble' Presents an Opportunity

The brief celebration following the government’s reopening faded quickly as the market turned lower again, led by tech. Missing essential economic data, uncertainty around the Fed’s December rate decision, and renewed skepticism over an “AI bubble” have become the dominant headwinds, fueling broad technical weakness. While we remain constructive through 2026, investors should be aware of several key technical and fundamental factors that could shape the next buying opportunity.

Charts tell much of the story. The Nasdaq 100’s 3-day moving average failed to break above the 7-day on Wednesday, halting a potential bullish reversal and pushing the index back into a downward trend. It remains unclear whether the index will retest its previous support level. If it breaks below that key level, a “lower-high, lower-low’’ bearish pattern may form, signaling the need for greater caution.

The RSI has slipped to 35, which is low relative to the past six months, though far from the extreme April reading of 14. The Nasdaq 100 also logged a seven-month rally prior to November and remains above October’s highs. The recent pullback is not alarming yet, which is why there is no urgency to buy the dip.

On fundamentals, although the government is reopening, the White House said Wednesday that October CPI and nonfarm payrolls may never be released, with priority shifting to November’s reports. The absence of these key figures leaves investors without a clear macro picture. It will take time for government operations to normalize, and markets need time to digest the resulting uncertainty. This is more short-term noise than structural risk.

The missing data also complicates the Fed’s December meeting. Chair Powell previously emphasized that there is no urgency to cut rates, citing still-elevated inflation. Yet a December cut may not matter as much as investors assume. A 25-basis-point move is often treated as a symbolic gesture rather than a meaningful economic catalyst. With Powell’s term nearing its end, more easing is expected in 2026 as Trump’s policy outlook carries greater influence. Even if the Fed holds steady in December, it would be a delay rather than a shift away from further easing.

The shutdown fallout and the December meeting are short-lived obstacles. The bigger concern for markets is the fear of an AI bubble. Former AI leaders, including NvidiaNVDA--, AMDAMD--, and BroadcomAVGO--, have all stumbled recently on valuation concerns and 'bubble' outlooks. While Amazon, Microsoft, Google, and Meta continue to commit massive AI spending, the slow pace of monetization has yet to justify elevated valuations. Meta’s disappointing results dragged the stock back to its May level as investors questioned the company’s ability to sustain such heavy investment. If monetization fails to accelerate, these companies may be forced to slow spending, pressuring the entire AI ecosystem.

Kioxia’s earnings added to the pressure, with guidance coming in well below expectations. However, Kioxia remains heavily tied to Apple’s supply chain, while Micron and Samsung are shifting toward AI-focused memory. Not every chipmaker will be a winner in this next phase of AI demand. As the trend enters a second stage, fewer players will dominate, and the winners will take an outsized share.

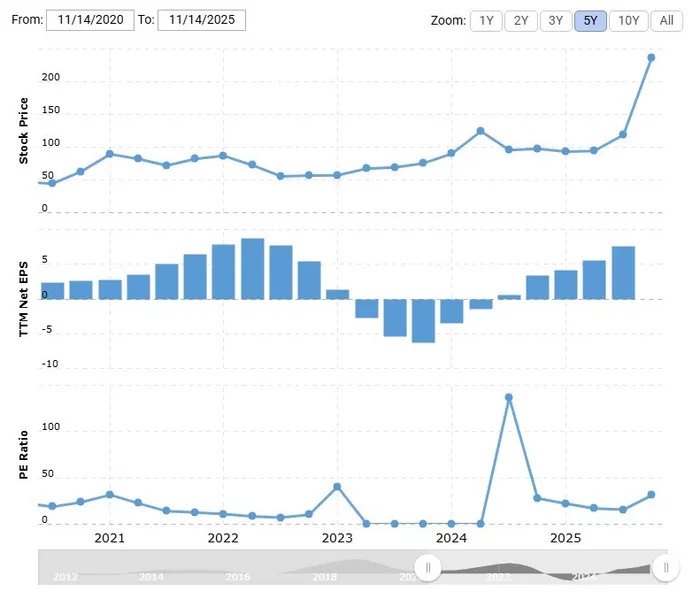

The AI narrative remains intact. Early monetization is real, and more industries are beginning to integrate AI technology, reinforcing the long-term story. It is far too early to call this a bubble. Even after a 182% rally this year, Micron trades at only 31 times earnings, hardly excessive. A genuine bubble forms when investors unanimously dismiss valuation risk. With skepticism still widespread, this is not peak euphoria.

(MU's Valuation Multiple)

Year-end positioning may also be contributing to the sell-off. After a year of exceptional gains for AI names, the lack of a blockbuster catalyst leaves funds inclined to lock in profits. Doubts over fundamentals and liquidity reinforce that caution.

Altogether, the technical landscape suggests the correction may continue, yet investors should not overreact to these headwinds. Government operations will return to normal, the AI-driven economic boom remains intact, and a delayed Fed cut does not alter the longer-term trajectory. While AI-bubble fears are the main source of anxiety, select players will continue to outperform with the macro trend at their back. This stage of the cycle is about alpha selection, not blanket exposure to every AI-related stock.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO