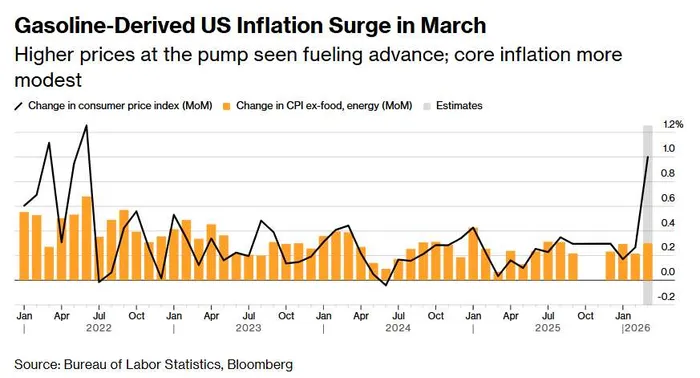

March CPI Preview: Spike to 3.3%, Cuts Delayed?

The recent surge in oil prices—driven by escalating tensions in the Middle East—has sharply altered the inflation outlook, placing the upcoming U.S. CPI release at the center of market attention. What was once a steady disinflation trend is now facing a meaningful disruption, and the March CPI print may offer the first clear signal of how deeply energy shocks are transmitting into the broader economy.

If inflation reaccelerates beyond expectations, it would not only delay the Federal Reserve’s rate-cut timeline, but could also reopen discussions around further tightening—a scenario markets have largely priced out.

A Sharp Rebound in Headline Inflation

Consensus expectations point to a notable jump in March CPI, with headline inflation projected to rise to 3.3% year-on-year, marking the highest level in nearly two years. Core CPI, which excludes food and energy, is expected to come in at 2.7%, suggesting that while underlying inflation remains relatively contained, pressure is beginning to build.

At a high level, this divergence reinforces a key dynamic:

headline inflation is being pulled higher by external shocks, while core inflation remains the battleground for policy decisions

Energy: The Primary Transmission Channel

Energy prices are set to be the dominant driver of the March inflation print. U.S. gasoline prices have already surpassed $4 per gallon, rising nearly 20%, and are expected to contribute roughly 0.6 percentage points to CPI alone.

This is not a contained shock. Rising fuel costs are cascading across the economy:

Higher jet fuel prices are feeding into airfare inflation

Transportation costs are increasing across supply chains

Logistics expenses are being passed through to end consumers

Compounding the issue, disruptions in critical supply routes such as the Strait of Hormuz introduce an additional layer of uncertainty, raising the risk of prolonged energy-driven inflation.

Food and Goods: Second-Round Effects Emerging

Beyond direct energy costs, second-order effects are beginning to surface.

Food prices are expected to rise approximately 2.5% year-on-year, as higher oil prices push up transportation and fertilizer costs. This represents a classic cost-push dynamic, where upstream price shocks gradually filter into consumer baskets.

In goods inflation, the impact is likely to be more moderate but still positive. The combination of higher input costs and ongoing tariff transmission is expected to exert incremental upward pressure on prices. While not explosive, this reinforces the broader narrative that inflation is becoming more persistent across categories.

Services Inflation: A Mixed but Critical Signal

Services remain the most important component for Federal Reserve policy—and here, the picture is more nuanced.

Housing inflation appears to be stabilizing. With restrictive interest rates still in place, slowing population growth, and structural shifts such as reduced office demand due to AI adoption, the housing market is tilting toward ownership rather than rental pressure. Owners’ equivalent rent is expected to rise modestly by 0.2% month-on-month, indicating a gradual cooling trend.

Healthcare inflation may also ease, following the resolution of labor disruptions and continued job growth in the sector.

However, not all services are softening. Restaurant prices—already up 3.9% over the past year—are likely to continue climbing, supported by rising food costs, wage pressures, and tighter labor supply due to reduced immigration. This highlights a key asymmetry:

while some service components are cooling, others remain structurally sticky

Wall Street Is Divided on the Path Forward

Investment banks broadly agree that energy will drive a sharp rebound in headline CPI. However, views diverge meaningfully when it comes to underlying inflation dynamics.

Some expect used car prices to stabilize or rebound, adding to core inflation

Others see continued weakness in auto pricing, limiting upside

On housing, opinions split between gradual cooling and potential reacceleration in rents

More importantly, there is no consensus on whether the current oil shock is transitory or persistent.

Some institutions warn of a dual inflation driver—energy plus goods—potentially pushing inflation toward 4%

Others argue that high energy costs will erode consumer purchasing power, limiting companies’ ability to pass through price increases

This divergence reflects a deeper uncertainty:

whether the current shock represents a temporary spike—or the beginning of a new inflation regime

The Bigger Risk: Inflation Staying Higher for Longer

Several analysts caution that even if oil prices eventually decline, the inflationary impact may linger.

Physical damage to Middle Eastern energy infrastructure could delay supply normalization, embedding a geopolitical risk premium into oil prices for an extended period. Estimates suggest it could take at least six months for inflation to fall back below 3%.

At the same time, tariffs continue to work their way through the system, contributing an estimated 0.5%–0.6% to inflation. This layered effect—energy plus policy—raises the risk that inflation will remain elevated even as individual components begin to normalize.

Notably, while energy has not yet significantly impacted core CPI, leading indicators such as airfares and transportation costs should be closely monitored. These categories often act as early signals of broader inflation transmission.

Conclusion: CPI as a Policy Pivot Point

The upcoming CPI release is more than just another data point—it is a critical inflection test for both markets and policymakers.

A stronger-than-expected print could delay rate cuts and revive tightening fears

A contained reading may reinforce the view that the shock is manageable

But the real question extends beyond March:

is this the beginning of a renewed inflation cycle, or simply a temporary disruption?

For now, the market is left navigating a familiar but uncomfortable reality— inflation is no longer falling in a straight line, and policy certainty is once again fading.

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet