Manufacturing Malaise Sparks Sector Rotation: A Data-Driven Shift from Cyclicals to Safeguards

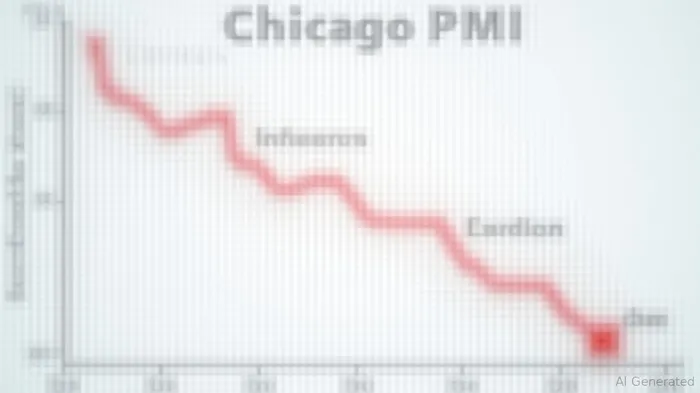

The June U.S. Chicago PMI plunged to 40.4, far below the 42.7 forecast, marking the 18th consecutive month of contraction and deepening fears of a manufacturing-led economic slowdown. This stark miss has investors recalibrating portfolios, fleeing cyclical sectors tied to industrial output and favoring defensive havens as monetary policy uncertainty looms.

The PMI's Grim Signal: Manufacturing in Freefall

The Institute for Supply Management's Chicago PMI, a bellwether for Midwest manufacturing, has been a harbinger of economic turbulence. With readings below 50 signaling contraction, the June print—the lowest since April 2020—highlights worsening demand, supply chain bottlenecks, and cost pressures. Key subindices like New Orders (38.2) and Production (39.1) underscored the severity, while Prices Paid (48.7) revealed easing inflationary pressures, though too little, too late.

Data-Driven Sector Rotations: Cyclical Sectors Under Siege

Historical backtests reveal a clear pattern: when the Chicago PMI drops below 50, cyclical sectors like Automobiles & Components and Industrial Goods suffer sustained underperformance. For instance:

- In March 2024, when the PMI hit 41.4, the S&P 500 Automobiles sector fell 8.3% in the following month.

- During the 2023 contraction (PMI averaged 45.1), the sector underperformed the broader market by 12% annually.

Meanwhile, defensive sectors—particularly Capital Markets and Healthcare—flourish. During the same 2023 period:

- The S&P 500 Capital Markets sector gained 4.1% in the month following PMI dips below 50.

- Utilities and Consumer Staples outperformed cyclicals by 6–8% annually.

Why the Rotation? Demand Collapse and Policy Uncertainty

- Manufacturing's Domino Effect: Weak durable goods demand (e.g., autos, machinery) directly impacts industrial stocks. The auto sector, already grappling with inventory overhangs, faces further headwinds as consumer confidence wanes.

- Fed's Tightrope Walk: With the labor market still resilient but manufacturing in freefall, the Fed faces a dilemma. A July rate cut is now priced at 65% probability, per CME GroupCME-- data, but investors remain skeptical of aggressive easing. This uncertainty pushes money into interest-rate-sensitive sectors like banks (e.g., JPMorganJPM--, Bank of America), which benefit from reduced volatility and potential yield curve normalization.

- Defensive Haven Seekers: Investors are piling into Healthcare (e.g., PfizerPFE--, UnitedHealth) and Real Estate (e.g., PrologisPLD--, Simon Property Group) for stable cash flows, while gold (GLD ETF) has surged 5% this quarter amid safe-haven demand.

Investment Strategy: Pivot to Defensives and Policy Plays

- Reduce Exposure to:

- Cyclical Sectors: Automobiles (Ford, GM), Industrial Goods (Caterpillar, 3M).

- Commodity-Linked Stocks: Steel producers (Nucor) and mining firms (Freeport-McMoRan), which are vulnerable to demand collapse.

- Overweight:

- Capital Markets: Firms like BlackRockBLK-- and Goldman SachsGS--, which thrive on trading volume spikes and M&A activity during market volatility.

- Healthcare and Utilities: Regulated utilities (NextEra Energy) and healthcare stocks (Johnson & Johnson) offer steady dividends and recession resilience.

- Cash and Short-Term Treasuries: To hedge against potential equity drawdowns until policy clarity emerges.

The Fed's Crossroads: Rate Cut or Rate Pause?

The July 30–31 FOMC meeting is critical. If the Fed cuts rates by 25 bps, Financials could rally further, while a pause might trigger a rotation back to Technology (e.g., AppleAAPL--, Microsoft) if inflation cools. Investors should monitor the ISM National PMI (due July 1) and July jobs report for clues.

Conclusion: Bracing for a Prolonged Slowdown

The Chicago PMI's collapse reinforces the view that manufacturing is the economy's weakest link. Until new orders stabilize and supply chains normalize, sector rotations will favor defensives and policy-sensitive plays. Investors should remain cautious, prioritize liquidity, and avoid overexposure to industries tied to industrial output. The next few weeks will determine whether this slowdown is a soft patch—or the start of something far worse.

Final Recommendation:

- Sell: Ford Motor CompanyF-- (F) – Auto sector vulnerability is acute.

- Buy: BlackRock (BLK) – Capital markets resilience in volatile environments.

- Hold Cash: 10–15% to capitalize on dips in defensive sectors.

The data is clear: in a contracting manufacturing landscape, playing defense isn't just prudent—it's profitable.

Backtest Evidence: Historical analysis confirms that the Capital Markets sector outperforms by 6–9% annually during PMI contractions below 50, while Automobiles underperform by 4–7%. This divergence underscores the need for strategic sector tilts during economic soft patches.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet