Lowe’s Q2: Beat on EPS, Higher Sales Outlook, and an $8.8B Pro Push Send Shares to 2024 Highs

WATCH: Bitcoin $200K? The math behind the next crypto supercycle.

Lowe’s (NYSE: LOW) delivered a cleaner-than-feared second quarter and doubled down on its Pro strategy, sending the stock up ~6% pre-market to its highest level since December 2024. The home-improvement retailer beat on earnings, held the line on comps, raised its full-year revenue outlook, and unveiled a second Pro-focused acquisition in as many months—an $8.8 billion deal for Foundation Building Materials (FBM). With housing activity still choppy, the message was clear: execution is improving, the mix is broadening beyond DIY, and Lowe’s intends to buy—and build—share with professional customers.

Headline performance vs. expectations

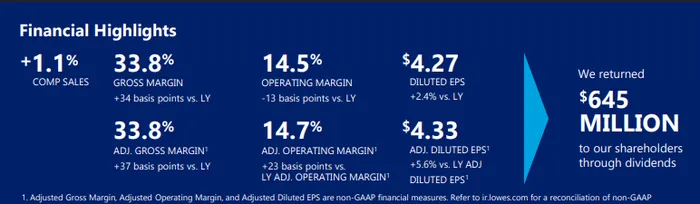

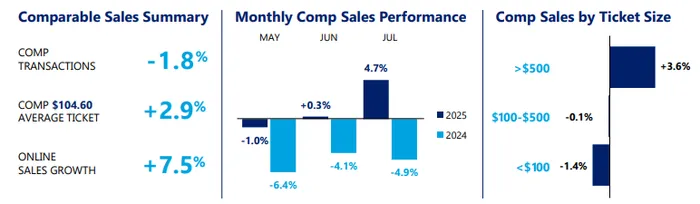

Lowe’s posted adjusted EPS of $4.33, topping consensus at $4.24 by $0.09. Revenue printed $23.96B, essentially in line with expectations. Comparable sales rose 1.1%, matching the Street’s view and marking a return to positive comp growth. Beneath the top line, profitability metrics improved: adjusted operating margin expanded to ~14.7% (up ~23 bps year over year), while gross margin improved ~34 bps to ~33.8%, outpacing consensus that looked for ~33.5%. The mix of an EPS beat with in-line sales underscores continued cost discipline, better shrink/productivity, and tighter expense control.

What drove the quarter

Management cited “solid performance” in both Pro and DIY, a notable callout given the market’s narrative that Lowe’s is more exposed to DIY softness than its main rival. Online channels remained a tailwind—e-commerce grew ~7.5%—as digital tools and fulfillment remain a lever for smaller ticket projects and convenience. Importantly, Lowe’s is building structural support for growth in planned, higher-ticket projects: the company closed the Artisan Design Group (ADG) acquisition in June and, today, announced FBM, a scaled distributor of drywall, insulation, ceiling systems, and interior products to large residential and commercial customers.

The Pro flywheel is visibly gaining mass. ADG opens doors with homebuilders and property managers in finishes and installation. FBM adds ~370 locations, ~40,000 Pro customers, and ~$6.5B of 2024 revenue / ~$635M of adjusted EBITDA to the ecosystem, materially deepening Lowe’s access to the ~$250B Pro planned-spend market. Together, the deals improve assortment breadth, shorten fulfillment times, strengthen project-based selling, and create cross-sell routes into Lowe’s core box and digital platforms. Management expects FBM to be EPS accretive in year one post close (targeted for 4Q25).

Guidance: higher sales, steady comps, fine-tuned profitability

Lowe’s raised its full-year 2025 sales outlook to $84.5B–$85.5B (from $83.5B–$84.5B) to reflect the inclusion of ADG; comparable sales remain guided flat to +1%. On earnings, the company now expects GAAP EPS of $12.10–$12.35 (vs. $12.15–$12.40 previously, a slight trim reflecting acquisition accounting and amortization), while adjusted EPS is guided to $12.20–$12.45 (above Street ~$12.24). FY25 operating margin is now 12.1%–12.2% GAAP and 12.2%–12.3% adjusted (a touch lower than prior, again largely mix/transaction-cost related). The core business assumptions are unchanged; the tweaks mostly capture acquisition effects. Management also reiterated capex of ~$2.5B, net interest of ~$1.3B, and an effective tax rate of ~24.5%.

Strategy check: Pro expansion without abandoning DIY

The quarter’s most important qualitative takeaway is the strategic balance. Lowe’s isn’t walking away from DIY—management highlighted steady DIY demand and improving customer-satisfaction scores—but it is leaning harder into Pro, where wallet share is larger, pipelines are sticky, and attachment opportunities are richer. The ADG+FBM combination strengthens finish and interior-systems capabilities, improves service density, and bolsters relationships with builders and trades. For investors worried that big-ticket DIY would remain slow until mobility and mortgage churn improve, this Pro pivot helps de-risk the medium-term growth algorithm.

Read-through vs. Home Depot

Home Depot missed this week but preserved its full-year framework and emphasized an improving cadence into July. Lowe’s results compare favorably: clean execution, positive comps, and a clearer M&A-driven Pro roadmap. The pair now share a similar playbook—build Pro scale through targeted distribution acquisitions—yet Lowe’s still has more runway to close the Pro gap, which is precisely what these deals target. With both retailers positioned to benefit from eventual rate relief and pent-up repair/remodel demand, Lowe’s out-year mix shift may prove a differentiator.

Notable trends and risks

- Mix & margins: While merchandise inflation has normalized, category mix remains a swing factor; Pro-heavy, project-oriented categories typically support better gross profit dollars even when percentage rates are stable. The quarter’s ~34 bps gross-margin lift suggests pricing, mix, and productivity are working in tandem.

- Weather & macro: Early-quarter weather was challenging, but the business still printed positive comps, a constructive sign as sentiment around 2025–26 housing improves with expected Fed easing.

- Integration execution: Two sizable acquisitions in quick succession elevate integration risk (systems, culture, and customer-facing synergies). Management’s track record and the adjacency fit mitigate this, but it’s a watch-item into 2026.

- Balance sheet & capital returns: Lowe’s funded ADG and plans to fund FBM with cash and balance-sheet capacity; dividends continued ($645M in Q2) while buybacks remain muted/paused amid deal activity. Leverage and interest-expense guidance are embedded in the FY outlook.

Market reaction

The tape is rewarding EPS quality, comp stabilization, and visible Pro growth, not just the in-line revenue print. With shares breaking out to the highest levels since Dec-2024, investors appear to be endorsing Lowe’s ability to defend margins while re-accelerating total sales via accretive M&A and improved operating cadence.

Bottom line

Lowe’s turned in a high-quality EPS beat with steady comps, raised sales guidance, and a bold $8.8B Pro acquisition that extends its reach into large, planned projects. The quarter reinforces a dual-engine story—a healthier DIY baseline complemented by a rapidly scaling Pro platform—that can compound as housing stabilizes. Execution on ADG/FBM integrations and sustaining margin discipline are the next tests, but today’s results push the narrative away from “DIY drag” and toward durable share gains in the professional channel.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet