The Longevity Dividend: Investing in Aging Populations for Sustainable Growth

The global demographic landscape is undergoing a seismic shift. By 2025, the population aged 65 and older will surpass 1.15 billion, a number projected to double by 2050. This aging wave, driven by rising life expectancy (73.3 years in 2024, expected to reach 77.4 by 2054), is reshaping financial systems, healthcare infrastructure, and retirement planning. While the challenges of longevity risk—outliving savings—are stark, this demographic transition also unlocks a $15 trillion market opportunity. Investors who align with the "longevity dividend" can secure sustainable growth while addressing systemic risks to retirement resilience.

The Dual Edges of Longevity Risk

The underestimation of longevity risk is a critical vulnerability. A 2025 TIAA Institute study reveals that 40% of millennials expect to live to 90 or beyond, yet only 25% of U.S. retirees over 70 utilize default annuities to convert savings into guaranteed income. Compounding this, 68% of Americans aged 55–64 lack confidence in managing retirement expenses, and 46% of global investors lack a robust long-term plan. Extending retirement by five years increases financial shortfall risks by 41%, while rising healthcare costs—driven by chronic disease management and caregiving demands—threaten to erode savings.

However, these challenges are not insurmountable. The aging population is also a catalyst for innovation in healthspan technologies, AI-driven financial tools, and longevity-linked assets. These solutions are not merely mitigants but engines of growth, offering both financial resilience and market returns.

Healthspan Technologies: Investing in the Science of Aging

The quest to extend "healthspan"—the period of life spent in good health—is attracting record capital. In 2025, over $2 billion has been invested in geroscience companies like ResTOR Bio and Superpower, which target biological aging and cognitive decline. The cognitive decline treatment market alone is projected to reach $200 billion by 2030, driven by demand for therapies addressing Alzheimer's and age-related diseases.

Investors should consider exposure to biotech firms pioneering senolytics (drugs that clear senescent cells) and neuroprotective therapies. For example, Unity Biotechnology (NASDAQ: UBX) and Alkahest are advancing clinical trials for age-related conditions. Additionally, ETFs like the Global X Longevity Thematic ETF (LNGR) provide diversified access to this sector.

Default Annuities: The Guaranteed Income Solution

Annuities remain a cornerstone of longevity risk mitigation. Single-premium immediate annuities (SPIAs) convert lump sums into lifelong income streams, ensuring retirees cannot outlive their savings. Despite their efficacy, only 25% of U.S. retirees over 70 currently use annuities, leaving a $25 trillion mortality coverage shortfall.

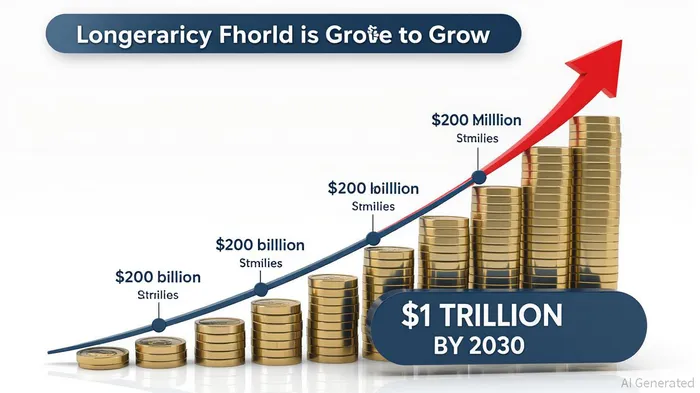

The rise of longevity bonds—financial instruments tied to life expectancy trends—offers another avenue. By 2030, this market is projected to grow from $200 billion to $1 trillion. These bonds hedge against demographic uncertainties by aligning payouts with mortality rates, making them ideal for pension funds and institutional investors.

AI-Driven Retirement Platforms: Cognitive Prosthetics for Aging Populations

Artificial intelligence is revolutionizing retirement planning by addressing cognitive decline and financial literacy gaps. Platforms like Betterment and Personal Capital integrate predictive analytics, behavioral nudges, and real-time fraud detection to empower aging users. For instance, Betterment's predictive budgeting algorithms have reduced late-stage portfolio adjustments by 20%, while Personal Capital's AI tools increased portfolio diversification by 15% among users over 65.

In China, digital wealth management platforms like Zheshang E-Finance have boosted self-funded retirement planning by 15–20% in low-literacy households, demonstrating the scalability of AI-driven solutions. These tools are not just financial instruments but "cognitive prosthetics," compensating for diminished decision-making capacity in older adults.

Policy and Market Synergies: A Global Perspective

Governments are increasingly recognizing the need to adapt retirement systems. Japan's 2024 mandatory annuity education policy led to a 15% adoption increase, while Singapore's focus on youth financial literacy (78% proficiency in 2025) ensures intergenerational resilience. These policies amplify the effectiveness of private-sector solutions, creating a virtuous cycle of innovation and adoption.

Emerging markets, though lagging in aging trends, will face demographic shocks by 2100, with population declines of 20–50% in some economies. Proactive investment in longevity-linked assets now can position investors to capitalize on these shifts.

Strategic Allocation: Building a Resilient Portfolio

To harness the longevity dividend, investors should diversify across three pillars:

1. Healthspan Technologies: 20–30% in biotech ETFs and clinical-stage firms.

2. Longevity-Linked Assets: 30–40% in annuities, longevity bonds, and senior housing REITs (e.g., Welltower).

3. AI-Driven Fintech: 15–20% in platforms like Betterment or Wealthfront.

Conclusion: The Longevity Era Is Here

The aging population is not a distant crisis but an immediate reality. By 2054, even rapidly growing regions will face systemic changes in healthcare and retirement systems. Investors who act now—by allocating to longevity-linked assets, AI-driven tools, and healthspan innovations—can secure both financial resilience and market returns. The longevity dividend is not just about managing risk; it is about building a future where extended lifespans are met with prosperity, not precarity.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet