The Long-Term Impact of Prolonged High Interest Rates on Global Equity Markets and Emerging Market Debt

The global financial landscape in 2025 is defined by a delicate balancing act: central banks grapple with the dual mandate of curbing inflation while mitigating the long-term scars of prolonged high interest rates. As the Federal Reserve, European Central Bank, and other major institutions navigate a gradual easing cycle, investors must assess how years of elevated rates have reshaped equity valuations and emerging market (EM) debt dynamics. The interplay between monetary policy, capital flows, and sectoral vulnerabilities offers critical insights for portfolio construction in an era of shifting macroeconomic fundamentals.

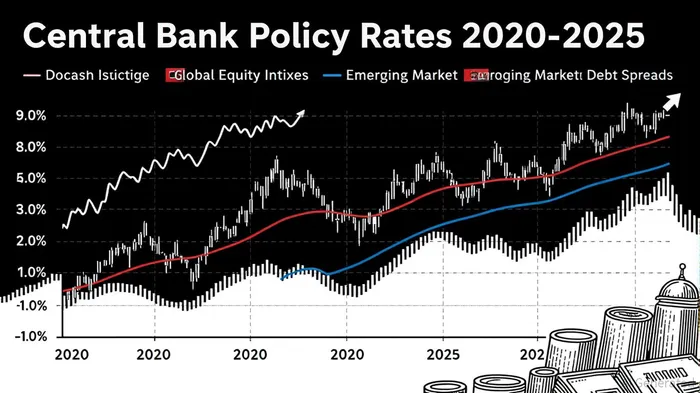

Central Bank Policy: A Tale of Divergence

Central banks have maintained elevated rates for over three years, a stark departure from the rapid easing cycles of 2008 and 2020. The U.S. Federal Reserve, for instance, , with a 25-basis-point cut in December 2024 marking the first step toward normalization. Similarly, the European Central Bank and Bank of England have followed suit, , respectively. In contrast, .

This prolonged high-rate environment has created a fragmented global monetary landscape. While advanced economies ease, EM central banks have responded to disinflationary pressures with rate cuts, creating a favorable yield differential. The Reserve Bank of Australia, for example, , while the Bank of Canada and Reserve Bank of New Zealand followed similar paths. This divergence has weakened the U.S. dollar, a critical tailwind for EM debt and local currency equities.

Equity Valuations: Resilience Amid Structural Shifts

Global equity markets have demonstrated remarkable resilience despite the high-rate backdrop. The S&P 500 and NASDAQ, for instance, rebounded from a brief bear market in Q2 2025 to reach record highs, driven by strong corporate earnings and fiscal stimulus. However, the structural impact of prolonged high rates is evident in sectoral rotations. Growth stocks—particularly speculative tech firms—have outperformed value and small-cap equities, as investors prioritize long-term innovation over short-term cash flows.

The "" tech stocks, , exemplify this trend. Their dominance underscores a shift in capital allocation toward sectors with scalable, AI-driven business models. Conversely, sectors reliant on short-term liquidity, such as commercial real estate and energy, face heightened refinancing risks. The "maturity wall" of corporate debt maturing at higher rates has forced firms to either deleverage or absorb elevated borrowing costs, compressing margins in capital-intensive industries.

Emerging Market Debt: A Fragile Equilibrium

Emerging market debt has navigated the high-rate environment with a mix of caution and opportunity. The weakening U.S. dollar, driven by fiscal uncertainty in the U.S. and accommodative EM monetary policies, has bolstered local currency bonds. The JP Morgan GBI-EM Global Diversified Index saw all 17 of its 19 currencies appreciate against the dollar in Q2 2025, a rare feat in a high-rate world. Sovereign and corporate spreads also tightened, reflecting improved risk appetite and the relative value of EM yields.

However, this stability is contingent on several factors. First, EM central banks must continue to balance inflation control with growth support. Brazil's decision to raise rates in 2025, for example, highlights the tension between fiscal discipline and economic recovery. Second, nonbank financial institutions—now accounting for nearly 50% of global syndicated loans—pose systemic risks if defaults rise. These entities, often underregulated and reliant on unstable funding, amplify contagion risks in a downturn.

Third, insolvency frameworks in EMs remain underdeveloped, prolonging corporate distress and delaying capital reallocation. The IMF's 2025 paper on corporate sector vulnerabilities underscores that firms in jurisdictions with weak insolvency regimes are more sensitive to monetary tightening, exacerbating defaults and crowding out healthier businesses.

Sectoral Vulnerabilities: Beyond the Property Sector

The risks of prolonged high rates extend beyond EM property markets. The corporate sector, particularly in non-tradable industries, faces a perfect storm of elevated debt servicing costs and weak demand. —those with debt servicing costs exceeding EBITDA—have proliferated in sectors like manufacturing and retail, where margins are thin and liquidity is scarce.

Nonbank credit intermediation further complicates the picture. In advanced economies, , often extending credit to weaker firms. This migration of risk to less-regulated entities increases the likelihood of a corporate default cycle, with spillovers to banks and broader financial systems. EMs, with less resilient banking sectors, are particularly vulnerable.

Investment Implications and Strategic Recommendations

For investors, the key lies in navigating the divergent impacts of prolonged high rates. In equities, sectoral tilts toward high-growth, AI-driven industries—while avoiding interest-rate-sensitive sectors like real estate and utilities—can mitigate downside risks. Defensive positions in healthcare and consumer staples may also offer stability.

In EM debt, a selective approach is critical. Prioritize countries with strong fiscal discipline, manageable external debt, and improving insolvency frameworks. Local currency bonds in Brazil, India, and Indonesia, for instance, offer attractive yields amid currency strength. Hard currency debt should focus on sovereigns with low debt-service-to-revenue ratios and political stability.

Finally, hedging against currency and interest rate volatility is essential. EM investors should consider dollar-cost averaging and diversifying across regional markets to reduce concentration risks. For equities, sector rotation and active management of duration exposure can enhance risk-adjusted returns in a high-rate environment.

Conclusion

The prolonged high-interest-rate era has left an indelible mark on global markets. While equity valuations have adapted through sectoral shifts and innovation-driven growth, EM debt remains a double-edged sword—offering yield but requiring careful risk management. As central banks edge toward normalization, investors must remain vigilant to the lingering scars of high rates and the evolving interplay between policy, capital flows, and sectoral vulnerabilities. The path forward demands a nuanced, data-driven approach to balance growth opportunities with structural risks.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet