Lithium’s Comeback: How Supply Strains Are Powering ETF Opportunities in EVs

After a punishing glut that drove prices into a downtrend through 2024, the lithium market is seeing a jolt of renewed interest in 2025. The catalyst: supply disruptions and tightening inventories have reminded investors of lithium’s critical role in the global clean energy transition, especially amid the persistent growth projections for electric vehicles (EVs). Battery manufacturers and automakers are escalating investments in upstream supply, while Western governments seek to secure domestic sources to avoid future shortage shocks—a shift echoed in the original ETF Trends analysis, which highlighted how macro pressures and supply chain vulnerabilities can spur a turnaround for beaten-down commodities like lithium.

Why Lithium Is Back in Focus

Two things can be true at once: prices cratered and risks are rising.

Prices collapsed ~90% from 2022 peaks, crushing miner profits (SQM’s Q2 net slid ~59%). Yet any incremental supply hit now lands on a fragile base.

A real disruption arrived in August: CATL halted its Yichun mine in China (≈3% of 2025 global supply) as a license expired—spiking Chinese lithium futures and lifting producer shares. Even cautious analysts say the halt trims the expected surplus and raises upside risks to prices.

Big picture: EV and storage demand keeps growing, but 2024–25 brought oversupply that pushed prices to multi-year lows; producers have responded with capex cuts, plant mothballing, and layoffs. That creates optionality if demand accelerates or more supply goes offline.

Source: tradingeconomics.com

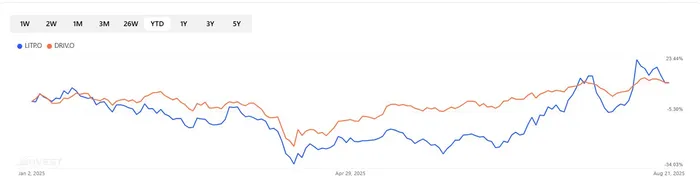

Key ETFs: LITPLITP--, DRIVDRIV-- – Macro Exposure to Lithium & EV Themes

Sprott Lithium Miners ETF (LITP)

Focus: Pure-play exposure to lithium miners globally, tracking the Nasdaq Sprott Lithium Miners Index —i.e., highest beta to lithium spot.

AUM / Fee: $19.7M AUM, 0.65% expense ratio.

Commentary: If disruptions persist or demand firms, miners are the most levered rebound play—but still carry funding and project-delay risk if prices stay low.

Global X Autonomous & Electric Vehicles ETF (DRIV)

Focus: Broad EV/autonomy value-chain—automakers, chips, software, and some battery materials. Less direct lithium exposure than miners.

AUM / Fee: $331.1M AUM, 0.68% expense ratio.

Commentary: DRIV offers diversified exposure to the EV supply chain, including automakers, battery technology, and sensor manufacturers. Growth in regulatory support and consumer adoption drives a favorable outlook, but competition and tech risk should be monitored as the sector matures.

Outlook: Lithium & EV ETFs Face Macro Crosswinds

Supply-Driven Rally: Supply chain shocks (from mine suspensions in China to slower ramp-ups in new projects) have turned lithium from oversupplied to a critical commodity overnight, fueling ETF rebounds.

EV Demand: Battery and automaker investments point to multi-year demand ramp, with global lithium consumption projected to multiply by 13x by 2050.

Risks: Commodity and tech ETFs remain threatened by geopolitical, regulatory, and supply chain risks—factors that can drive volatility but also create buying opportunities for tactical investors.

Summary

Lithium’s rebound underscores how macro events can transform market sentiment—and ETF opportunities—almost overnight. For retail investors, tracking both direct miner ETFs (like LITP) and broader EV technology fund (DRIV) offers complementary approaches. As supply disruption risks linger and EV adoption surges globally, strategic exposure via these ETFs can be an effective way to leverage the energy transition while managing risk.

Compare the Lithium plays LITP, DRIV with our ETF Compare Tool

Market Radar delivers concise, daily trading ideas by tracking everything from options activity and market sentiment to high-profile political trades.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet