LifeMD's Preferred Dividend Signal and Investment Attractiveness: A Deep Dive into Dividend Reliability and Capital Preservation

When evaluating preferred stocks in a rising interest rate environment, investors must balance the allure of high yields with the risks of price volatility and dividend sustainability. . , it offers a tempting income stream, but its investment attractiveness hinges on critical factors like credit risk, interest rate sensitivity, and the company's financial health.

Dividend Reliability: A Double-Edged Sword

, . , with consistent quarterly payments[1]. 's recent “Overweight” rating and $15.00 price target underscore confidence in LifeMD's growth trajectory, particularly in women's and behavioral health[2]. However, , signaling potential fragility[3]. While the company has avoided dividend cuts, its reliance on a fixed payout in a rising rate environment could strain cash flow if telehealth demand or margins falter.

Capital Preservation: Navigating Interest Rate Headwinds

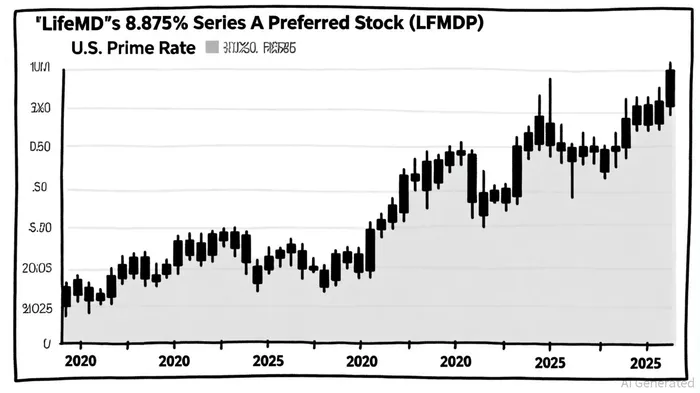

Preferred stocks like LFMDPLFMDP-- are inherently sensitive to interest rate changes. As the U.S. , , . This discount reflects market skepticism about its yield relative to newer, higher-rate instruments. . If rates continue rising, LFMDP's price could face further downward pressure, eroding capital gains potential.

Credit Risk: A Missing Puzzle Piece

LifeMD's absence of a publicly disclosed credit rating from S&P, Moody's, or Fitch in 2025 introduces uncertainty. , the lack of third-party validation leaves investors in the dark about its ability to weather economic downturns. For context, Weatherford International's recent upgrades from all three agencies followed demonstrable improvements in liquidity and margins[7]. Without similar clarity for LifeMDLFMD--, .

The Bottom Line: A High-Yield Gamble?

, especially for income-focused investors. However, its investment case is a tightrope walk. The fixed dividend offers stability, but rising rates could depress its price, and the absence of a credit rating complicates risk assessment. Cantor Fitzgerald's optimism is justified by LifeMD's growth in high-margin telehealth segments, but prudence dictates hedging exposure. For those willing to tolerate volatility, LFMDP could serve as a speculative complement to a diversified portfolio—provided they monitor macroeconomic signals and the company's financial updates closely.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet