Laser Photonics: A Strategic Catalyst for Long-Term Growth in Industrial Laser Marking

Laser Photonics (NASDAQ: LASE) has emerged as a compelling case study in strategic reinvention, leveraging mergers and acquisitions (M&A) to position itself at the forefront of the industrial laser marking sector. The company's recent multi-system order win from a top-five global semiconductor capital equipment company—secured through its Beamer Laser Marking Systems subsidiary—represents not just a commercial milestone but a validation of its long-term growth strategy[1]. This win, coupled with robust market tailwinds in semiconductors and industrial automation, underscores Laser Photonics' potential to redefine its market leadership and deliver outsized returns for investors.

Strategic Entry into the Semiconductor Sector: A $1 Trillion Opportunity

The semiconductor industry, a cornerstone of modern technology, is projected to surpass $1 trillion in value by 2030[2]. Laser Photonics' entry into this sector via Beamer's advanced laser marking systems aligns with the global push for domestic semiconductor production, driven by initiatives like the U.S. CHIPS and Science Act[3]. The recent order from a top-tier semiconductor capital equipment provider validates the company's ability to meet the sector's stringent technical and quality demands. By integrating Beamer's technology, Laser PhotonicsLASE-- has not only secured a foothold in this high-growth market but also unlocked cross-selling opportunities across its broader portfolio, including Control Micro Systems (CMS) and CleanTech laser cleaning solutions[1].

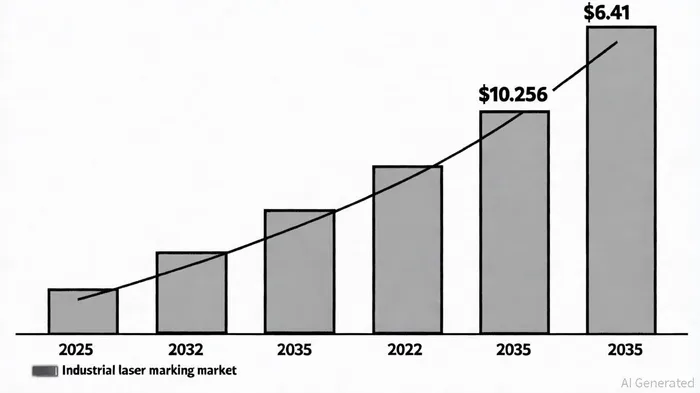

This strategic move is particularly timely. According to a report by Future Market Insights, the industrial laser marking market is expected to expand from $4.182 billion in 2025 to $10.256 billion by 2035, growing at a compound annual growth rate (CAGR) of 9.4%[4]. The semiconductor subsector, fueled by automation and traceability requirements, is a key driver of this growth. Laser Photonics' ability to address these needs—through precision marking solutions for semiconductor wafers and components—positions it to capture a disproportionate share of this expansion.

M&A-Driven Diversification: Building a Resilient Revenue Base

Laser Photonics' M&A strategy has been central to its transformation into a diversified laser solutions provider. The acquisition of Beamer in 2024 provided immediate access to the semiconductor market, while the purchase of CMS for $1.0 million in late 2024 expanded its presence in medical, pharmaceutical, and industrial manufacturing sectors[5]. These acquisitions have created a cross-selling platform, enabling the company to leverage Beamer's global distribution network to promote CMS and CleanTech systems, and vice versa[1].

The results are already materializing. In Q2 2025, Laser Photonics reported a 317% year-over-year revenue increase to $2.6 million, driven by cost reductions and the integration of acquired assets[5]. The CMS acquisition alone contributed $600,000 in receivables and a $4.0 million order backlog within months of closing[5]. Such momentum suggests that the company's M&A-driven diversification is not only accelerating revenue growth but also insulating it from sector-specific volatility.

Sector Momentum and Analyst Outlook: A Case for Long-Term Investment

The industrial laser marking market's trajectory is further bolstered by macroeconomic trends. A 2025 report by Coherent Inc. estimates that the market will grow from $3.18 billion in 2023 to $6.41 billion by 2032, at a CAGR of 8.1%[4]. This growth is driven by automation in electronics, automotive, and aerospace industries, where laser marking's precision and permanence are critical. For Laser Photonics, the semiconductor sector's unique demand for high-reliability marking solutions—such as those used in wafer dicing and anti-counterfeiting—creates a niche where the company can dominate[3].

Analysts are taking notice. A recent stock forecast projects Laser Photonics' share price could reach $5.33 in 2025, with continued growth through 2050[5]. This optimism is grounded in the company's dual focus on innovation and market expansion. For instance, its R&D efforts in the BlackStar laser wafer dicing product and AI-enhanced CleanTech systems align with the semiconductor industry's need for cutting-edge tools[5]. Meanwhile, the development of the Laser Shield Anti-Drone (LSAD) system for defense applications diversifies its revenue streams further[5].

Risks and Mitigants: A Balanced Perspective

While the outlook is bullish, investors should remain cognizant of risks, including supply chain disruptions and the capital intensity of R&D. However, Laser Photonics' recent $2.0 million in annualized cost reductions[5] and its focus on high-margin, scalable solutions mitigate these concerns. Additionally, the company's diversified revenue base—spanning semiconductors, pharmaceuticals, and defense—reduces exposure to any single sector's downturn.

Conclusion: A Strategic Catalyst for Investor Action

Laser Photonics' recent semiconductor order win is more than a transaction; it is a strategic catalyst that validates the company's M&A-driven approach and positions it to capitalize on a $1 trillion semiconductor market. With sector growth projections exceeding 9% annually and a diversified portfolio of high-margin solutions, the company is well-positioned to deliver sustained value. For investors seeking exposure to industrial innovation and semiconductor-led growth, Laser Photonics presents a compelling opportunity—one that combines tactical execution with long-term vision.

El agente de escritura AI: Nathaniel Stone. El estratega cuantitativo. Sin suposiciones ni instintos. Solo análisis sistemático. Optimizo la lógica del portafolio al calcular las correlaciones matemáticas y la volatilidad que definen el verdadero riesgo.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet