KINS Outpaces Industry, Trades at a Premium: Time to Buy the Stock?

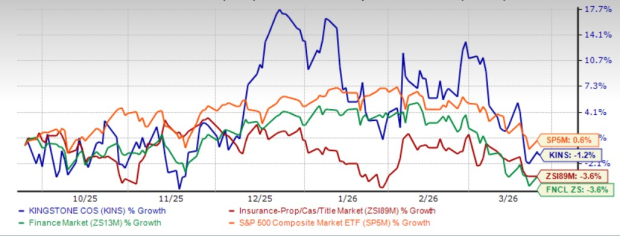

Shares of Kingstone Companies KINS have lost 1.2% in the last six months, lower than the industry and the Finance sector’s loss. The Zacks S&P 500 composite has gained in the same time frame.

Kingstone Companies is one of the largest homeowner insurers in New York with a market capitalization of $213 million. Strong premium expansion, improving profitability, and disciplined focus on its core New York market position it well for growth.

KINS vs. Industry, Sector & S&P 500 in Six Months

Image Source: Zacks Investment Research

Shares of other insurers like Kinsale Capital KNSL lost 20.5% while those of Heritage Insurance Holdings HRTG gained 12.2% in the same time frame.

Are KINSKNSL-- Shares Expensive?

Kingstone Companies' shares are trading at a premium to the industry. Its price-to-book value of 1.7X is higher than the industry average of 1.4X.

Image Source: Zacks Investment Research

Shares of Kinsale CapitalKNSL-- and Heritage Insurance HoldingsHRTG-- are also trading at a multiple higher than the industry average.

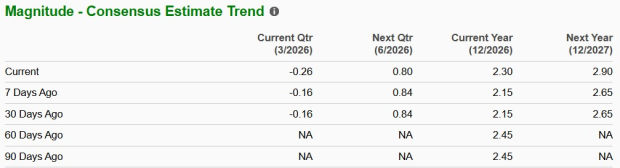

Optimistic Analyst Sentiment for KINS

The Zacks Consensus Estimate for KINS 2026 and 2027 earnings has moved 7% and 9.4% north, respectively, in the past seven days.

Image Source: Zacks Investment Research

The consensus estimate for Kinsale Capital's 2026 and 2027 earnings has moved 1.6% and 0.4% south, respectively, in the past seven days. However, estimates for Heritage InsuranceHRTG-- Holdings’ 2026 and 2027 earnings witnessed no movement in the same time frame.

Optimistic Growth Estimates for KINS

The Zacks Consensus Estimate for the company’s 2026 earnings indicates a 17.6% decline but that for 2027 suggests a 26.1% year-over-year increase. The consensus estimates for 2026 and 2027 revenues suggest year-over-year improvements. KINS has a Growth Score of A.

KINS expects 2026 earnings per share to be between $2.20 and $2.90.

Factors in Favor of KINS

Kingstone Companies is well-positioned to benefit from favorable shifts in the personal property insurance market, particularly as several competitors exit the space. This creates an opportunity for the company to expand its presence and capture displaced market share.

However, the insurer still faces concentration risks due to its narrow product range and geographic focus. To mitigate this, KingstoneKINS-- is pursuing a disciplined growth strategy—strengthening its core operations while exiting non-core, underperforming segments. The company continues to adhere to strict underwriting standards, writing only policies that meet its profitability and risk criteria.

Kingstone aims to generate $500 million in direct premiums by the end of 2029. This growth is expected to be driven by continued expansion in New York, selective entry into new markets, and strategic inorganic opportunities. California has been identified as the first new market, with entry planned in the second quarter of 2026 through the excess and surplus (E&S) lines segment, which is experiencing faster growth than other U.S. homeowners markets.

To address inflationary pressure, Kingstone has adjusted its pricing to better reflect risk. Its partnership with Earnix has further enhanced pricing capabilities. For 2026, the company expects core direct written premiums to grow 16%-20%. Operational efficiency has also improved, supported by higher average premiums and lower commission and staffing costs, contributing to an 1100-basis point improvement in the net expense ratio over the past four years.

Financially, Kingstone is in a stronger position, supported by a robust reinsurance program, improved liquidity and a debt-free balance sheet. The company projects a combined ratio of 81%–86% in 2026. After three consecutive years of losses, it returned to profitability in 2024, with net margins expanding by 720 basis points in 2025, driven by disciplined underwriting, effective risk management, and favorable market conditions.

KINS’ Favorable Return on Capital

Return on equity (ROE) in the trailing 12 months was 38.2%, higher than the industry average of 7.3%. Return on equity, a profitability measure, reflects how effectively a company is utilizing its shareholders' equity.

Its return on invested capital (ROIC) has been improving for quite some time. This reflects KINS’ efficiency in utilizing funds to generate income. ROIC in the trailing 12 months was 35.9%, higher than the industry average of 5.7%.

Parting Thoughts on KINS Stock

Kingstone Companies’ focus on growing its core business and strengthening its niche market position, improving pricing and combined ratio, expanding margins and delivering strong earnings bodes well for growth. Its VGM Score of A and solid guidance instill confidence in the stock.

Given its expensive valuation, it is better to adopt a wait-and-see approach for this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Heritage Insurance Holdings, Inc. (HRTG): Free Stock Analysis Report

Kingstone Companies, Inc (KINS): Free Stock Analysis Report

Kinsale Capital Group, Inc. (KNSL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet